Abstract

This project explores the identification of patterns in stock market volatility through feature engineering and data analysis. Using historical financial data from the Nasdaq 100 index, the study examines the benefits of using percentage change in price over absolute price values to ensure fair comparison and better model scaling. The research introduces a window based pattern recognition approach to identify recurring price movements before significant returns or losses. By extracting datetime features and analyzing the relationship between volatility and specific time intervals, the project provides a foundation for developing automated trading strategies based on historical price behavior.

Overview

This project uses financial data obtained from Yahoo Finance using an open source library. The data will then be explored and pre-processed to be used as training and testing datasets for the implementation of machine learning models. The implementation of the machine learning models will be done in the second part of the coursework. The project plan is to prepare a dataset of the three most volatile companies from the Nasdaq 100 index technology sector to be used for the machine learning models. Then we compare the results of these trained machine learning models. We could then use the best performing model or use them all together as an ensemble of models along with some ruleset to trade the markets.

The following coursework will cover data selection, preparing the data, preprocessing the data, and some analysis for it.

Installing yFinance

# Installing yfinance

%pip install yfinanceNote: you may need to restart the kernel to use updated packages.Requirement already satisfied: yfinance in c:\users\edwin teoh\anaconda3\lib\site-packages (0.2.33)

Requirement already satisfied: beautifulsoup4>=4.11.1 in c:\users\edwin teoh\anaconda3\lib\site-packages (from yfinance) (4.11.1)

Requirement already satisfied: pandas>=1.3.0 in c:\users\edwin teoh\anaconda3\lib\site-packages (from yfinance) (1.4.2)

Requirement already satisfied: peewee>=3.16.2 in c:\users\edwin teoh\anaconda3\lib\site-packages (from yfinance) (3.17.0)

Requirement already satisfied: appdirs>=1.4.4 in c:\users\edwin teoh\anaconda3\lib\site-packages (from yfinance) (1.4.4)

Requirement already satisfied: pytz>=2022.5 in c:\users\edwin teoh\anaconda3\lib\site-packages (from yfinance) (2023.3.post1)

Requirement already satisfied: requests>=2.31 in c:\users\edwin teoh\anaconda3\lib\site-packages (from yfinance) (2.31.0)

Requirement already satisfied: frozendict>=2.3.4 in c:\users\edwin teoh\anaconda3\lib\site-packages (from yfinance) (2.4.0)

Requirement already satisfied: multitasking>=0.0.7 in c:\users\edwin teoh\anaconda3\lib\site-packages (from yfinance) (0.0.11)

Requirement already satisfied: html5lib>=1.1 in c:\users\edwin teoh\anaconda3\lib\site-packages (from yfinance) (1.1)

Requirement already satisfied: numpy>=1.16.5 in c:\users\edwin teoh\anaconda3\lib\site-packages (from yfinance) (1.26.2)

Requirement already satisfied: lxml>=4.9.1 in c:\users\edwin teoh\anaconda3\lib\site-packages (from yfinance) (5.0.0)

Requirement already satisfied: soupsieve>1.2 in c:\users\edwin teoh\anaconda3\lib\site-packages (from beautifulsoup4>=4.11.1->yfinance) (2.3.1)

Requirement already satisfied: six>=1.9 in c:\users\edwin teoh\anaconda3\lib\site-packages (from html5lib>=1.1->yfinance) (1.16.0)

Requirement already satisfied: webencodings in c:\users\edwin teoh\anaconda3\lib\site-packages (from html5lib>=1.1->yfinance) (0.5.1)

Requirement already satisfied: python-dateutil>=2.8.1 in c:\users\edwin teoh\anaconda3\lib\site-packages (from pandas>=1.3.0->yfinance) (2.8.2)

Requirement already satisfied: charset-normalizer<4,>=2 in c:\users\edwin teoh\anaconda3\lib\site-packages (from requests>=2.31->yfinance) (2.0.4)

Requirement already satisfied: certifi>=2017.4.17 in c:\users\edwin teoh\anaconda3\lib\site-packages (from requests>=2.31->yfinance) (2021.10.8)

Requirement already satisfied: idna<4,>=2.5 in c:\users\edwin teoh\anaconda3\lib\site-packages (from requests>=2.31->yfinance) (3.3)

Requirement already satisfied: urllib3<3,>=1.21.1 in c:\users\edwin teoh\anaconda3\lib\site-packages (from requests>=2.31->yfinance) (1.26.9)Importing Libraries

import numpy as np

from bs4 import BeautifulSoup

import requests

from matplotlib import pyplot as plt

import seaborn as sns

import pandas as pd

import yfinance as yfNote:

That the visualization may change due to the data being updated.

The changes may not be drastic as there are only a few values updated daily.

Choosing Data

The data that we will be using in this project are going to be financial stock data as the project involve using machine learning models to predict stock prices.

The data chosen are from Yahoo Finance, specifically from their library that can be directly installed in Python for ease of use. There are several methods that can also be used to obtain the data which will also be demonstrated later in the project. The data will also be pre-processed before it is used for the machine learning model.

The companies that are chosen for the project will be based on our analysis later to see which stocks from the Nasdaq 100 index, specifically the technology stocks, have the higher standard deviation. Stocks with higher standard deviation have more opportunities for shorter term trades that could be profitable. We will then use the top three stocks selected to be trained individually and another model with the Nasdaq 100 index to see which will perform better.

Getting the list of 30 Companies in Nasdaq 100 index

The website here was chosen as it lists the companies that are in the Nasdaq 100 index and specifically the technology sector. Given any large changes or news that affect any of the 30 companies listed here it should stay the same. But do take note that the list might change.

headers = {

"user-agent":"Mozilla/5.0 (X11; Linux x86_64) AppleWebKit/537.36 (KHTML, like Gecko) Chrome/61.0.3163.100 Safari/537.36"

}

tech_companies_site = 'https://finance.yahoo.com/quote/%5ENDXT/components?p=%5ENDXT'

tech_companies_request = requests.get(tech_companies_site,headers=headers)# Checking if the request was successful

tech_companies_request.status_code200tech_companies_df = pd.read_html(tech_companies_request.content)

tech_companies_df[0] Symbol Company Name Last Price Change \

0 ASML ASML Holding N.V. 717.75 -0.04

1 ADI Analog Devices, Inc. 188.44 0.07

2 MDB MongoDB, Inc. 393.49 0.35

3 META Meta Platforms, Inc. 370.12 -0.35

4 GOOG Alphabet Inc. 143.60 -0.20

5 ANSS ANSYS, Inc. 355.54 0.68

6 NXPI NXP Semiconductors N.V. 210.87 -0.42

7 INTU Intuit Inc. 607.46 -1.24

8 GOOGL Alphabet Inc. 141.97 -0.31

9 CDW CDW Corporation 220.99 0.71

10 QCOM QUALCOMM Incorporated 138.84 -0.47

11 MSFT Microsoft Corporation 384.45 1.68

12 AAPL Apple Inc. 185.35 -0.85

13 AMD Advanced Micro Devices, Inc. 147.71 -0.83

14 NVDA NVIDIA Corporation 546.79 3.29

15 DDOG Datadog, Inc. 120.92 0.73

16 MU Micron Technology, Inc. 83.09 0.71

17 CRWD CrowdStrike Holdings, Inc. 284.50 2.46

18 ADSK Autodesk, Inc. 240.93 2.11

19 KLAC KLA Corporation 561.04 4.95

20 AMAT Applied Materials, Inc. 151.24 1.43

21 GFS GLOBALFOUNDRIES Inc. 56.63 -0.55

22 TXN Texas Instruments Incorporated 165.45 -1.80

23 LRCX Lam Research Corporation 758.89 9.20

24 DASH DoorDash, Inc. 104.10 -1.49

25 PDD PDD Holdings Inc. 151.64 2.45

26 AVGO Broadcom Inc. 1098.37 17.80

27 ON ON Semiconductor Corporation 74.28 -1.33

28 CTSH Cognizant Technology Solutions Corporation 74.71 1.36

29 PANW Palo Alto Networks, Inc. 322.81 6.72

% Change Volume

0 -0.01% 420852

1 +0.04% 1645541

2 +0.09% 1016993

3 -0.09% 14623797

4 -0.14% 13891962

5 +0.19% 612520

6 -0.20% 943793

7 -0.20% 858896

8 -0.22% 20136213

9 +0.32% 318119

10 -0.34% 4701678

11 +0.44% 21135744

12 -0.45% 36857156

13 -0.56% 57576536

14 +0.61% 55306006

15 +0.61% 2384169

16 +0.86% 7473666

17 +0.87% 2990299

18 +0.88% 648072

19 +0.89% 351522

20 +0.95% 3834207

21 -0.96% 433762

22 -1.08% 3070799

23 +1.23% 459184

24 -1.41% 1982696

25 +1.64% 4449454

26 +1.65% 1533869

27 -1.76% 7649211

28 +1.85% 1750842

29 +2.13% 4176703| Column | Description |

|---|---|

| Symbol | Short abbreviation of the company name. |

| Company Name | Self Explanatory |

| Last Price | The latest price. at the given time |

| Change | The change in price based on the last price, at the given time |

| % Change | The change in price based on the last price, in percentage, at the given time |

| Volume | How much available share there is in the market at the given time |

# Check if the columns are as shown, without spacing/blanks in the column name

tech_companies_df[0].columnsIndex(['Symbol', 'Company Name', 'Last Price', 'Change', '% Change', 'Volume'], dtype='object')We are only interested in getting the list of symbols

tech_companies_symbols_list = tech_companies_df[0]['Symbol'].sort_values()

tech_companies_symbols_list12 AAPL

1 ADI

18 ADSK

20 AMAT

13 AMD

5 ANSS

0 ASML

26 AVGO

9 CDW

17 CRWD

28 CTSH

24 DASH

15 DDOG

21 GFS

4 GOOG

8 GOOGL

7 INTU

19 KLAC

23 LRCX

2 MDB

3 META

11 MSFT

16 MU

14 NVDA

6 NXPI

27 ON

29 PANW

25 PDD

10 QCOM

22 TXN

Name: Symbol, dtype: objectUsing Yahoo Finance via Web Scraping

Given this link we can make some changes to it and then get the stock price data we need. But using the URL this way we would need to understand the time period that is used in the URL. We will need to convert our desired timeline into Unix timestamp. Furthermore, by using this method we are only limited to dataset intervals of one day, one week, or one month. Datasets with intervals of lower than one day cannot be accessed easily or at least based on the limited time we had to explore ways to scrape this. Yahoo Finance have also properly formatted the data so that we can easily use pd.read_html to extract the table into a DataFrame.

site = 'https://sg.finance.yahoo.com/quote/AAPL/history?period1=345427200&period2=1704153600&interval=1d&filter=history&frequency=1d&includeAdjustedClose=true'

dataset_request = requests.get(site,headers=headers)dataset_request.status_code200pd.read_html(dataset_request.content)[0] Date \

0 29 Dec 2023

1 28 Dec 2023

2 27 Dec 2023

3 26 Dec 2023

4 22 Dec 2023

.. ...

96 15 Aug 2023

97 14 Aug 2023

98 11 Aug 2023

99 11 Aug 2023

100 *Close price adjusted for splits.**Close price...

Open \

0 193.90

1 194.14

2 192.49

3 193.61

4 195.18

.. ...

96 178.88

97 177.97

98 177.32

99 0.24 Dividend

100 *Close price adjusted for splits.**Close price...

High \

0 194.40

1 194.66

2 193.50

3 193.89

4 195.41

.. ...

96 179.48

97 179.69

98 178.62

99 0.24 Dividend

100 *Close price adjusted for splits.**Close price...

Low \

0 191.73

1 193.17

2 191.09

3 192.83

4 192.97

.. ...

96 177.05

97 177.31

98 176.55

99 0.24 Dividend

100 *Close price adjusted for splits.**Close price...

Close* \

0 192.53

1 193.58

2 193.15

3 193.05

4 193.60

.. ...

96 177.45

97 179.46

98 177.79

99 0.24 Dividend

100 *Close price adjusted for splits.**Close price...

Adj. close** \

0 192.53

1 193.58

2 193.15

3 193.05

4 193.60

.. ...

96 177.22

97 179.22

98 177.56

99 0.24 Dividend

100 *Close price adjusted for splits.**Close price...

Volume

0 42628800

1 34049900

2 48087700

3 28919300

4 37122800

.. ...

96 43622600

97 43675600

98 51988100

99 0.24 Dividend

100 *Close price adjusted for splits.**Close price...

[101 rows x 7 columns]Now we try by using the period of 10 Aug 2023, until today, in unix timestamp, then setting the interval to 1h and changing 'AAPL' to 'C' (the ticker for Citibank), and changing both the interval and frequency to 1 hour.

site = 'https://sg.finance.yahoo.com/quote/AAPL/history?period1=1696934989&period2=1704883789&interval=1h&filter=history&frequency=1h&includeAdjustedClose=true'

dataset_request = requests.get(site,headers=headers)dataset_request.status_code200pd.read_html(dataset_request.content)[0] Date \

0 10 Nov 2023

1 *Close price adjusted for splits.**Close price...

Open \

0 0.24 Dividend

1 *Close price adjusted for splits.**Close price...

High \

0 0.24 Dividend

1 *Close price adjusted for splits.**Close price...

Low \

0 0.24 Dividend

1 *Close price adjusted for splits.**Close price...

Close* \

0 0.24 Dividend

1 *Close price adjusted for splits.**Close price...

Adj. close** \

0 0.24 Dividend

1 *Close price adjusted for splits.**Close price...

Volume

0 0.24 Dividend

1 *Close price adjusted for splits.**Close price...But now, we try once more, using the same time period, but changing the interval and frequency in the URL, back tto '1d' from '1h'

site = 'https://sg.finance.yahoo.com/quote/AAPL/history?period1=1696934989&period2=1704883789&interval=1d&filter=history&frequency=1d&includeAdjustedClose=true'

dataset_request = requests.get(site,headers=headers)

dataset_request.status_code200pd.read_html(dataset_request.content)[0] Date \

0 09 Jan 2024

1 08 Jan 2024

2 05 Jan 2024

3 04 Jan 2024

4 03 Jan 2024

.. ...

60 13 Oct 2023

61 12 Oct 2023

62 11 Oct 2023

63 10 Oct 2023

64 *Close price adjusted for splits.**Close price...

Open \

0 183.92

1 182.09

2 181.99

3 182.15

4 184.22

.. ...

60 181.42

61 180.07

62 178.20

63 178.10

64 *Close price adjusted for splits.**Close price...

High \

0 185.15

1 185.60

2 182.76

3 183.09

4 185.88

.. ...

60 181.93

61 182.34

62 179.85

63 179.72

64 *Close price adjusted for splits.**Close price...

Low \

0 182.73

1 181.50

2 180.17

3 180.88

4 183.43

.. ...

60 178.14

61 179.04

62 177.60

63 177.95

64 *Close price adjusted for splits.**Close price...

Close* \

0 185.14

1 185.56

2 181.18

3 181.91

4 184.25

.. ...

60 178.85

61 180.71

62 179.80

63 178.39

64 *Close price adjusted for splits.**Close price...

Adj. close** \

0 185.14

1 185.56

2 181.18

3 181.91

4 184.25

.. ...

60 178.61

61 180.47

62 179.56

63 178.16

64 *Close price adjusted for splits.**Close price...

Volume

0 42841800

1 59144500

2 62303300

3 71983600

4 58414500

.. ...

60 51427100

61 56743100

62 47551100

63 43698000

64 *Close price adjusted for splits.**Close price...

[65 rows x 7 columns]As shown, the granularity required from the dataset, cannot achieve by using this method.

Using yfinance to extract data

Using this method is easier and faster. But there are also some limitations faced. Given the interval that is chosen to be downloaded, the timeframe or the duration of the data gets shorter. For example, a daily interval dataset can be downloaded with the full timeline of a stock. If we want to have a dataset that has an interval of five minutes we can only get a maximum of 60 days. It is also understandable that the dataset size also increases significantly the lower the interval we go. Additionally, the more granular the dataset is, the more likely it is that we will have to either make a purchase or subscribe to such access of information.

aapl = yf.Ticker("AAPL")

aapl.history(period='70d',interval='5m')AAPL: 5m data not available for startTime=1698958004 and endTime=1705006004. The requested range must be within the last 60 days.Empty DataFrame

Columns: [Open, High, Low, Close, Adj Close, Volume]

Index: []aapl.history(period='5y',interval='1h')AAPL: 1h data not available for startTime=1547326005 and endTime=1705006005. The requested range must be within the last 730 days.Empty DataFrame

Columns: [Open, High, Low, Close, Adj Close, Volume]

Index: []aapl.history(period='7d',interval='1m') Open High Low Close \

Datetime

2024-01-03 09:30:00-05:00 184.220001 184.740005 183.860001 184.690002

2024-01-03 09:31:00-05:00 184.679993 185.220001 184.470001 185.100098

2024-01-03 09:32:00-05:00 185.100006 185.330002 184.929993 185.259995

2024-01-03 09:33:00-05:00 185.270004 185.380005 185.080002 185.360001

2024-01-03 09:34:00-05:00 185.365005 185.688705 185.270004 185.630005

... ... ... ... ...

2024-01-11 15:42:00-05:00 185.429993 185.464996 185.375000 185.399994

2024-01-11 15:43:00-05:00 185.395004 185.419998 185.350006 185.409195

2024-01-11 15:44:00-05:00 185.399994 185.500000 185.399994 185.414993

2024-01-11 15:45:00-05:00 185.419998 185.470001 185.360001 185.384995

2024-01-11 15:46:00-05:00 185.370102 185.370102 185.370102 185.370102

Volume Dividends Stock Splits

Datetime

2024-01-03 09:30:00-05:00 2565996 0.0 0.0

2024-01-03 09:31:00-05:00 492296 0.0 0.0

2024-01-03 09:32:00-05:00 353071 0.0 0.0

2024-01-03 09:33:00-05:00 295721 0.0 0.0

2024-01-03 09:34:00-05:00 492106 0.0 0.0

... ... ... ...

2024-01-11 15:42:00-05:00 80598 0.0 0.0

2024-01-11 15:43:00-05:00 74422 0.0 0.0

2024-01-11 15:44:00-05:00 78927 0.0 0.0

2024-01-11 15:45:00-05:00 73016 0.0 0.0

2024-01-11 15:46:00-05:00 0 0.0 0.0

[2711 rows x 7 columns]aapl.history(period='8d',interval='1m')AAPL: 1m data not available for startTime=1704314805 and endTime=1705006005. Only 7 days worth of 1m granularity data are allowed to be fetched per request.Empty DataFrame

Columns: [Open, High, Low, Close, Adj Close, Volume]

Index: []aapl = yf.Ticker("AAPL")

aapl.history(period='730d',interval='1h') Open High Low Close \

Datetime

2021-02-18 09:30:00-05:00 129.199997 129.679993 127.410004 128.119904

2021-02-18 10:30:00-05:00 128.100006 129.104996 127.830002 128.675705

2021-02-18 11:30:00-05:00 128.669998 128.710007 127.900002 128.620102

2021-02-18 12:30:00-05:00 128.625000 129.070007 128.449997 128.994995

2021-02-18 13:30:00-05:00 129.000000 129.050003 128.449997 128.710007

... ... ... ... ...

2024-01-11 11:30:00-05:00 184.184998 184.449997 183.835007 184.050003

2024-01-11 12:30:00-05:00 184.074997 184.777206 184.074997 184.654999

2024-01-11 13:30:00-05:00 184.669998 185.539993 184.559998 185.514999

2024-01-11 14:30:00-05:00 185.520004 185.699997 184.755005 185.369995

2024-01-11 15:30:00-05:00 185.369995 185.559998 185.350006 185.370102

Volume Dividends Stock Splits

Datetime

2021-02-18 09:30:00-05:00 28938326 0.0 0.0

2021-02-18 10:30:00-05:00 13477687 0.0 0.0

2021-02-18 11:30:00-05:00 12770713 0.0 0.0

2021-02-18 12:30:00-05:00 8465690 0.0 0.0

2021-02-18 13:30:00-05:00 8516504 0.0 0.0

... ... ... ...

2024-01-11 11:30:00-05:00 3849444 0.0 0.0

2024-01-11 12:30:00-05:00 4000614 0.0 0.0

2024-01-11 13:30:00-05:00 3924789 0.0 0.0

2024-01-11 14:30:00-05:00 4502053 0.0 0.0

2024-01-11 15:30:00-05:00 1503923 0.0 0.0

[5094 rows x 7 columns]The decision to use 1 hour interval, and about 2 years to 3 years of data, will be used in the project. This is because the timeframe is fast enough where we can try to implement a system or program that can support our decisions for short term trading, and that there will be enough data to experiment. If the timeframe was too long such as 1 day for the span of 10 year, then the program will at most try to make daily or weekly decisions. Going with an hourly interval dataset, allow us to explore an hourly model or system. If we would like to take it slow and and make decisions based on a longer timeframe, we still have to option to do so.

tech_companies_history_list = []

for tech_company in tech_companies_symbols_list:

temp = yf.Ticker(tech_company)

tech_companies_history_list.append((tech_company, temp.history(period='730d',interval='1h')))

tech_companies_history_list[0]GFS: 1h data not available for startTime=1635427800 and endTime=1705006008. The requested range must be within the last 730 days.('AAPL',

Open High Low Close \

Datetime

2021-02-18 09:30:00-05:00 129.199997 129.679993 127.410004 128.119904

2021-02-18 10:30:00-05:00 128.100006 129.104996 127.830002 128.675705

2021-02-18 11:30:00-05:00 128.669998 128.710007 127.900002 128.620102

2021-02-18 12:30:00-05:00 128.625000 129.070007 128.449997 128.994995

2021-02-18 13:30:00-05:00 129.000000 129.050003 128.449997 128.710007

... ... ... ... ...

2024-01-11 11:30:00-05:00 184.184998 184.449997 183.835007 184.050003

2024-01-11 12:30:00-05:00 184.074997 184.777206 184.074997 184.654999

2024-01-11 13:30:00-05:00 184.669998 185.539993 184.559998 185.514999

2024-01-11 14:30:00-05:00 185.520004 185.699997 184.755005 185.369995

2024-01-11 15:30:00-05:00 185.369995 185.559998 185.350006 185.370102

Volume Dividends Stock Splits

Datetime

2021-02-18 09:30:00-05:00 28938326 0.0 0.0

2021-02-18 10:30:00-05:00 13477687 0.0 0.0

2021-02-18 11:30:00-05:00 12770713 0.0 0.0

2021-02-18 12:30:00-05:00 8465690 0.0 0.0

2021-02-18 13:30:00-05:00 8516504 0.0 0.0

... ... ... ...

2024-01-11 11:30:00-05:00 3849444 0.0 0.0

2024-01-11 12:30:00-05:00 4000614 0.0 0.0

2024-01-11 13:30:00-05:00 3924789 0.0 0.0

2024-01-11 14:30:00-05:00 4502053 0.0 0.0

2024-01-11 15:30:00-05:00 1503923 0.0 0.0

[5094 rows x 7 columns])| Column | Description |

|---|---|

| Open | The price at the start of the interval |

| High | The highest price achieve within the given interval |

| Low | The lowest price achieve within the given interval |

| Close | The price at the end of the interval |

| Volume | The number of share available in the market |

| Dvidends | How much returns are given back to investor, per share. |

| Stock Spits | How many shares gained per share |

The interval mentioned would be 1 hour, as that is the interval chosen for this coursework. But the interval could be 4 hours, 1 day, 1 week, or as low as 1 minute, 1 second or even down to per tick. So the open, high, low, close prices are highly likely to be different the larger the interval selected.

## Checking the number of rows for each company

[len(tech_company[1]) for tech_company in tech_companies_history_list][5094,

5094,

5094,

5080,

5094,

5094,

5094,

5094,

5094,

5094,

5094,

5094,

5094,

0,

5094,

5094,

5066,

5094,

5094,

5094,

5094,

5094,

5085,

5094,

5094,

5092,

5094,

5094,

5094,

5094]max_num_row = pd.DataFrame([len(tech_company[1]) for tech_company in tech_companies_history_list]).max()

max_num_row[0]5094tech_companies = list(

filter(

lambda x: len(x[1]) == max_num_row[0],

tech_companies_history_list

)

)

print("The number of companies left: ", len(tech_companies), end='\n\n')

print("The following are the remaining companies: ")

print(*[x[0] for x in tech_companies],sep=', ')The number of companies left: 25

The following are the remaining companies:

AAPL, ADI, ADSK, AMD, ANSS, ASML, AVGO, CDW, CRWD, CTSH, DASH, DDOG, GOOG, GOOGL, KLAC, LRCX, MDB, META, MSFT, NVDA, NXPI, PANW, PDD, QCOM, TXNUsing change in price

There are many tutorials and courses out there that use stock prices as input, labels and predictors for all kinds of machine learning models. But there are some problems with using prices.

Prices are absolute

Because using the price of the stock at the given time, is not a fair comparison against other stocks. Stocks can have stock splits, which divides the share price by the number of shares, a single share is split into. Some companies do not soar to higher number than others. For example, Berkshire Hathaway Inc Class A shares (Ticker Symbol: BRK.A), as of 6 Jan 2024, they are currently priced at $554,300 per share, while Google Shares are priced at $135.

Scaling

It is also common practice to use some form of scaling to bring value of features closer to one another so that the machine learning models can proper consider all features equally. If we were to use min max scaling, the problem is that any timeframe, there might be a new lowest low and a new highest high. There is no limit to price movement. The model will have difficulty in making prediction with unseen data that are outside the training dataset. If we would like to compare other stock data as well, ones 0.5 might represent a different price from another. Standardization, or the Standard Scaler, has also got similar issue. Most stock data have an upward trend, because in the long term, stock prices do go up. Therefore, stock data based on price, will have increasing mean/average, which indicate that overtime, the model's understanding of value will not represent the same price as it was trained with as well.

Change in Value matters

A trader or an investor still make the same amount of money, given that a stock that cost $100 increases by $10 compared to a stock that cost $10 and increase by $1. Furthermore, with popularity of many financial services and brokers providing the ability to purchase fractional shares (the ability to purchase parts of a stock/share), the absolute price of a stock is not as relevant. A trader or an investor can still reap the benefit of holding Berkshire Hathaway Inc Class A shares with $10. Traders and investors alike can focus on their analysis and finding companies and opportunities without worrying the magnitude of the share price.

Therefore, we will be using percentage change in price as an input.

# Use a single index to access the company ticker and dataset

tech_companies[24]('TXN',

Open High Low Close \

Datetime

2021-02-18 09:30:00-05:00 177.429993 177.520004 174.250000 174.570007

2021-02-18 10:30:00-05:00 174.589996 175.550003 174.220001 174.970001

2021-02-18 11:30:00-05:00 175.020004 175.259995 174.199997 175.149994

2021-02-18 12:30:00-05:00 175.156906 176.149994 174.500000 176.080002

2021-02-18 13:30:00-05:00 176.100006 176.580002 175.639999 176.020004

... ... ... ... ...

2024-01-11 11:30:00-05:00 165.839996 165.880005 165.029999 165.339996

2024-01-11 12:30:00-05:00 165.339996 165.860001 165.289993 165.619995

2024-01-11 13:30:00-05:00 165.600006 166.270004 165.479996 166.119995

2024-01-11 14:30:00-05:00 166.115005 166.440002 165.440002 165.520004

2024-01-11 15:30:00-05:00 165.522797 165.766006 165.410004 165.470001

Volume Dividends Stock Splits

Datetime

2021-02-18 09:30:00-05:00 607178 0.0 0.0

2021-02-18 10:30:00-05:00 443595 0.0 0.0

2021-02-18 11:30:00-05:00 313774 0.0 0.0

2021-02-18 12:30:00-05:00 513549 0.0 0.0

2021-02-18 13:30:00-05:00 410585 0.0 0.0

... ... ... ...

2024-01-11 11:30:00-05:00 558498 0.0 0.0

2024-01-11 12:30:00-05:00 503848 0.0 0.0

2024-01-11 13:30:00-05:00 347788 0.0 0.0

2024-01-11 14:30:00-05:00 490683 0.0 0.0

2024-01-11 15:30:00-05:00 183174 0.0 0.0

[5094 rows x 7 columns])# Use two index to access the company dataset

# Checking the columns

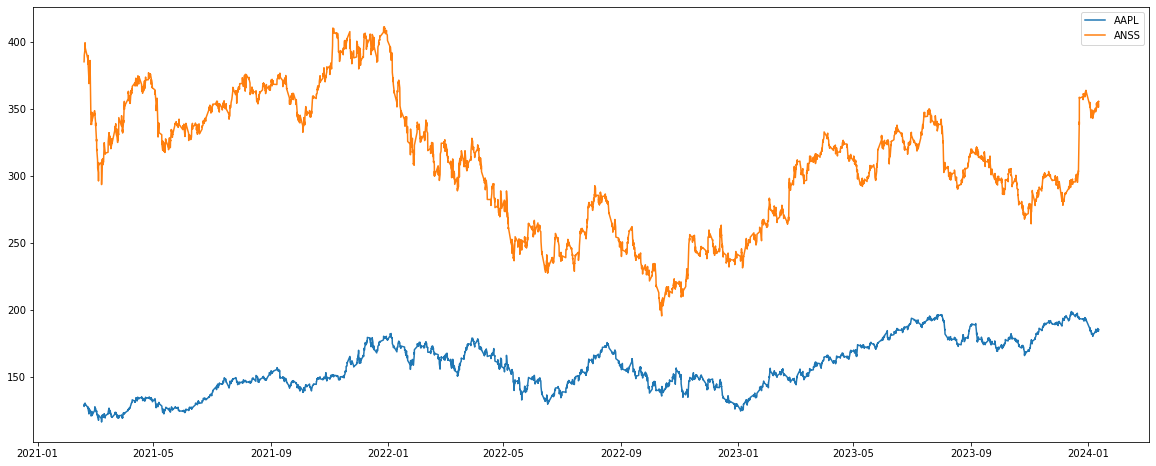

tech_companies[0][1].columnsIndex(['Open', 'High', 'Low', 'Close', 'Volume', 'Dividends', 'Stock Splits'], dtype='object')Plotting two companies' absolute share price

# Datetime as x

# Close price of 2 stock for y

datetime = tech_companies[0][1].index

close_price1 = tech_companies[0][1]['Close']

close_price2 = tech_companies[4][1]['Close']

# Plotting the 2 stock prices

plt.figure(figsize=(20, 8))

plt.plot(datetime, close_price1,label=tech_companies[0][0])

plt.plot(datetime, close_price2,label=tech_companies[4][0])

plt.legend()

Adding % Change in Close Price columns

df1 = tech_companies[0][1]

df1['Close']Datetime

2021-02-18 09:30:00-05:00 128.119904

2021-02-18 10:30:00-05:00 128.675705

2021-02-18 11:30:00-05:00 128.620102

2021-02-18 12:30:00-05:00 128.994995

2021-02-18 13:30:00-05:00 128.710007

...

2024-01-11 11:30:00-05:00 184.050003

2024-01-11 12:30:00-05:00 184.654999

2024-01-11 13:30:00-05:00 185.514999

2024-01-11 14:30:00-05:00 185.369995

2024-01-11 15:30:00-05:00 185.370102

Name: Close, Length: 5094, dtype: float64df1['Close'].shift(1)Datetime

2021-02-18 09:30:00-05:00 NaN

2021-02-18 10:30:00-05:00 128.119904

2021-02-18 11:30:00-05:00 128.675705

2021-02-18 12:30:00-05:00 128.620102

2021-02-18 13:30:00-05:00 128.994995

...

2024-01-11 11:30:00-05:00 184.190002

2024-01-11 12:30:00-05:00 184.050003

2024-01-11 13:30:00-05:00 184.654999

2024-01-11 14:30:00-05:00 185.514999

2024-01-11 15:30:00-05:00 185.369995

Name: Close, Length: 5094, dtype: float64temp_change_of_price = ((df1['Close'] - df1['Close'].shift(1)) / df1['Close'].shift(1))

temp_change_of_priceDatetime

2021-02-18 09:30:00-05:00 NaN

2021-02-18 10:30:00-05:00 4.338135e-03

2021-02-18 11:30:00-05:00 -4.321175e-04

2021-02-18 12:30:00-05:00 2.914732e-03

2021-02-18 13:30:00-05:00 -2.209298e-03

...

2024-01-11 11:30:00-05:00 -7.600814e-04

2024-01-11 12:30:00-05:00 3.287127e-03

2024-01-11 13:30:00-05:00 4.657337e-03

2024-01-11 14:30:00-05:00 -7.816310e-04

2024-01-11 15:30:00-05:00 5.762072e-07

Name: Close, Length: 5094, dtype: float64df1['% Change in Close Price'] = temp_change_of_price

df1['% Change in Close Price']Datetime

2021-02-18 09:30:00-05:00 NaN

2021-02-18 10:30:00-05:00 4.338135e-03

2021-02-18 11:30:00-05:00 -4.321175e-04

2021-02-18 12:30:00-05:00 2.914732e-03

2021-02-18 13:30:00-05:00 -2.209298e-03

...

2024-01-11 11:30:00-05:00 -7.600814e-04

2024-01-11 12:30:00-05:00 3.287127e-03

2024-01-11 13:30:00-05:00 4.657337e-03

2024-01-11 14:30:00-05:00 -7.816310e-04

2024-01-11 15:30:00-05:00 5.762072e-07

Name: % Change in Close Price, Length: 5094, dtype: float64# Initializing the dataframe of 2 stocks

df1 = tech_companies[0][1]

df2 = tech_companies[4][1]

# Create the % Change in Close price columns

df1['% Change in Close Price'] = None

df2['% Change in Close Price'] = None

# Using the change in price (current) and price (previous interval) and divided by the price (previous)

df1['% Change in Close Price'] = (df1['Close'] - df1['Close'].shift(1))/ df1['Close'].shift(1)

df2['% Change in Close Price'] = (df2['Close'] - df2['Close'].shift(1))/ df2['Close'].shift(1)

display(df1[['Close', '% Change in Close Price']])

display(df2[['Close', '% Change in Close Price']])# Removing top row as it is not needed and used.

df1 = df1[1:]

df2 = df2[1:]

display(df1[['Close', '% Change in Close Price']])

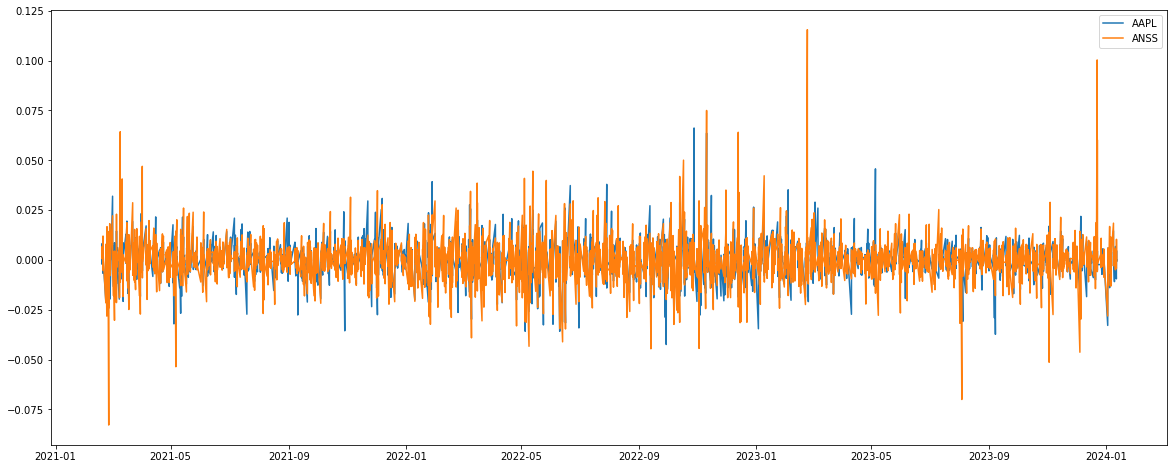

display(df2[['Close', '% Change in Close Price']])Plotting both the % Change in value of 2 stocks

plt.figure(figsize=(20, 8))

plt.plot(df1.index, df1['% Change in Close Price'],label=tech_companies[0][0])

plt.plot(df1.index, df2['% Change in Close Price'],label=tech_companies[4][0])

plt.legend()

As compared to using only price, it can now be fairly compared. The spikes can be seen as large movement and these are the spikes that we would wish to identify. We can try to identify characteristics of such spikes, or even just above average returns. It also now resemble a lot like noise or random data with a very small hints of trends. Once the data is in this form, there are many ways we could further process this as well.

Frequency Distribution

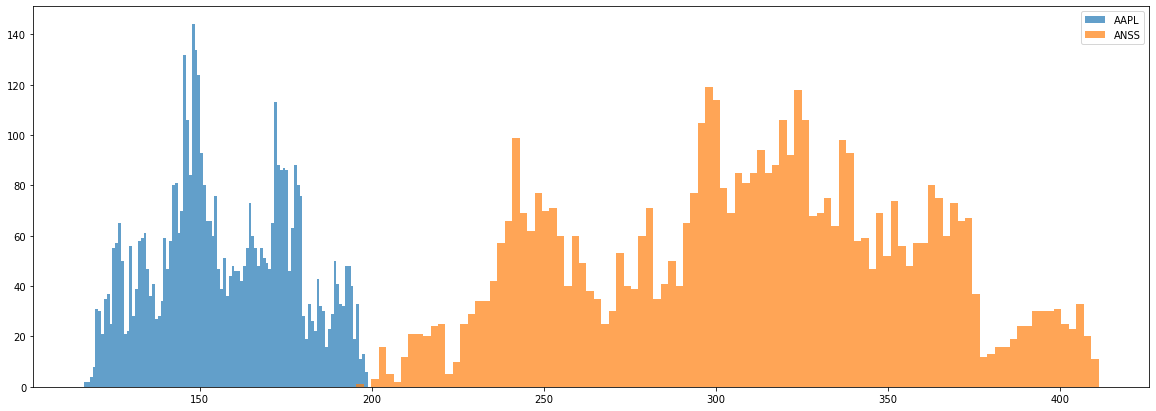

When absolute price is plotted in a frequency distribution, it resemble a crown, because there are average prices that the stock will range between until some large price movement, shifting the average to another price level. Hence, it is like seeing multiple different normal distribution throughout.

plt.figure(figsize=(20, 7))

plt.hist(df1['Close'],bins=100,alpha=0.7,label=tech_companies[0][0])

plt.hist(df2['Close'],bins=100,alpha=0.7,label=tech_companies[4][0])

plt.legend()

plt.show()

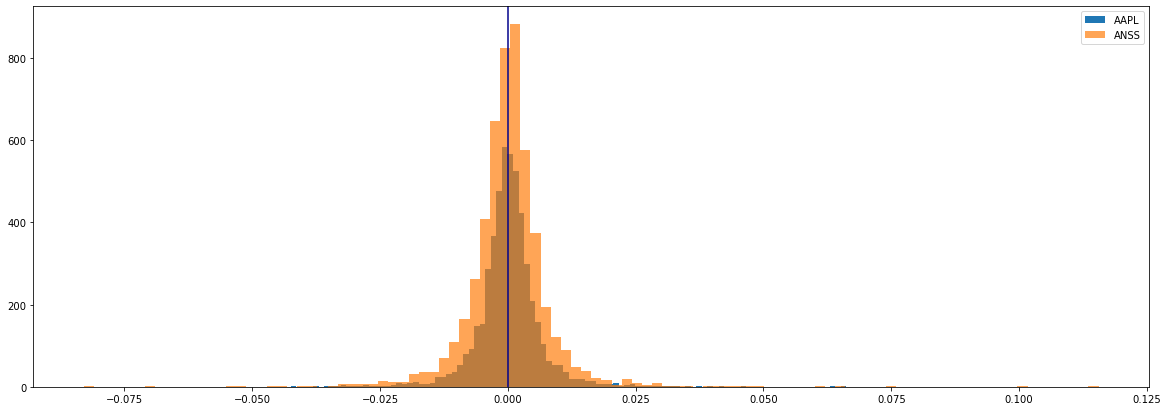

plt.figure(figsize=(20, 7))

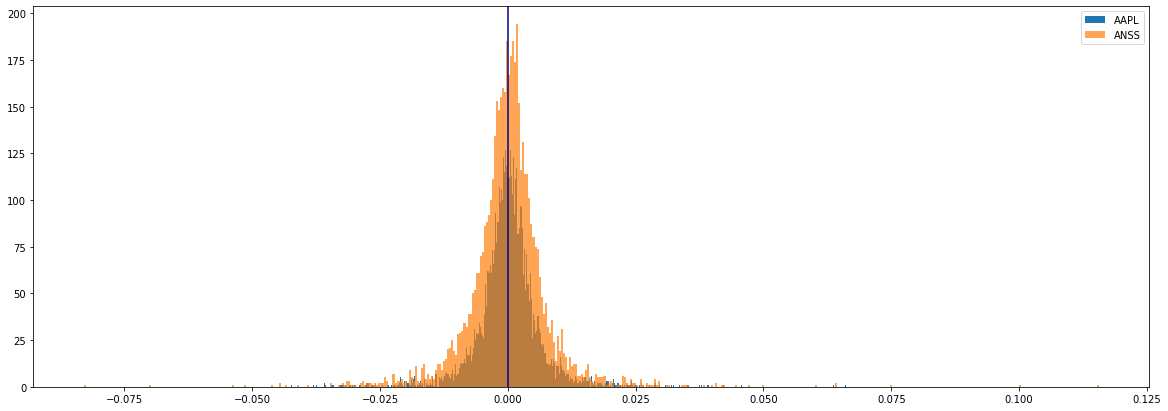

plt.hist(df1['% Change in Close Price'],bins=100,label=tech_companies[0][0])

plt.hist(df2['% Change in Close Price'],bins=100,alpha=0.7,label=tech_companies[4][0])

plt.axvline(x = 0, linestyle = '-', color ='darkblue')

plt.legend()

plt.show()

plt.figure(figsize=(20, 7))

plt.hist(df1['% Change in Close Price'],bins=500,label=tech_companies[0][0])

plt.hist(df2['% Change in Close Price'],bins=500,alpha=0.7,label=tech_companies[4][0])

plt.axvline(x = 0, linestyle = '-', color ='darkblue')

plt.legend()

plt.show()

By using percentage change in price and plotting it in a frequency distribution, we can see that it resembles very much like a normal distribution. In a single glance we can see which stock has more price movement over the other. We can see if it is more skewed to downward price movements or positive movements. Exploration on using methods and models that can take advantage of the normal distribution would be advantageous but it will not be what we will do for this project.

Looking for patterns in % Change in Price, with % Change in Price

Next we will explore some patterns of the percentage change in price to see when it is going to have a positive or negative change. This is achieved by having a window size and desired return. The window size is how far back we want to look to identify a pattern and the desired return will be used as a threshold to filter on the minimum percentage change we would like to see. For example if we have a window size of three and desired return of five percent we will be looping through the percentage change. For each instance of five percent or more we will look back at the last 10 hours of percentage change.

Using the window size of 3 and desired return of 5%, we will use the example list below.

- It will loop through each value. The first value in the list that satisfies the desired return of five percent is the third element. Since we have a window size of three we cannot store the first instance. We continue looping until the next value which is the seventh element.

-

Store the last 3 values before 7%.

-

Then we continue the loop for the next value that satisfies the condition. The next one is the last value. We will then store the last three values.

- Which will give us the final list of

- Analyze the list. Given this toy example, we can see that a negative change, then a 2 percent change with a 3-4 percent change may lead to a high percent change.

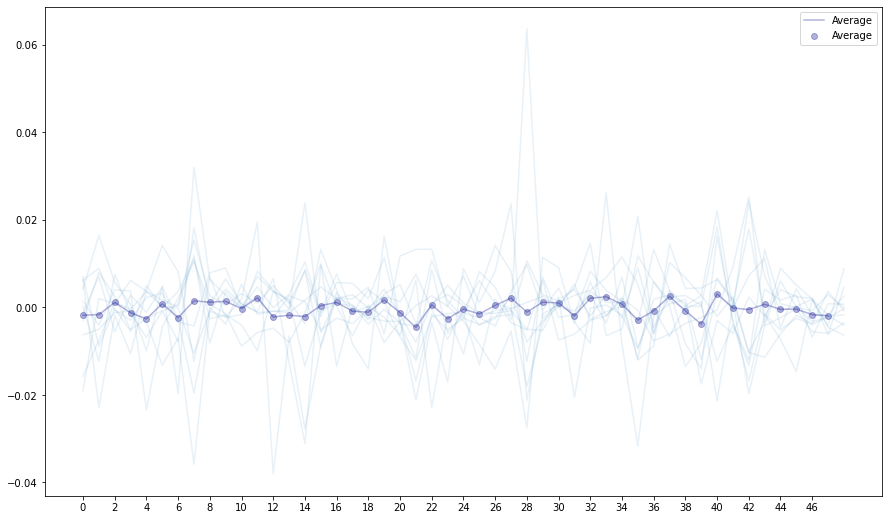

We will explore using a 48 hour window with a desired return of three percent. This is a good number if we would like to have a higher chance of making a return. As shown in the frequency distribution above the higher the return the less likely it will occur. Furthermore if we were to use such a high return there will be too little data to create an average pattern.

# List to store the patterns found

patterns_of_higher_return = []

changes_in_price = df1['% Change in Close Price'].to_list()

# Setting window size and desired return

window_size = 48

desired_returns = 0.03

# Loop the column to find the those that have equal or more than desired returns

for row_no, returns in enumerate(changes_in_price):

if row_no <= window_size:

continue

else:

if returns >= desired_returns:

patterns_of_higher_return.append(changes_in_price[row_no-window_size-1:row_no])

# List to store average pattern

average_pattern_of_higher_return = []

# Loop through a list from 0 to window size, indicating the value on the x axis

for no in range(window_size):

temp = 0

# Loop through the list of patterns and store all the value in the given x axis

for pattern in patterns_of_higher_return:

temp += pattern[no]

# Get the average of the values collected in the given x axis

average_pattern_of_higher_return.append(temp/len(patterns_of_higher_return))

# Set chart size

plt.figure(figsize=(15, 9))

# Plot the average

for i in patterns_of_higher_return:

plt.plot(i,'C0',alpha=0.1)

# Plot the patterns found

plt.plot(average_pattern_of_higher_return,'darkblue',alpha=0.3,label='Average')

plt.scatter([x for x in range(window_size)],average_pattern_of_higher_return,color='darkblue',alpha=0.3,label='Average')

plt.xticks(np.arange(0, window_size, 2.0))

plt.legend()

plt.show()

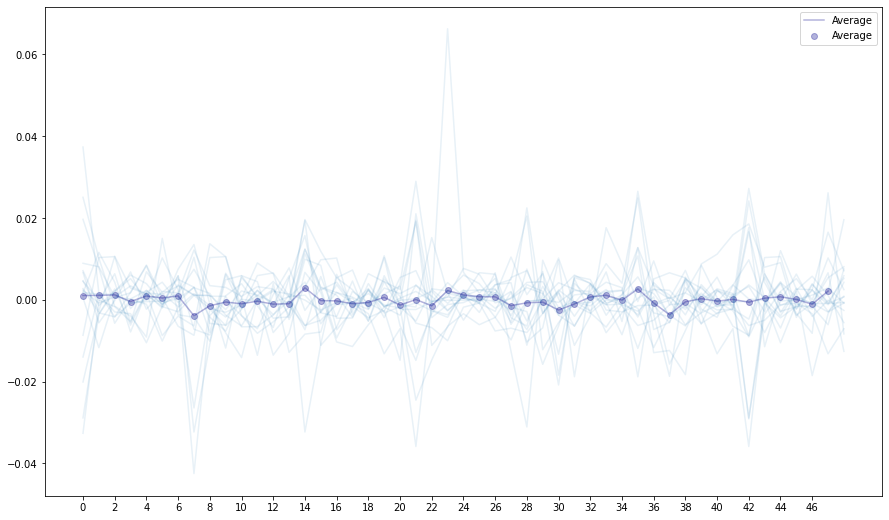

Using the same thing as above, but we look into patterns of losses, are there also patterns that can indicate a negative percentage change?

# List to store the patterns found

patterns_of_higher_losses = []

prices = df1['% Change in Close Price'].to_list()

# Setting window size and desired return

window_size = 48

desired_returns = -0.03

# Loop the column to find the those that have equal or more than desired returns

for row_no, returns in enumerate(prices):

if row_no <= window_size:

continue

else:

if returns <= desired_returns:

patterns_of_higher_losses.append(prices[row_no-window_size-1:row_no])

# List to store average pattern

average_pattern_of_higher_losses = []

# Loop through a list from 0 to window size, indicating the value on the x axis

for no in range(window_size):

temp = 0

# Loop through the list of patterns and store all the value in the given x axis

for pattern in patterns_of_higher_losses:

temp += pattern[no]

# Get the average of the values collected in the given x axis

average_pattern_of_higher_losses.append(temp/len(patterns_of_higher_losses))

# Set chart size

plt.figure(figsize=(15,9))

# Plot the average

for i in patterns_of_higher_losses:

plt.plot(i,'C0',alpha=0.1)

# Plot the patterns found

plt.plot(average_pattern_of_higher_losses,'darkblue',alpha=0.3,label='Average')

plt.scatter([x for x in range(window_size)],average_pattern_of_higher_losses,color='darkblue',alpha=0.3,label='Average')

plt.xticks(np.arange(0, window_size, 2.0))

plt.legend()

plt.show()

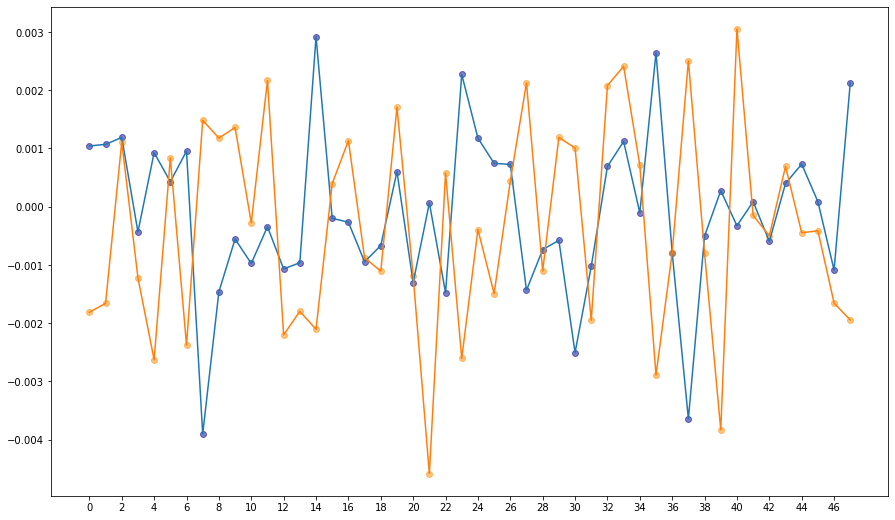

It seems like they do have different areas of peaks and trough. This means that these differences might be able to be used as early indicators for positive or negative change. We can have a clearer view by stacking both of them together.

# Set the chart size

plt.figure(figsize=(15,9))

# Plot both the averages

plt.plot(average_pattern_of_higher_losses)

plt.plot(average_pattern_of_higher_return)

plt.scatter([x for x in range(window_size)],average_pattern_of_higher_losses,color='darkblue',alpha=0.5,label='Average')

plt.scatter([x for x in range(window_size)],average_pattern_of_higher_return,color='darkorange',alpha=0.5,label='Average')

plt.xticks(np.arange(0, window_size, 2.0))

plt.show()

From here we might even be able to use some form of image recognition models or even use dynamic time warping to match the average recurring pattern found here to create a trading strategy. The difference between the pattern identifying a positive percentage change and a negative change seem to have some distinction. It can be seen that there are several areas of opposite values which can be used as an indicator that the next predicted value would be a positive or negative one.

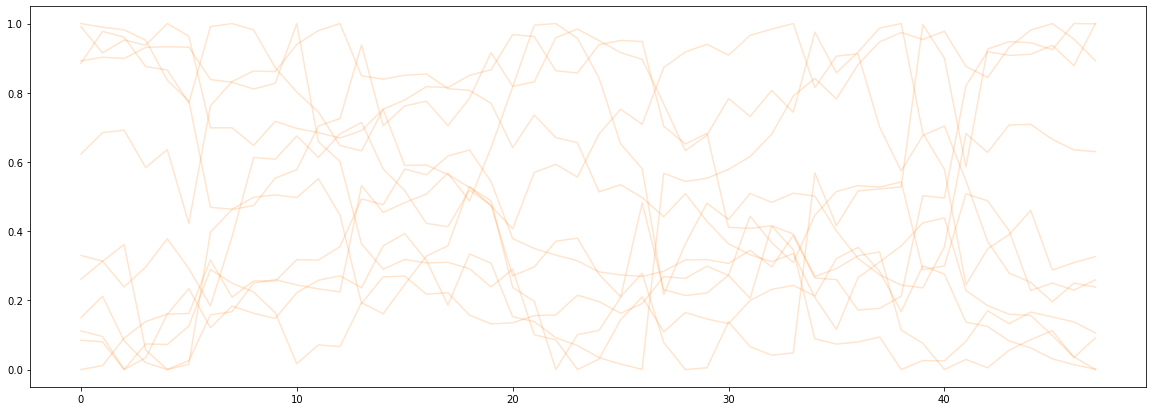

Using Scaled Price

Using the same codes as above, we implement and explore what if we were to use price instead. We will need to scaled the pattern to values between 0 - 1, so that we can compare the different price movement occurring before the desired return. A 5% return but the pattern before it could [1,2,3] and [100,110,113]. If we do not scale the lists individually, we cannot see any meaningful difference among them.

patterns_of_higher_return = []

prices = df1['Close']

return_percentage = df1['% Change in Close Price'].to_list()

window_size = 48

desired_returns = 0.03

for row_no, returns in enumerate(return_percentage):

if row_no <= window_size:

continue

else:

if returns >= desired_returns:

temp = prices[row_no-window_size:row_no]

maxtemp = temp.max()

mintemp = temp.min()

patterns_of_higher_return.append(

[((x-mintemp)/(maxtemp - mintemp))*1 for x in temp]

)

average_pattern_of_higher_return = []

for no in range(window_size):

temp = 0

for pattern in patterns_of_higher_losses:

temp += pattern[no]

average_pattern_of_higher_losses.append(temp/len(patterns_of_higher_losses))

plt.figure(figsize=(20, 7))

x_values = [x for x in range(window_size)]

for i in patterns_of_higher_return:

plt.plot(x_values,i,'C1',alpha=0.2)

plt.show()

By using normal price, even when it is scaled, it is hard to further identify some form of repeatable pattern.

We will explore this again in the later part of the project, after extracting datetime features.

Adding % Change in Close Price for all stocks

change_in_close_price_str = '% Change in Close Price'

reference_column = 'Close'

print('Before adding the column:')

print('Number of Column: ', [len(tech_company[1].columns) for tech_company in tech_companies])

for tech_company in tech_companies:

temp = tech_company[1]

temp[change_in_close_price_str] = (temp[reference_column] - temp[reference_column].shift(1))/temp[reference_column].shift(1)

tech_company[1][change_in_close_price_str] = temp[change_in_close_price_str]

print()

print('After adding the column:')

print('Number of Column: ', [len(tech_company[1].columns) for tech_company in tech_companies])Before adding the column:

Number of Column: [8, 8, 8, 8, 8, 8, 8, 8, 8, 8, 8, 8, 8, 8, 8, 8, 8, 8, 8, 8, 8, 8, 8, 8, 8]

After adding the column:

Number of Column: [8, 8, 8, 8, 8, 8, 8, 8, 8, 8, 8, 8, 8, 8, 8, 8, 8, 8, 8, 8, 8, 8, 8, 8, 8]Processing all other price related columns

Open Price

change_in_close_price_str = '% Change in Open Price'

reference_column = 'Open'

print('Before adding the column:')

print('Number of Column: ', [len(tech_company[1].columns) for tech_company in tech_companies])

for tech_company in tech_companies:

temp = tech_company[1]

temp[change_in_close_price_str] = (temp[reference_column] - temp[reference_column].shift(1))/temp[reference_column].shift(1)

tech_company[1][change_in_close_price_str] = temp[change_in_close_price_str]

print()

print('After adding the column:')

print('Number of Column: ', [len(tech_company[1].columns) for tech_company in tech_companies])Before adding the column:

Number of Column: [8, 8, 8, 8, 8, 8, 8, 8, 8, 8, 8, 8, 8, 8, 8, 8, 8, 8, 8, 8, 8, 8, 8, 8, 8]

After adding the column:

Number of Column: [9, 9, 9, 9, 9, 9, 9, 9, 9, 9, 9, 9, 9, 9, 9, 9, 9, 9, 9, 9, 9, 9, 9, 9, 9]Low Price

change_in_close_price_str = '% Change in Low Price'

reference_column = 'Low'

print('Before adding the column:')

print('Number of Column: ', [len(tech_company[1].columns) for tech_company in tech_companies])

for tech_company in tech_companies:

temp = tech_company[1]

temp[change_in_close_price_str] = (temp[reference_column] - temp[reference_column].shift(1))/temp[reference_column].shift(1)

tech_company[1][change_in_close_price_str] = temp[change_in_close_price_str]

print()

print('After adding the column:')

print('Number of Column: ', [len(tech_company[1].columns) for tech_company in tech_companies])Before adding the column:

Number of Column: [9, 9, 9, 9, 9, 9, 9, 9, 9, 9, 9, 9, 9, 9, 9, 9, 9, 9, 9, 9, 9, 9, 9, 9, 9]

After adding the column:

Number of Column: [10, 10, 10, 10, 10, 10, 10, 10, 10, 10, 10, 10, 10, 10, 10, 10, 10, 10, 10, 10, 10, 10, 10, 10, 10]High Price

change_in_close_price_str = '% Change in High Price'

reference_column = 'High'

print('Before adding the column:')

print('Number of Column: ', [len(tech_company[1].columns) for tech_company in tech_companies])

for tech_company in tech_companies:

temp = tech_company[1]

temp[change_in_close_price_str] = (temp[reference_column] - temp[reference_column].shift(1))/temp[reference_column].shift(1)

tech_company[1][change_in_close_price_str] = temp[change_in_close_price_str]

print()

print('After adding the column:')

print('Number of Column: ', [len(tech_company[1].columns) for tech_company in tech_companies])Before adding the column:

Number of Column: [10, 10, 10, 10, 10, 10, 10, 10, 10, 10, 10, 10, 10, 10, 10, 10, 10, 10, 10, 10, 10, 10, 10, 10, 10]

After adding the column:

Number of Column: [11, 11, 11, 11, 11, 11, 11, 11, 11, 11, 11, 11, 11, 11, 11, 11, 11, 11, 11, 11, 11, 11, 11, 11, 11]tech_companies[0][1] Open High Low Close \

Datetime

2021-02-18 09:30:00-05:00 129.199997 129.679993 127.410004 128.119904

2021-02-18 10:30:00-05:00 128.100006 129.104996 127.830002 128.675705

2021-02-18 11:30:00-05:00 128.669998 128.710007 127.900002 128.620102

2021-02-18 12:30:00-05:00 128.625000 129.070007 128.449997 128.994995

2021-02-18 13:30:00-05:00 129.000000 129.050003 128.449997 128.710007

... ... ... ... ...

2024-01-11 11:30:00-05:00 184.184998 184.449997 183.835007 184.050003

2024-01-11 12:30:00-05:00 184.074997 184.777206 184.074997 184.654999

2024-01-11 13:30:00-05:00 184.669998 185.539993 184.559998 185.514999

2024-01-11 14:30:00-05:00 185.520004 185.699997 184.755005 185.369995

2024-01-11 15:30:00-05:00 185.369995 185.559998 185.350006 185.370102

Volume Dividends Stock Splits \

Datetime

2021-02-18 09:30:00-05:00 28938326 0.0 0.0

2021-02-18 10:30:00-05:00 13477687 0.0 0.0

2021-02-18 11:30:00-05:00 12770713 0.0 0.0

2021-02-18 12:30:00-05:00 8465690 0.0 0.0

2021-02-18 13:30:00-05:00 8516504 0.0 0.0

... ... ... ...

2024-01-11 11:30:00-05:00 3849444 0.0 0.0

2024-01-11 12:30:00-05:00 4000614 0.0 0.0

2024-01-11 13:30:00-05:00 3924789 0.0 0.0

2024-01-11 14:30:00-05:00 4502053 0.0 0.0

2024-01-11 15:30:00-05:00 1503923 0.0 0.0

% Change in Close Price % Change in Open Price \

Datetime

2021-02-18 09:30:00-05:00 NaN NaN

2021-02-18 10:30:00-05:00 4.338135e-03 -0.008514

2021-02-18 11:30:00-05:00 -4.321175e-04 0.004450

2021-02-18 12:30:00-05:00 2.914732e-03 -0.000350

2021-02-18 13:30:00-05:00 -2.209298e-03 0.002915

... ... ...

2024-01-11 11:30:00-05:00 -7.600814e-04 -0.000976

2024-01-11 12:30:00-05:00 3.287127e-03 -0.000597

2024-01-11 13:30:00-05:00 4.657337e-03 0.003232

2024-01-11 14:30:00-05:00 -7.816310e-04 0.004603

2024-01-11 15:30:00-05:00 5.762072e-07 -0.000809

% Change in Low Price % Change in High Price

Datetime

2021-02-18 09:30:00-05:00 NaN NaN

2021-02-18 10:30:00-05:00 0.003296 -0.004434

2021-02-18 11:30:00-05:00 0.000548 -0.003059

2021-02-18 12:30:00-05:00 0.004300 0.002797

2021-02-18 13:30:00-05:00 0.000000 -0.000155

... ... ...

2024-01-11 11:30:00-05:00 0.000000 -0.002326

2024-01-11 12:30:00-05:00 0.001305 0.001774

2024-01-11 13:30:00-05:00 0.002635 0.004128

2024-01-11 14:30:00-05:00 0.001057 0.000862

2024-01-11 15:30:00-05:00 0.003220 -0.000754

[5094 rows x 11 columns]Choosing Companies

Due to time and scope constraints we will be selecting the top three companies to further explore and perform implementation in the later parts of the coursework. The condition for picking out three companies is that these companies will need to provide the most opportunity to make a return. Therefore we look for companies not only with large price movements but also with high frequency of those movements. We need to establish that we will only be looking into buying shares or entering a long position. It is understood that money could also be made when the market moves downward. However the scope will be finding the highest absolute sum of percentage change in price as any direction is an opportunity to generate returns. We will limit our analysis to making returns when the market is going up.

Because our data is already processed to represent price movement there are several ways we can approach this.

- The sum of percentage change in price to see which company would have the highest net positive movement.

- The number of positive percentage changes in price to see which company would have the most frequent number of positive movements.

- The sum of positive percentage change in price to see which company would have the highest positive movement.

- The sum of the differences between high and low price.

- The sum of the differences between high and close price.

- The sum of the differences between low and close price.

We will be settling on using total positive percentage change.

We will also be comparing this to the approach of using standard deviation of the stock price. Standard deviation usually represents the volatility of a financial instrument and also risk. Therefore a stock with a higher standard deviation is what we would like to pick.

tech_companies[0][1]['% Change in Close Price']Datetime

2021-02-18 09:30:00-05:00 NaN

2021-02-18 10:30:00-05:00 4.338135e-03

2021-02-18 11:30:00-05:00 -4.321175e-04

2021-02-18 12:30:00-05:00 2.914732e-03

2021-02-18 13:30:00-05:00 -2.209298e-03

...

2024-01-11 11:30:00-05:00 -7.600814e-04

2024-01-11 12:30:00-05:00 3.287127e-03

2024-01-11 13:30:00-05:00 4.657337e-03

2024-01-11 14:30:00-05:00 -7.816310e-04

2024-01-11 15:30:00-05:00 5.762072e-07

Name: % Change in Close Price, Length: 5094, dtype: float64tech_companies_ticker = [tech_company[0] for tech_company in tech_companies]

companies_df = pd.DataFrame(index = tech_companies_ticker)

companies_dfEmpty DataFrame

Columns: []

Index: [AAPL, ADI, ADSK, AMD, ANSS, ASML, AVGO, CDW, CRWD, CTSH, DASH, DDOG, GOOG, GOOGL, KLAC, LRCX, MDB, META, MSFT, NVDA, NXPI, PANW, PDD, QCOM, TXN]Sum of % Positive Close Price Changes

sum_of_positive_changes_str = 'Sum of Positive Close Price Changes'

companies_df[sum_of_positive_changes_str] = None

for tech_company in tech_companies:

companies_df.loc[tech_company[0], sum_of_positive_changes_str] = sum(

list(filter(lambda x: x > 0, tech_company[1]['% Change in Close Price'][1:]))

)

companies_df Sum of Positive Close Price Changes

AAPL 10.784127

ADI 12.092185

ADSK 13.781926

AMD 19.563814

ANSS 12.933404

ASML 14.493156

AVGO 12.797733

CDW 10.444991

CRWD 20.581841

CTSH 9.911096

DASH 24.763219

DDOG 23.552644

GOOG 11.539979

GOOGL 11.683878

KLAC 15.823952

LRCX 16.54264

MDB 25.052964

META 15.01839

MSFT 10.795445

NVDA 20.052809

NXPI 15.32139

PANW 15.20349

PDD 24.920476

QCOM 13.922156

TXN 10.838171Sum of % Change in Price

sum_of_changes_str = 'Sum of Close Price Changes'

companies_df[sum_of_changes_str] = None

for tech_company in tech_companies:

companies_df.loc[tech_company[0], sum_of_changes_str] = sum(tech_company[1]['% Change in Close Price'][1:])

companies_df Sum of Positive Close Price Changes Sum of Close Price Changes

AAPL 10.784127 0.475806

ADI 12.092185 0.316209

ADSK 13.781926 0.002792

AMD 19.563814 0.867206

ANSS 12.933404 0.087076

ASML 14.493156 0.437682

AVGO 12.797733 0.975791

CDW 10.444991 0.43849

CRWD 20.581841 0.647721

CTSH 9.911096 0.105226

DASH 24.763219 0.055267

DDOG 23.552644 0.787556

GOOG 11.539979 0.442579

GOOGL 11.683878 0.439984

KLAC 15.823952 0.775045

LRCX 16.54264 0.544324

MDB 25.052964 0.714716

META 15.01839 0.625347

MSFT 10.795445 0.57566

NVDA 20.052809 1.695652

NXPI 15.32139 0.346168

PANW 15.20349 1.153684

PDD 24.920476 0.707896

QCOM 13.922156 0.1617

TXN 10.838171 0.051368Average Gap between Low and High

average_gap_str = 'Average Gap (High - Low)'

companies_df[average_gap_str] = None

for tech_company in tech_companies:

companies_df.loc[tech_company[0], average_gap_str] = sum((tech_company[1]['High'][1:] - tech_company[1]['Low'][1:]) / tech_company[1]['Low'][1:] ) / len(tech_company[1][1:])

companies_df Sum of Positive Close Price Changes Sum of Close Price Changes \

AAPL 10.784127 0.475806

ADI 12.092185 0.316209

ADSK 13.781926 0.002792

AMD 19.563814 0.867206

ANSS 12.933404 0.087076

ASML 14.493156 0.437682

AVGO 12.797733 0.975791

CDW 10.444991 0.43849

CRWD 20.581841 0.647721

CTSH 9.911096 0.105226

DASH 24.763219 0.055267

DDOG 23.552644 0.787556

GOOG 11.539979 0.442579

GOOGL 11.683878 0.439984

KLAC 15.823952 0.775045

LRCX 16.54264 0.544324

MDB 25.052964 0.714716

META 15.01839 0.625347

MSFT 10.795445 0.57566

NVDA 20.052809 1.695652

NXPI 15.32139 0.346168

PANW 15.20349 1.153684

PDD 24.920476 0.707896

QCOM 13.922156 0.1617

TXN 10.838171 0.051368

Average Gap (High - Low)

AAPL 0.007524

ADI 0.008492

ADSK 0.009741

AMD 0.013881

ANSS 0.008775

ASML 0.008735

AVGO 0.008587

CDW 0.007192

CRWD 0.01487

CTSH 0.006904

DASH 0.018389

DDOG 0.016879

GOOG 0.007889

GOOGL 0.008093

KLAC 0.010719

LRCX 0.011346

MDB 0.017585

META 0.010453

MSFT 0.007331

NVDA 0.013883

NXPI 0.010598

PANW 0.010641

PDD 0.016798

QCOM 0.009806

TXN 0.007737Standard Deviation

columns = tech_companies[0][1].columns

index = [tech_company[0] for tech_company in tech_companies]

companies_standard_deviations = pd.DataFrame(columns=columns, index=index)

for tech_company in tech_companies:

companies_standard_deviations.loc[tech_company[0]] = tech_company[1].std()

companies_standard_deviations = companies_standard_deviations.sort_values(['% Change in Close Price'], ascending=False).drop(columns=['Volume', 'Dividends', 'Stock Splits'])

companies_standard_deviations Open High Low Close % Change in Close Price \

PDD 32.080006 32.23114 31.915326 32.064646 0.019483

MDB 98.760671 99.268854 98.228868 98.727557 0.01708

DASH 50.425317 50.804168 50.037054 50.409624 0.01612

DDOG 30.319219 30.608159 30.01792 30.30877 0.015823

CRWD 47.528904 47.749702 47.289229 47.527375 0.013231

NVDA 114.239468 114.743463 113.70487 114.22924 0.012289

AMD 22.272153 22.431132 22.100393 22.267683 0.011628

META 80.131509 80.260925 79.970756 80.126257 0.01079

LRCX 96.648191 96.664046 96.555595 96.629964 0.010065

PANW 45.515648 45.717731 45.370409 45.561569 0.009816

KLAC 70.415159 70.490377 70.373619 70.452785 0.009329

ASML 101.669561 101.570227 101.722034 101.663423 0.009292

NXPI 21.07974 21.067232 21.073547 21.079791 0.009153

ADSK 42.976498 43.041587 42.898398 42.968848 0.008853

QCOM 19.359434 19.527088 19.197413 19.3657 0.008699

ANSS 48.050243 48.119773 47.967689 48.050613 0.008109

AVGO 165.6667 166.459976 165.076903 165.81627 0.007442

GOOGL 16.905788 16.896378 16.890284 16.892939 0.007365

GOOG 17.025381 17.013128 17.015443 17.014153 0.007266

ADI 13.984689 13.938348 14.03361 13.99286 0.007145

MSFT 39.978472 40.00587 39.961993 39.978433 0.006599

CTSH 8.970093 8.996426 8.937564 8.970886 0.006481

AAPL 19.769706 19.766775 19.782729 19.771827 0.006468

TXN 12.61352 12.58614 12.621553 12.616761 0.006416

CDW 16.664114 16.634817 16.694416 16.665404 0.006257

% Change in Open Price % Change in Low Price % Change in High Price

PDD 0.018998 0.019522 0.020066

MDB 0.017038 0.016511 0.017406

DASH 0.016489 0.016242 0.016296

DDOG 0.015958 0.015543 0.015966

CRWD 0.013339 0.013352 0.013045

NVDA 0.01249 0.011933 0.011902

AMD 0.011748 0.011282 0.01135

META 0.010954 0.010853 0.010767

LRCX 0.009959 0.009788 0.009623

PANW 0.009765 0.009607 0.009957

KLAC 0.009507 0.009162 0.009164

ASML 0.009398 0.009049 0.008881

NXPI 0.009172 0.008935 0.008639

ADSK 0.008846 0.00886 0.008613

QCOM 0.008886 0.008561 0.008529

ANSS 0.008587 0.008109 0.008235

AVGO 0.007365 0.007084 0.007253

GOOGL 0.007362 0.007163 0.007374

GOOG 0.007241 0.007052 0.006969

ADI 0.007332 0.007182 0.00674

MSFT 0.006522 0.006275 0.006274

CTSH 0.006628 0.00643 0.006285

AAPL 0.006413 0.006331 0.006053

TXN 0.006685 0.006363 0.005972

CDW 0.006454 0.006477 0.005878columns = companies_standard_deviations.columns[-4:]

companies_df[columns] = companies_standard_deviations[columns]

companies_df Sum of Positive Close Price Changes Sum of Close Price Changes \

AAPL 10.784127 0.475806

ADI 12.092185 0.316209

ADSK 13.781926 0.002792

AMD 19.563814 0.867206

ANSS 12.933404 0.087076

ASML 14.493156 0.437682

AVGO 12.797733 0.975791

CDW 10.444991 0.43849

CRWD 20.581841 0.647721

CTSH 9.911096 0.105226

DASH 24.763219 0.055267

DDOG 23.552644 0.787556

GOOG 11.539979 0.442579

GOOGL 11.683878 0.439984

KLAC 15.823952 0.775045

LRCX 16.54264 0.544324

MDB 25.052964 0.714716

META 15.01839 0.625347

MSFT 10.795445 0.57566

NVDA 20.052809 1.695652

NXPI 15.32139 0.346168

PANW 15.20349 1.153684

PDD 24.920476 0.707896

QCOM 13.922156 0.1617

TXN 10.838171 0.051368

Average Gap (High - Low) % Change in Close Price % Change in Open Price \

AAPL 0.007524 0.006468 0.006413

ADI 0.008492 0.007145 0.007332

ADSK 0.009741 0.008853 0.008846

AMD 0.013881 0.011628 0.011748

ANSS 0.008775 0.008109 0.008587

ASML 0.008735 0.009292 0.009398

AVGO 0.008587 0.007442 0.007365

CDW 0.007192 0.006257 0.006454

CRWD 0.01487 0.013231 0.013339

CTSH 0.006904 0.006481 0.006628

DASH 0.018389 0.01612 0.016489

DDOG 0.016879 0.015823 0.015958

GOOG 0.007889 0.007266 0.007241

GOOGL 0.008093 0.007365 0.007362

KLAC 0.010719 0.009329 0.009507

LRCX 0.011346 0.010065 0.009959

MDB 0.017585 0.01708 0.017038

META 0.010453 0.01079 0.010954

MSFT 0.007331 0.006599 0.006522

NVDA 0.013883 0.012289 0.01249

NXPI 0.010598 0.009153 0.009172

PANW 0.010641 0.009816 0.009765

PDD 0.016798 0.019483 0.018998

QCOM 0.009806 0.008699 0.008886

TXN 0.007737 0.006416 0.006685

% Change in Low Price % Change in High Price

AAPL 0.006331 0.006053

ADI 0.007182 0.00674

ADSK 0.00886 0.008613

AMD 0.011282 0.01135

ANSS 0.008109 0.008235

ASML 0.009049 0.008881

AVGO 0.007084 0.007253

CDW 0.006477 0.005878

CRWD 0.013352 0.013045

CTSH 0.00643 0.006285

DASH 0.016242 0.016296

DDOG 0.015543 0.015966

GOOG 0.007052 0.006969

GOOGL 0.007163 0.007374

KLAC 0.009162 0.009164

LRCX 0.009788 0.009623

MDB 0.016511 0.017406

META 0.010853 0.010767

MSFT 0.006275 0.006274

NVDA 0.011933 0.011902

NXPI 0.008935 0.008639

PANW 0.009607 0.009957

PDD 0.019522 0.020066

QCOM 0.008561 0.008529

TXN 0.006363 0.005972Any of the columns available in the DataFrame are all justifiable to be used to decide. But we will go through each of them to see which are the companies that have more price movement that others.

Comparing the columns

We will create a column to see how many points can the companies collect. The top 3 highest scorer will be chosen to be used, moving forward

companies_df['Score'] = 0

companies_df Sum of Positive Close Price Changes Sum of Close Price Changes \

AAPL 10.784127 0.475806

ADI 12.092185 0.316209

ADSK 13.781926 0.002792

AMD 19.563814 0.867206

ANSS 12.933404 0.087076

ASML 14.493156 0.437682

AVGO 12.797733 0.975791

CDW 10.444991 0.43849

CRWD 20.581841 0.647721

CTSH 9.911096 0.105226

DASH 24.763219 0.055267

DDOG 23.552644 0.787556

GOOG 11.539979 0.442579

GOOGL 11.683878 0.439984

KLAC 15.823952 0.775045

LRCX 16.54264 0.544324

MDB 25.052964 0.714716

META 15.01839 0.625347

MSFT 10.795445 0.57566

NVDA 20.052809 1.695652

NXPI 15.32139 0.346168

PANW 15.20349 1.153684

PDD 24.920476 0.707896

QCOM 13.922156 0.1617

TXN 10.838171 0.051368

Average Gap (High - Low) % Change in Close Price % Change in Open Price \

AAPL 0.007524 0.006468 0.006413

ADI 0.008492 0.007145 0.007332

ADSK 0.009741 0.008853 0.008846

AMD 0.013881 0.011628 0.011748

ANSS 0.008775 0.008109 0.008587

ASML 0.008735 0.009292 0.009398

AVGO 0.008587 0.007442 0.007365

CDW 0.007192 0.006257 0.006454

CRWD 0.01487 0.013231 0.013339

CTSH 0.006904 0.006481 0.006628

DASH 0.018389 0.01612 0.016489

DDOG 0.016879 0.015823 0.015958

GOOG 0.007889 0.007266 0.007241

GOOGL 0.008093 0.007365 0.007362

KLAC 0.010719 0.009329 0.009507

LRCX 0.011346 0.010065 0.009959

MDB 0.017585 0.01708 0.017038

META 0.010453 0.01079 0.010954

MSFT 0.007331 0.006599 0.006522

NVDA 0.013883 0.012289 0.01249

NXPI 0.010598 0.009153 0.009172

PANW 0.010641 0.009816 0.009765

PDD 0.016798 0.019483 0.018998

QCOM 0.009806 0.008699 0.008886

TXN 0.007737 0.006416 0.006685

% Change in Low Price % Change in High Price Score

AAPL 0.006331 0.006053 0

ADI 0.007182 0.00674 0

ADSK 0.00886 0.008613 0

AMD 0.011282 0.01135 0

ANSS 0.008109 0.008235 0

ASML 0.009049 0.008881 0

AVGO 0.007084 0.007253 0

CDW 0.006477 0.005878 0

CRWD 0.013352 0.013045 0

CTSH 0.00643 0.006285 0

DASH 0.016242 0.016296 0

DDOG 0.015543 0.015966 0

GOOG 0.007052 0.006969 0

GOOGL 0.007163 0.007374 0

KLAC 0.009162 0.009164 0

LRCX 0.009788 0.009623 0

MDB 0.016511 0.017406 0

META 0.010853 0.010767 0

MSFT 0.006275 0.006274 0

NVDA 0.011933 0.011902 0

NXPI 0.008935 0.008639 0

PANW 0.009607 0.009957 0

PDD 0.019522 0.020066 0

QCOM 0.008561 0.008529 0

TXN 0.006363 0.005972 0companies_df.columns[-1]'Score'# Looping through all the columns in the DataFrame

for column in companies_df.columns:

# Sorting them in descending order

companies_df = companies_df.sort_values(column,ascending=False)

# Giving a point to the top 3 companies

companies_df.iloc[:3, -1] += 1

companies_df Sum of Positive Close Price Changes Sum of Close Price Changes \

DASH 24.763219 0.055267

MDB 25.052964 0.714716

PDD 24.920476 0.707896

DDOG 23.552644 0.787556

NVDA 20.052809 1.695652

PANW 15.20349 1.153684

AVGO 12.797733 0.975791

ANSS 12.933404 0.087076

TXN 10.838171 0.051368

AAPL 10.784127 0.475806

MSFT 10.795445 0.57566

CTSH 9.911096 0.105226

ADI 12.092185 0.316209

GOOG 11.539979 0.442579

GOOGL 11.683878 0.439984

NXPI 15.32139 0.346168

QCOM 13.922156 0.1617

ADSK 13.781926 0.002792

ASML 14.493156 0.437682

KLAC 15.823952 0.775045

LRCX 16.54264 0.544324

META 15.01839 0.625347

AMD 19.563814 0.867206

CRWD 20.581841 0.647721

CDW 10.444991 0.43849

Average Gap (High - Low) % Change in Close Price % Change in Open Price \

DASH 0.018389 0.01612 0.016489

MDB 0.017585 0.01708 0.017038

PDD 0.016798 0.019483 0.018998

DDOG 0.016879 0.015823 0.015958

NVDA 0.013883 0.012289 0.01249

PANW 0.010641 0.009816 0.009765

AVGO 0.008587 0.007442 0.007365

ANSS 0.008775 0.008109 0.008587

TXN 0.007737 0.006416 0.006685

AAPL 0.007524 0.006468 0.006413

MSFT 0.007331 0.006599 0.006522

CTSH 0.006904 0.006481 0.006628

ADI 0.008492 0.007145 0.007332

GOOG 0.007889 0.007266 0.007241

GOOGL 0.008093 0.007365 0.007362

NXPI 0.010598 0.009153 0.009172

QCOM 0.009806 0.008699 0.008886

ADSK 0.009741 0.008853 0.008846

ASML 0.008735 0.009292 0.009398

KLAC 0.010719 0.009329 0.009507

LRCX 0.011346 0.010065 0.009959

META 0.010453 0.01079 0.010954

AMD 0.013881 0.011628 0.011748

CRWD 0.01487 0.013231 0.013339

CDW 0.007192 0.006257 0.006454

% Change in Low Price % Change in High Price Score

DASH 0.016242 0.016296 7

MDB 0.016511 0.017406 7

PDD 0.019522 0.020066 6

DDOG 0.015543 0.015966 1

NVDA 0.011933 0.011902 1

PANW 0.009607 0.009957 1

AVGO 0.007084 0.007253 1

ANSS 0.008109 0.008235 0

TXN 0.006363 0.005972 0

AAPL 0.006331 0.006053 0

MSFT 0.006275 0.006274 0

CTSH 0.00643 0.006285 0

ADI 0.007182 0.00674 0

GOOG 0.007052 0.006969 0

GOOGL 0.007163 0.007374 0

NXPI 0.008935 0.008639 0

QCOM 0.008561 0.008529 0

ADSK 0.00886 0.008613 0

ASML 0.009049 0.008881 0

KLAC 0.009162 0.009164 0

LRCX 0.009788 0.009623 0

META 0.010853 0.010767 0

AMD 0.011282 0.01135 0

CRWD 0.013352 0.013045 0

CDW 0.006477 0.005878 0Based on the results, we can see that ticker 'MDB', 'PDD' and 'DASH' are the winners as they scored the most.

winning_companies = ['MDB', 'PDD', 'DASH']

companies_dict = {}

for tech_company in tech_companies:

if tech_company[0] in winning_companies:

companies_dict[tech_company[0]] = tech_company[1]

companies_dict{'DASH': Open High Low Close \

Datetime

2021-02-18 09:30:00-05:00 194.300003 196.610001 188.990005 189.800003

2021-02-18 10:30:00-05:00 189.576096 194.800003 188.910004 193.691101

2021-02-18 11:30:00-05:00 193.770004 196.979996 191.339996 191.554993

2021-02-18 12:30:00-05:00 191.339996 194.490005 191.169998 193.899994

2021-02-18 13:30:00-05:00 194.149994 196.440002 193.809998 196.220001

... ... ... ... ...

2024-01-11 11:30:00-05:00 102.565002 103.139999 102.400002 102.925003

2024-01-11 12:30:00-05:00 102.959999 103.959999 102.889999 103.800003

2024-01-11 13:30:00-05:00 103.779999 104.650002 103.675003 104.625000

2024-01-11 14:30:00-05:00 104.644997 104.695000 104.065002 104.339996

2024-01-11 15:30:00-05:00 104.320000 104.330002 104.029999 104.100098

Volume Dividends Stock Splits \

Datetime

2021-02-18 09:30:00-05:00 410371 0.0 0.0

2021-02-18 10:30:00-05:00 270042 0.0 0.0

2021-02-18 11:30:00-05:00 270798 0.0 0.0

2021-02-18 12:30:00-05:00 185655 0.0 0.0

2021-02-18 13:30:00-05:00 108898 0.0 0.0

... ... ... ...

2024-01-11 11:30:00-05:00 226748 0.0 0.0

2024-01-11 12:30:00-05:00 230721 0.0 0.0

2024-01-11 13:30:00-05:00 270964 0.0 0.0

2024-01-11 14:30:00-05:00 247590 0.0 0.0

2024-01-11 15:30:00-05:00 87951 0.0 0.0

% Change in Close Price % Change in Open Price \

Datetime

2021-02-18 09:30:00-05:00 NaN NaN

2021-02-18 10:30:00-05:00 0.020501 -0.024312

2021-02-18 11:30:00-05:00 -0.011028 0.022123

2021-02-18 12:30:00-05:00 0.012242 -0.012541

2021-02-18 13:30:00-05:00 0.011965 0.014686

... ... ...

2024-01-11 11:30:00-05:00 0.003559 -0.012088

2024-01-11 12:30:00-05:00 0.008501 0.003851

2024-01-11 13:30:00-05:00 0.007948 0.007964

2024-01-11 14:30:00-05:00 -0.002724 0.008335

2024-01-11 15:30:00-05:00 -0.002299 -0.003106

% Change in Low Price % Change in High Price

Datetime

2021-02-18 09:30:00-05:00 NaN NaN

2021-02-18 10:30:00-05:00 -0.000423 -0.009206

2021-02-18 11:30:00-05:00 0.012863 0.011191

2021-02-18 12:30:00-05:00 -0.000888 -0.012641

2021-02-18 13:30:00-05:00 0.013810 0.010026

... ... ...

2024-01-11 11:30:00-05:00 -0.001073 -0.011596

2024-01-11 12:30:00-05:00 0.004785 0.007950

2024-01-11 13:30:00-05:00 0.007630 0.006637

2024-01-11 14:30:00-05:00 0.003762 0.000430

2024-01-11 15:30:00-05:00 -0.000336 -0.003486

[5094 rows x 11 columns],

'MDB': Open High Low Close \

Datetime

2021-02-18 09:30:00-05:00 402.079987 409.820007 397.397491 398.625000

2021-02-18 10:30:00-05:00 399.190002 407.035004 397.420013 404.570007

2021-02-18 11:30:00-05:00 405.480011 405.480011 401.940002 403.084991

2021-02-18 12:30:00-05:00 403.019989 404.109985 398.540009 403.070007

2021-02-18 13:30:00-05:00 402.799988 403.959991 402.029999 402.489990

... ... ... ... ...

2024-01-11 11:30:00-05:00 385.250000 387.010010 383.200012 383.899994

2024-01-11 12:30:00-05:00 384.160004 390.000000 384.010010 389.619995

2024-01-11 13:30:00-05:00 389.559998 393.489990 389.006989 392.549988

2024-01-11 14:30:00-05:00 392.679993 393.129913 391.830109 392.720001

2024-01-11 15:30:00-05:00 392.829987 393.519989 392.470001 393.494995

Volume Dividends Stock Splits \

Datetime

2021-02-18 09:30:00-05:00 108932 0.0 0.0

2021-02-18 10:30:00-05:00 59993 0.0 0.0

2021-02-18 11:30:00-05:00 41952 0.0 0.0

2021-02-18 12:30:00-05:00 79363 0.0 0.0

2021-02-18 13:30:00-05:00 59128 0.0 0.0

... ... ... ...

2024-01-11 11:30:00-05:00 133670 0.0 0.0

2024-01-11 12:30:00-05:00 90468 0.0 0.0

2024-01-11 13:30:00-05:00 112940 0.0 0.0

2024-01-11 14:30:00-05:00 102012 0.0 0.0

2024-01-11 15:30:00-05:00 45298 0.0 0.0

% Change in Close Price % Change in Open Price \

Datetime

2021-02-18 09:30:00-05:00 NaN NaN

2021-02-18 10:30:00-05:00 0.014914 -0.007188

2021-02-18 11:30:00-05:00 -0.003671 0.015757

2021-02-18 12:30:00-05:00 -0.000037 -0.006067

2021-02-18 13:30:00-05:00 -0.001439 -0.000546

... ... ...

2024-01-11 11:30:00-05:00 -0.003375 -0.009691

2024-01-11 12:30:00-05:00 0.014900 -0.002829

2024-01-11 13:30:00-05:00 0.007520 0.014057

2024-01-11 14:30:00-05:00 0.000433 0.008009

2024-01-11 15:30:00-05:00 0.001973 0.000382

% Change in Low Price % Change in High Price

Datetime

2021-02-18 09:30:00-05:00 NaN NaN

2021-02-18 10:30:00-05:00 0.000057 -0.006796

2021-02-18 11:30:00-05:00 0.011373 -0.003820

2021-02-18 12:30:00-05:00 -0.008459 -0.003379

2021-02-18 13:30:00-05:00 0.008757 -0.000371

... ... ...

2024-01-11 11:30:00-05:00 -0.005192 -0.009457

2024-01-11 12:30:00-05:00 0.002114 0.007726

2024-01-11 13:30:00-05:00 0.013013 0.008949

2024-01-11 14:30:00-05:00 0.007257 -0.000915

2024-01-11 15:30:00-05:00 0.001633 0.000992

[5094 rows x 11 columns],

'PDD': Open High Low Close \

Datetime

2021-02-18 09:30:00-05:00 198.000000 199.309998 192.899994 194.009995

2021-02-18 10:30:00-05:00 194.000000 196.000000 193.875000 195.100006

2021-02-18 11:30:00-05:00 195.000000 195.578003 193.100006 193.845001

2021-02-18 12:30:00-05:00 193.820007 195.544998 192.029999 195.220001

2021-02-18 13:30:00-05:00 195.179993 195.699997 194.660004 195.070007

... ... ... ... ...

2024-01-11 11:30:00-05:00 150.289993 151.050003 149.949997 150.550003

2024-01-11 12:30:00-05:00 150.554993 151.339996 150.475006 151.070007

2024-01-11 13:30:00-05:00 151.085007 151.630005 151.050003 151.539993

2024-01-11 14:30:00-05:00 151.559998 151.774994 151.430099 151.580994

2024-01-11 15:30:00-05:00 151.589996 151.720001 151.483994 151.649994

Volume Dividends Stock Splits \

Datetime

2021-02-18 09:30:00-05:00 1851955 0.0 0.0

2021-02-18 10:30:00-05:00 633548 0.0 0.0

2021-02-18 11:30:00-05:00 305243 0.0 0.0

2021-02-18 12:30:00-05:00 521230 0.0 0.0

2021-02-18 13:30:00-05:00 185892 0.0 0.0

... ... ... ...

2024-01-11 11:30:00-05:00 437558 0.0 0.0

2024-01-11 12:30:00-05:00 321022 0.0 0.0

2024-01-11 13:30:00-05:00 361665 0.0 0.0

2024-01-11 14:30:00-05:00 449250 0.0 0.0

2024-01-11 15:30:00-05:00 155503 0.0 0.0

% Change in Close Price % Change in Open Price \

Datetime

2021-02-18 09:30:00-05:00 NaN NaN

2021-02-18 10:30:00-05:00 0.005618 -0.020202

2021-02-18 11:30:00-05:00 -0.006433 0.005155

2021-02-18 12:30:00-05:00 0.007093 -0.006051

2021-02-18 13:30:00-05:00 -0.000768 0.007017

... ... ...

2024-01-11 11:30:00-05:00 0.001830 -0.006249

2024-01-11 12:30:00-05:00 0.003454 0.001763

2024-01-11 13:30:00-05:00 0.003111 0.003520

2024-01-11 14:30:00-05:00 0.000271 0.003144

2024-01-11 15:30:00-05:00 0.000455 0.000198

% Change in Low Price % Change in High Price

Datetime

2021-02-18 09:30:00-05:00 NaN NaN

2021-02-18 10:30:00-05:00 0.005054 -0.016607

2021-02-18 11:30:00-05:00 -0.003997 -0.002153

2021-02-18 12:30:00-05:00 -0.005541 -0.000169

2021-02-18 13:30:00-05:00 0.013696 0.000793

... ... ...

2024-01-11 11:30:00-05:00 0.000801 -0.003529

2024-01-11 12:30:00-05:00 0.003501 0.001920

2024-01-11 13:30:00-05:00 0.003821 0.001916

2024-01-11 14:30:00-05:00 0.002516 0.000956

2024-01-11 15:30:00-05:00 0.000356 -0.000362

[5094 rows x 11 columns]}Including Gap

As done above, we explored that the average gap between the high and low prices can also be an indication of price movement. Because our final dataset will be using change in price, the information about the difference between the high price and low price will be lost. Therefore, we should add a column that mentions the gap. Similarly, because the gap is based on the price, it shares the same issue as every price related column. But percentage change of the gap also does not convey the gap in price. Therefore, we will be using gap (difference between high and low) divided by the low price. Therefore, the gap is shown in percentage form.

companies_dict['MDB'].columnsIndex(['Open', 'High', 'Low', 'Close', 'Volume', 'Dividends', 'Stock Splits',

'% Change in Close Price', '% Change in Open Price',

'% Change in Low Price', '% Change in High Price'],

dtype='object')for company in winning_companies:

companies_dict[company]['Gap'] = (companies_dict[company]['High'] - companies_dict[company]['Low']) / companies_dict[company]['Low']

print(companies_dict[company]['Gap'])Datetime

2021-02-18 09:30:00-05:00 0.031260

2021-02-18 10:30:00-05:00 0.024194

2021-02-18 11:30:00-05:00 0.008807

2021-02-18 12:30:00-05:00 0.013976

2021-02-18 13:30:00-05:00 0.004801

...

2024-01-11 11:30:00-05:00 0.009943

2024-01-11 12:30:00-05:00 0.015599

2024-01-11 13:30:00-05:00 0.011524

2024-01-11 14:30:00-05:00 0.003317

2024-01-11 15:30:00-05:00 0.002675

Name: Gap, Length: 5094, dtype: float64

Datetime

2021-02-18 09:30:00-05:00 0.033230

2021-02-18 10:30:00-05:00 0.010961

2021-02-18 11:30:00-05:00 0.012833

2021-02-18 12:30:00-05:00 0.018304

2021-02-18 13:30:00-05:00 0.005343

...

2024-01-11 11:30:00-05:00 0.007336

2024-01-11 12:30:00-05:00 0.005748

2024-01-11 13:30:00-05:00 0.003840

2024-01-11 14:30:00-05:00 0.002278

2024-01-11 15:30:00-05:00 0.001558

Name: Gap, Length: 5094, dtype: float64

Datetime

2021-02-18 09:30:00-05:00 0.040320

2021-02-18 10:30:00-05:00 0.031179

2021-02-18 11:30:00-05:00 0.029476

2021-02-18 12:30:00-05:00 0.017367

2021-02-18 13:30:00-05:00 0.013570

...

2024-01-11 11:30:00-05:00 0.007227

2024-01-11 12:30:00-05:00 0.010399

2024-01-11 13:30:00-05:00 0.009404

2024-01-11 14:30:00-05:00 0.006054

2024-01-11 15:30:00-05:00 0.002884

Name: Gap, Length: 5094, dtype: float64Datetime Features

We will now be extracting the datetime features. This is because they might be repeating patterns within the datetime that are might not be obvious to us. For example, it may be most volatile during Tuesday, 2pm to 4pm, when there change in close of at least 3%. Therefore, extracting these features will allow the machine learning model to identify patterns as mentioned.

companies_dict['DASH'] Open High Low Close \

Datetime

2021-02-18 09:30:00-05:00 194.300003 196.610001 188.990005 189.800003

2021-02-18 10:30:00-05:00 189.576096 194.800003 188.910004 193.691101

2021-02-18 11:30:00-05:00 193.770004 196.979996 191.339996 191.554993

2021-02-18 12:30:00-05:00 191.339996 194.490005 191.169998 193.899994