Abstract

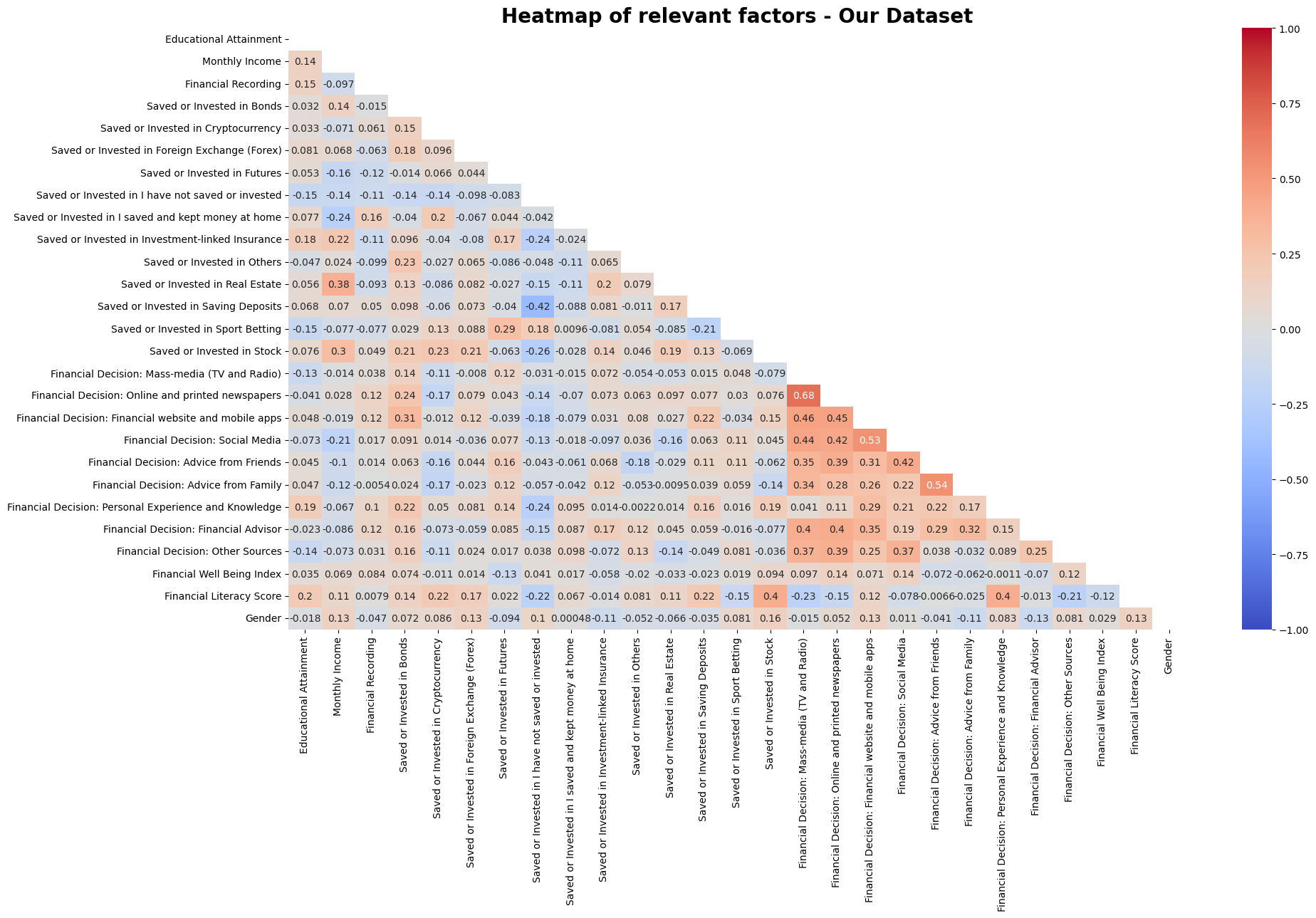

In this project, we compared a dataset from Romania with our own collected dataset from Malaysia. We explored how different factors like age, income, and education affect a person's financial literacy and financial well-being. We found that while things like education and income usually predict financial skills, our dataset showed some different and interesting behaviors. For example, we noticed that people with high income and high financial literacy in our group actually prefer 'mental tracking' instead of keeping strict records. We also found that even though our group had higher financial literacy scores, it didn't necessarily mean they had higher financial well-being scores compared to the Romanian group. We also observed that the financial well-being for our dataset didn't hit the 'universal security' levels that were seen in the Romanian dataset.

There is also a part 2 of this project, where we use the same romanian and self-surveyed dataset, along with a Ghanaians dataset, to also explore the relationship of sociodemographic and financial factors, in the participation of Higher Risk Financial Vehicle such as sport-betting, cryptocurrency, derivatives, forex, etc.

Research Topic

Topic of Investigation

Financial literacy has been a popular topic to explore, which can be seen in the number of publications and researches increasing year over year, as shown in this bibliographic analysis by Goyal and Kumar (2021). The aim of the research is to explore the relationship of between sociodemographic attributes and financial literacy and their effect on financial well-being and the avoidance of higher-risk financial vehicle (HRFV). In this study, a questionnaire survey will be conducted, as existing literature review have demonstrated the positive impact of financial literacy on financial well-being, as discussed in later sections. As for the aspect of avoiding risk financial, this will be the additional contribution to the study of financial literacy and also to understand if financial literacy makes an individual avoid higher-risk financial vehicles (HRFV) or encourage them to utilize it due to their better understanding of associated risks and financial management, such as the study by Ofosu and Kotey (2019).

This project is inspired by Nițoi et al. (2022) as the questionnaire from this study will be adopted, but focuses on target demographic of university students and working adults of Malaysians residing in Kuala Lumpur. The result of the project by Nițoi et al. (2022) will be used as data source for comparison against the outcome of this project. Additional questions to the questionnaire will be added to further explore the avoidance of HRFV, and will be compared to other existing studies such as the study by Ofosu and Kotey, (2019).

Background Research

Sociodemographic Attributes, Financial Literacy and Financial Well-Being

The findings in several studies, such as Zulfiqar and Bilal (2016), Zhang and Chatterjee (2023), Akhter and Sangmi (2016), have demonstrated a positive relationship between financial literacy and financial well-being. This is because financial literacy equips individuals with the skills to effectively plan and manage their finances, which reduces stress and anxiety that could be caused by unforeseen circumstances. These findings also emphasize the importance of policymakers, regulators, governments and educators taking proactive measures to improve and elevate financial literacy for everyone through educational program. As emphasized by Zhang and Chatterjee (2023), “it is never too late to educate individuals on financial literacy”.

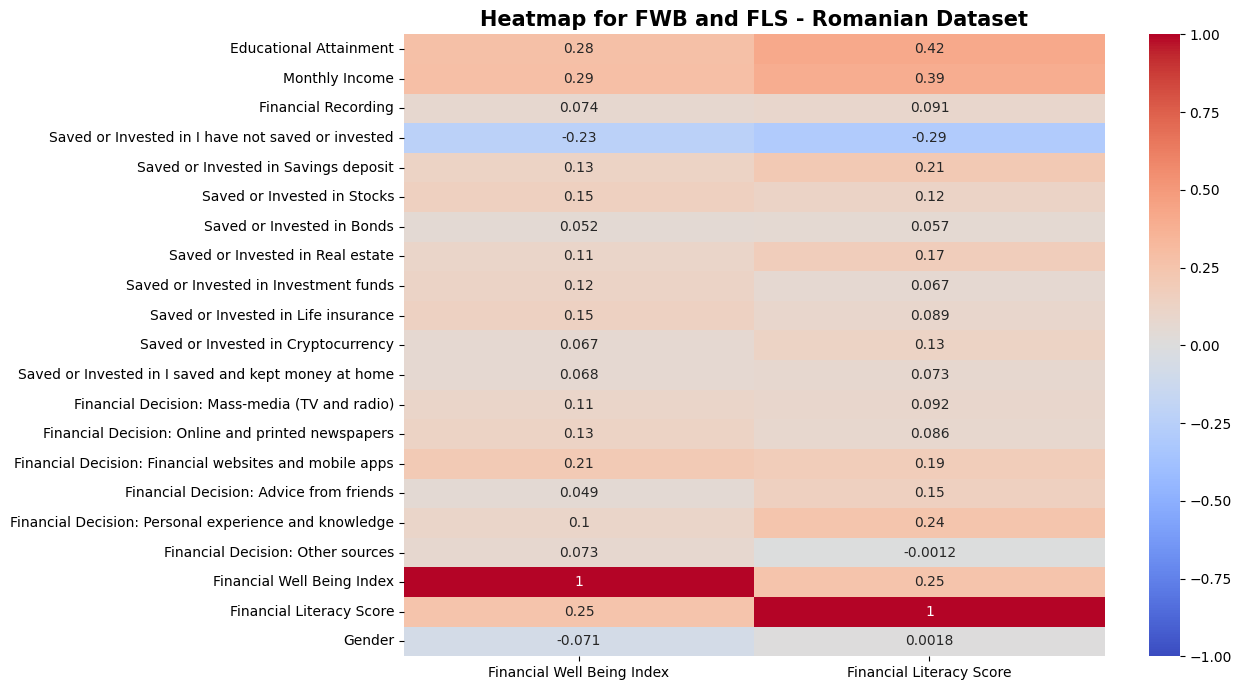

This project will utilize a dataset (secondary data) from a study conducted in Romania, Nițoi et al. (2022). The study highlighted that 92% of the 1391 respondents in the questionnaire survey were financially illiterate. Results also indicated that only 15% felt financially secured, 35% had a moderately stable financial situation, 38% struggled to meet their financial needs, and the remaining 13% experienced significant financial insecurity. Income levels, age and education were identified as influential factors in determining financial well-being, while gender and residential status exhibited no significant impact. Furthermore, the study also noted that individuals with higher financial literacy, have above-average financial well-being.

Numerous studies have been conducted in Malaysia, in a variety of areas of financial literacy. Despite their limited citation, they offer valuable insights in a local perspective. For instance, in a study conducted by Kah et al. (2021), it was identified that sociodemographic attributes, including income, age and education level, along with financial literacy, played significant roles in the engagement of financial planning. This engagement in turn, results in achieving good financial well-being. Similarly, Ali et al. (2015) concluded that financial literacy was a crucial determinant for basic money management and financial planning, which are essential steps toward financial well-being. Notably, over 60% of the sampled Malaysian demonstrated moderately high levels of financial literacy. Furthermore, a study by Rahman et al. (2021) examined the financial well-being, financial stress, and financial literacy as variables. The results indicated that all three variables were statistically significant. Therefore, this project will explore into the relationship between sociodemographic attributes, financial literacy and financial well-being.

Operational Definitions

Financial Literacy

Nițoi et al., (2022) has adopted standardized approach for measuring financial literacy from a widely cited study by Lusardi and Mitchell, (2009) , where they have established a set of basic and advanced questions to assess an individuals’ financial literacy. This project will be using the same sets of questions and scoring to ensure comparability with the dataset from Nițoi et al., (2022).

Finacnial Well-Being

Nițoi et al., (2022) utilized the Consumer Financial Protection Bureau (CFPB)’s financial well-being questionnaire and scoring method to measure financial well-being. This widely accepted approach will be applied in this project as to ensure comparability with the dataset from Nițoi et al., (2022).

Research Objectives

- To understand the influence of sociodemographic attributes to financial literacy and financial well-being.

- To understand the relationship between financial literacy and financial well-being

Research Questions

- What are sociodemographic conditions that affect the financial literacy and financial well-being of an individual?

- Does possessing financial literacy lead to financial well-being?

Data Collection & Survey Design

Population and Sample

Based on data on Statista (2023), in the year 2020, there are around 500,000 students in university, and in year 2022, there were approximately 15 million that working adults (age range from 15 to 64). Because the population size is so large, and there is no data available to further narrow the scope to only university student and early working adults. Based on the calculation for ideal sample size, if at confidence level of 95% with margin of error of 5% and population of 50%, the sample size would be 385. Because the questionnaire survey that was made and the short time frame of this project, even at the margin of error of 10%, the sample size required is still 97. The goal for this project, is to get 97 to 385 responses.

In the end, the survey was able to reach about 144 response. We used Jisc Online Surveys, as it was required for the project. We have also employed word of mouth or similarly, snowball sampling. This was the easiest way, given the resource and time constraint for the given project. This method of data collection also has its downsides, such as having bias to the data. This is because, people around us are highly likely to have some form of similarity in characteristics, financial status and demographic traits with us. There is also a risk of data inaccuracy as participants might not take the survey as seriously. For our case, the demographic was supposed to be targeted to younger adults from 18 to 35 years old. But because of this method of collecting data, we ended up having a wide range of ages in the survey, which we will explore in the later sections.

The survey was available for participants for the month of September. We also gave the option for survey participants to claim an optional RM3 / £0.50 / US$0.63. Additionally, the response rate for the survey is 48%, about half of the participants completed the survey.

External Data Source

The project will be using a dataset from a study from Romania Nițoi et al. (2022), where a survey was conducted in regards to financial literacy and financial well-being. It was the only few full datasets which included the questionnaire and the data for a direct comparison.

We will be using an external dataset from the Romanian study, , which can be downloaded in the link of their paper, it contains all the relevant links to the paper, and for the dataset.

Another set of paper that we will be making comparison to is the Ghanaian study, Ofosu and Kotey, (2019). Note that a direct comparison between Ghana and Malaysia may not be entirely equal due to their differing financial situations. For instance, in 2021, Ghana’s GDP stood at US$77 billion while Malaysia’s GDP reached nearly US$373 billion, according to data from the World Bank, (2023). Although GDP alone does not fully reflect a country’s financial situation, it is often used as a quick indicator.

Key Findings

The key findings are:

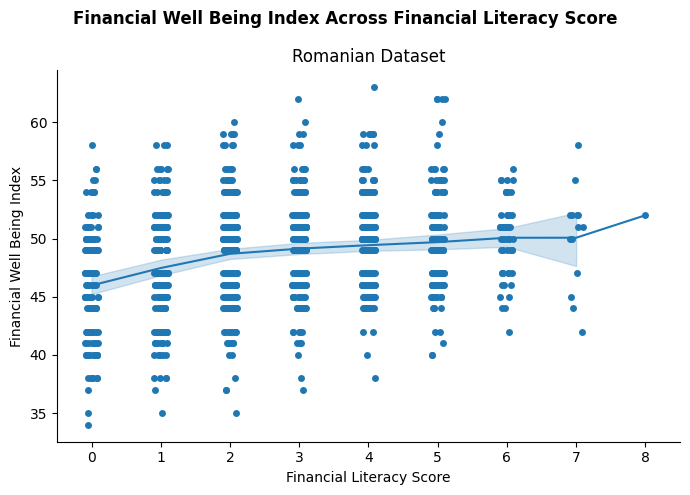

Does High Financial Literacy mean High Financial Well-Being?

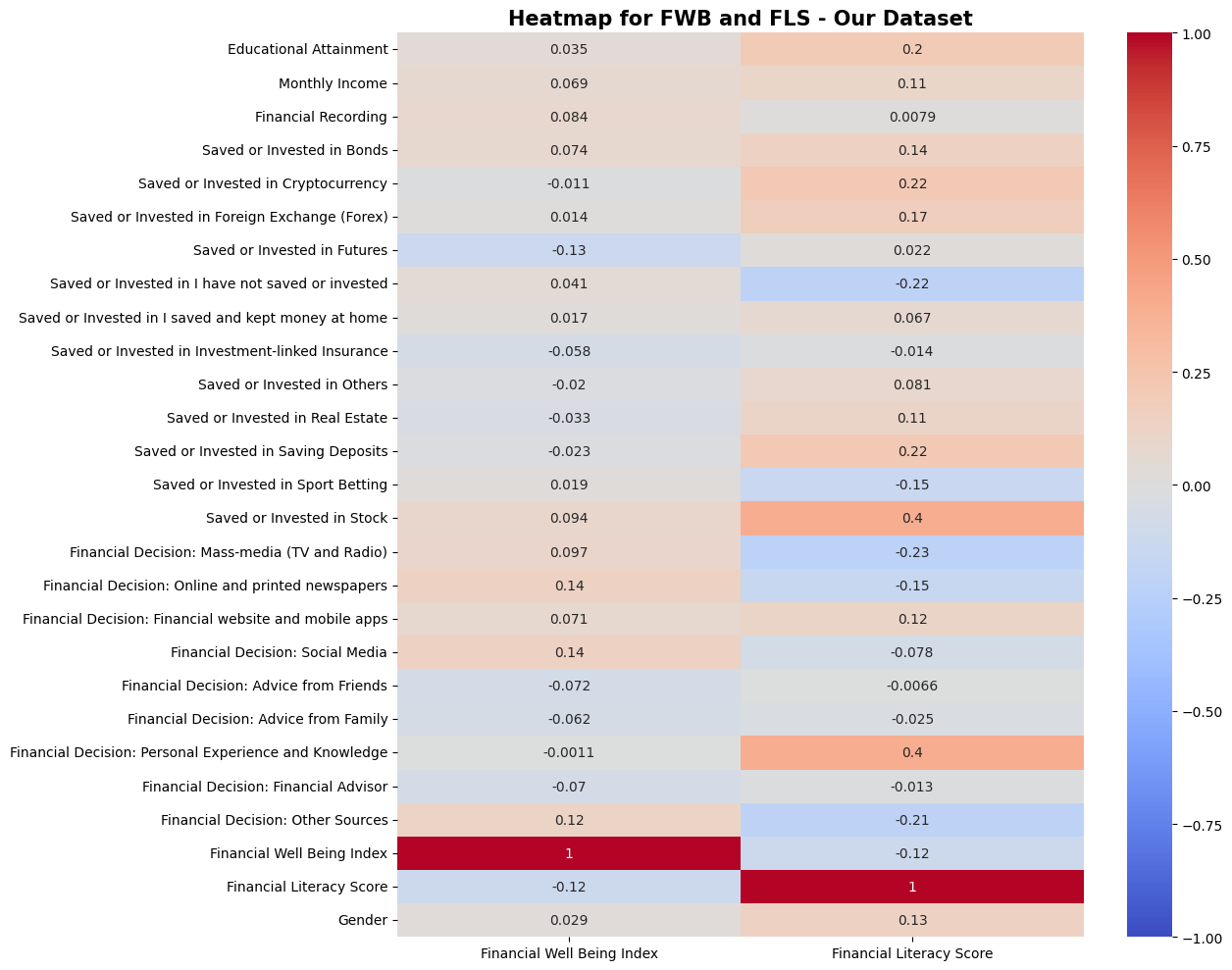

We found that our dataset had higher average financial literacy scores (peaking at 4 out of 8) compared to the Romanian dataset (peaking at 2 out of 8). However, having a higher score did not mean having better financial well-being. In fact, we saw that financial well-being scores for our dataset were capped at around 57.5, while the Romanian dataset had scores going above 70, reaching 'universal security' levels. Ironically, we also found a weak negative correlation (-0.12) between financial literacy and financial well-being in our dataset.

Do High Earners Keep Strict Records?

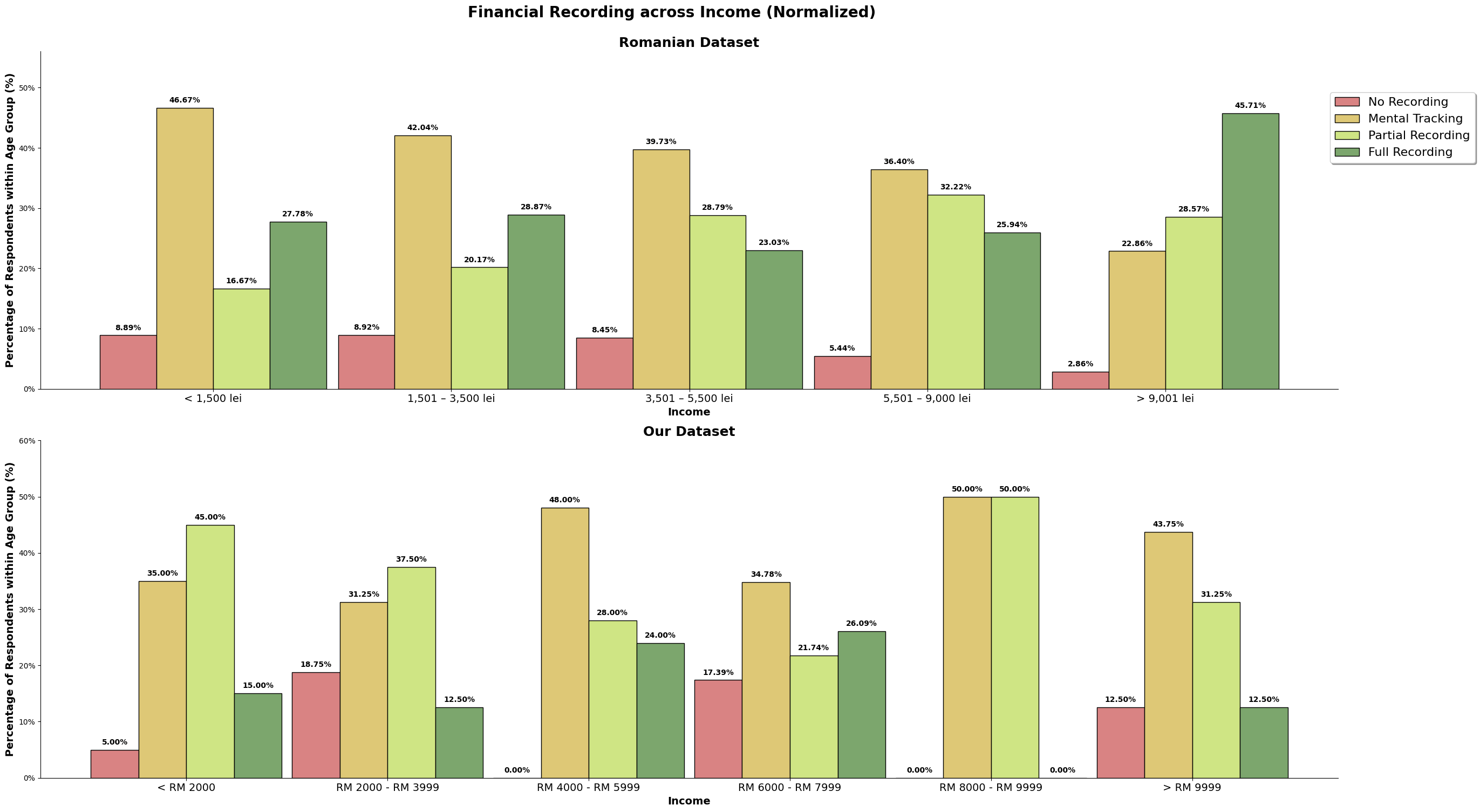

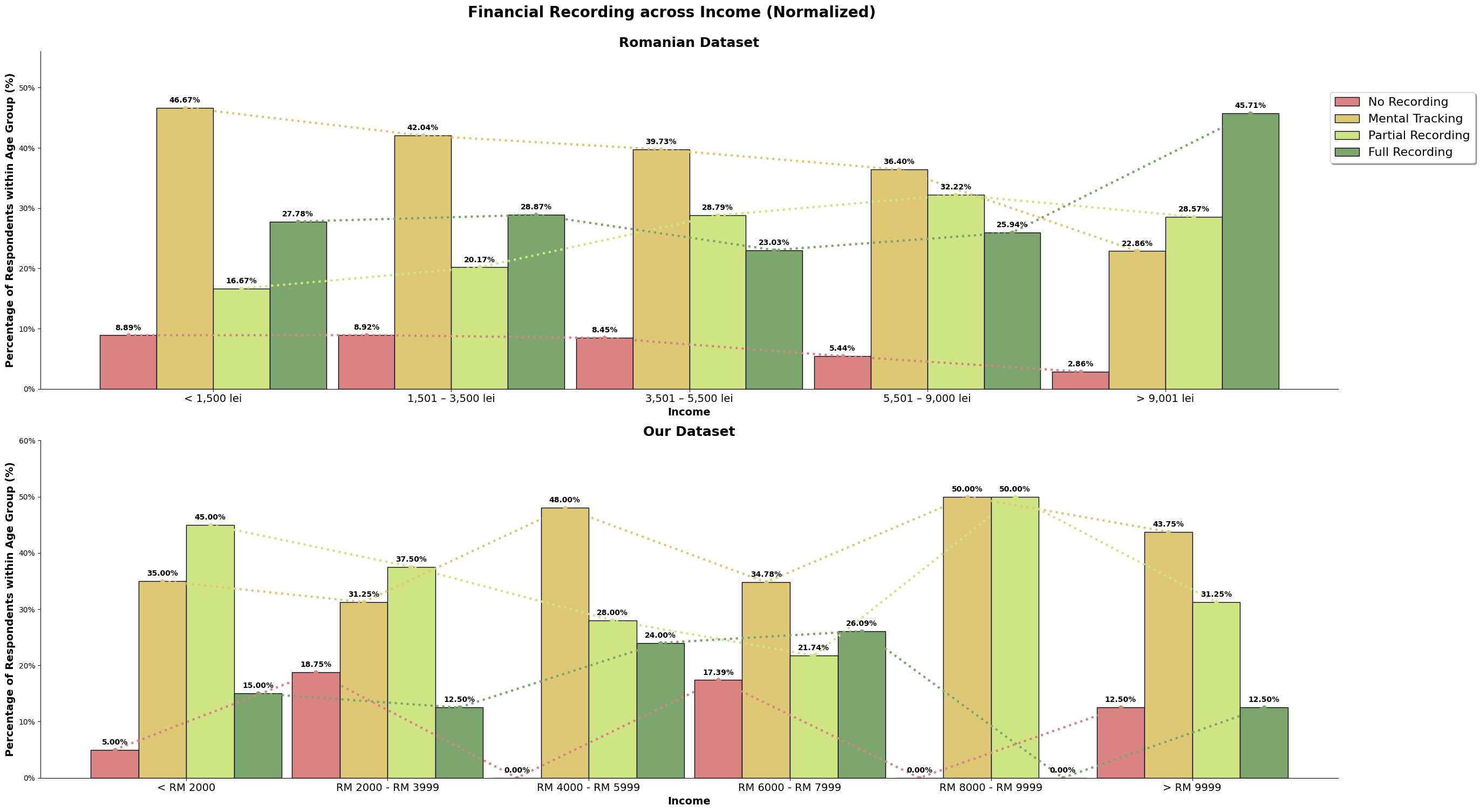

In the Romanian study, we saw that as people earn more and get older, they tend to keep better records of their money. But for our dataset, we found something different. We observed that those with high financial literacy actually do less strict recording and prefer 'Mental Tracking'. This suggests that they might feel confident enough to just estimate their finances mentally instead of keeping detailed records.

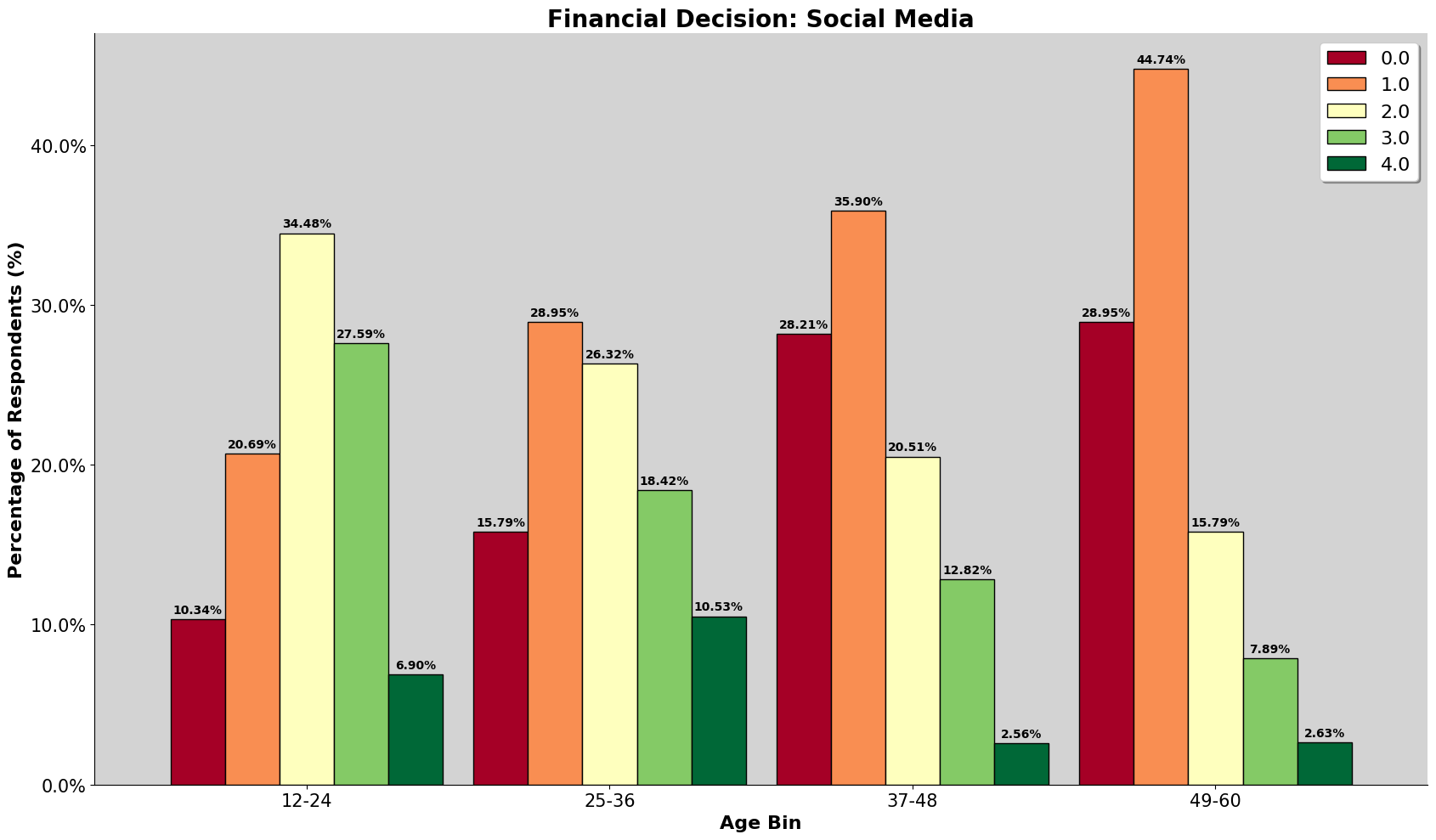

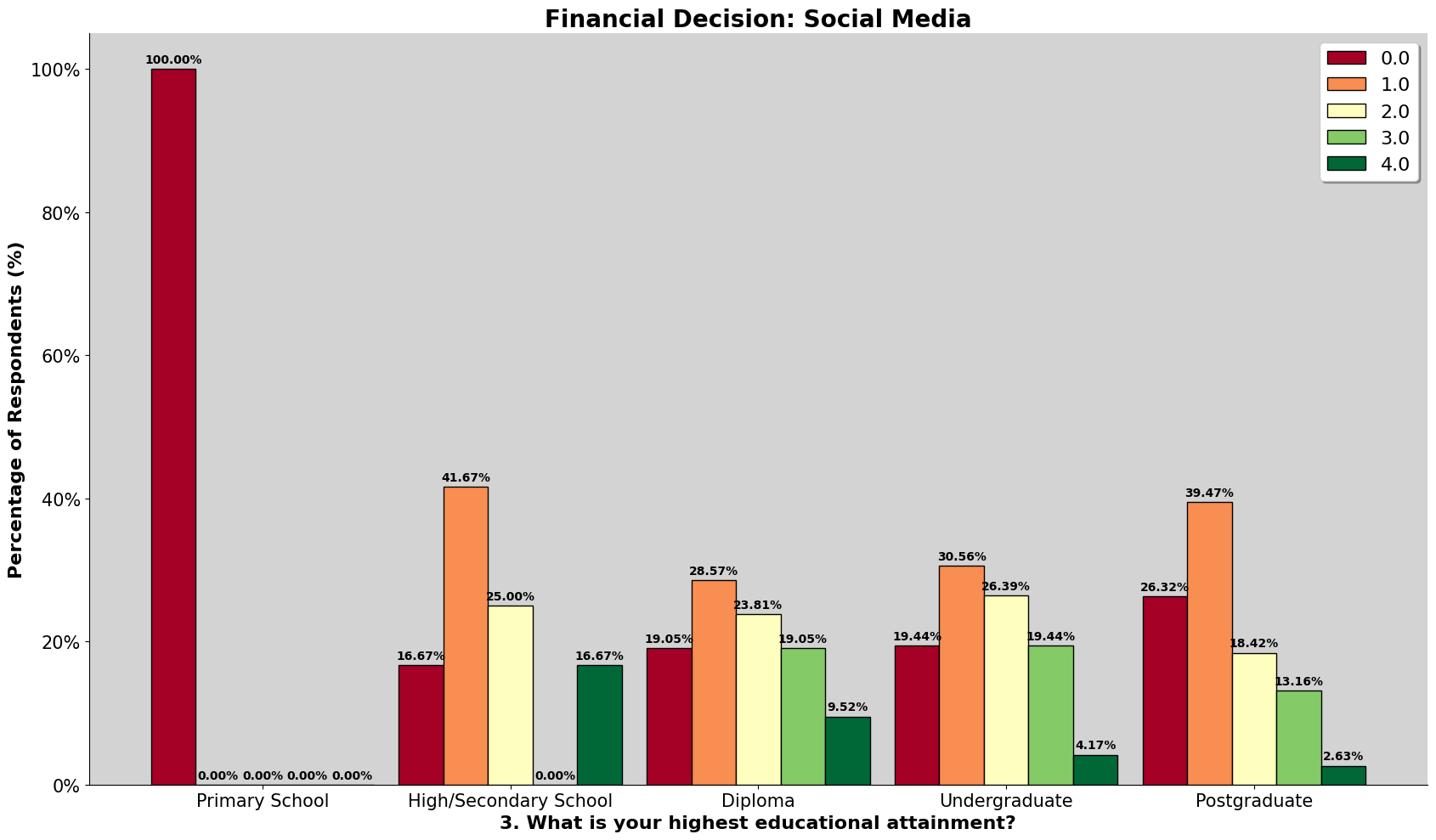

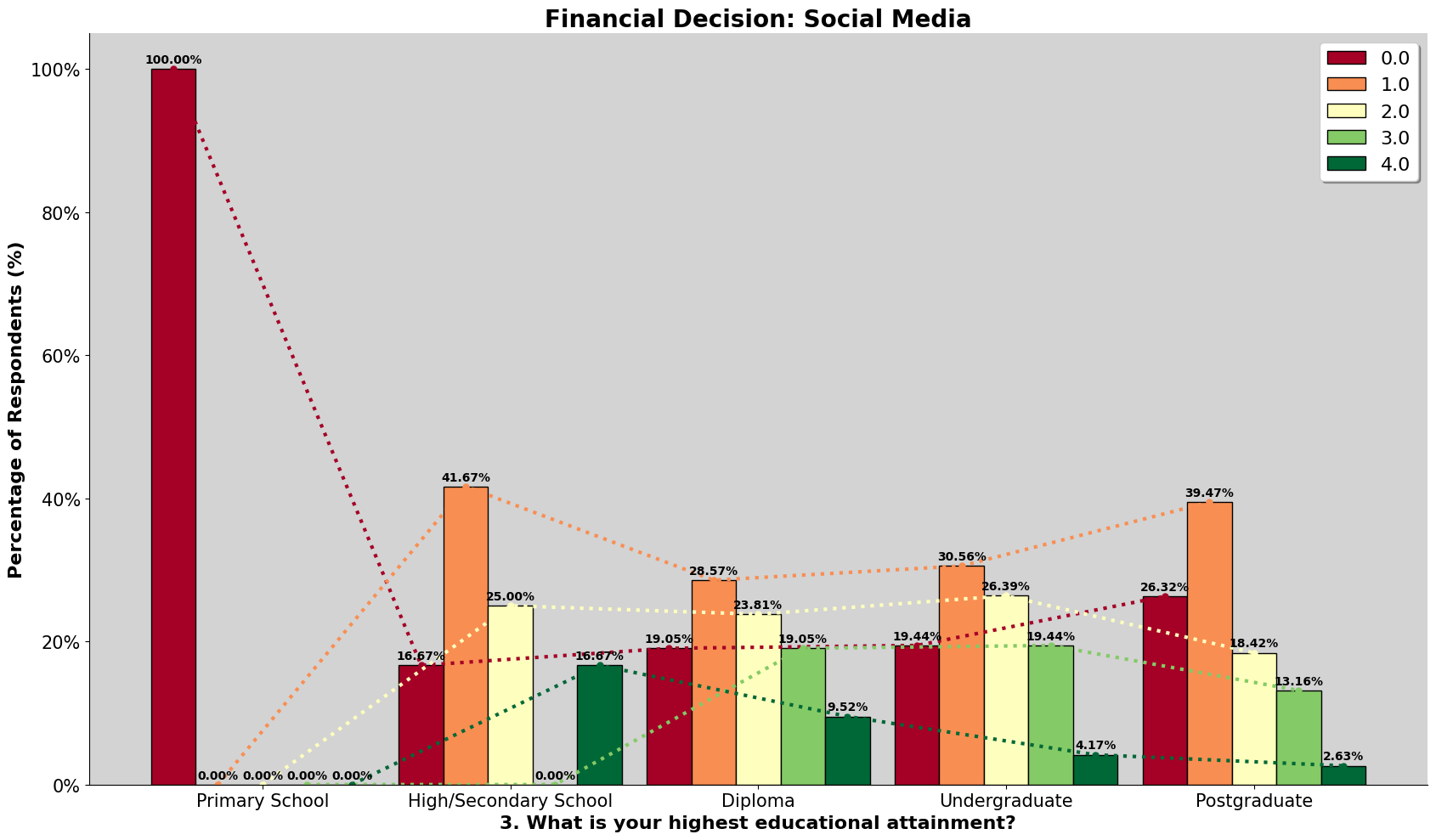

Who do we listen to for advice?

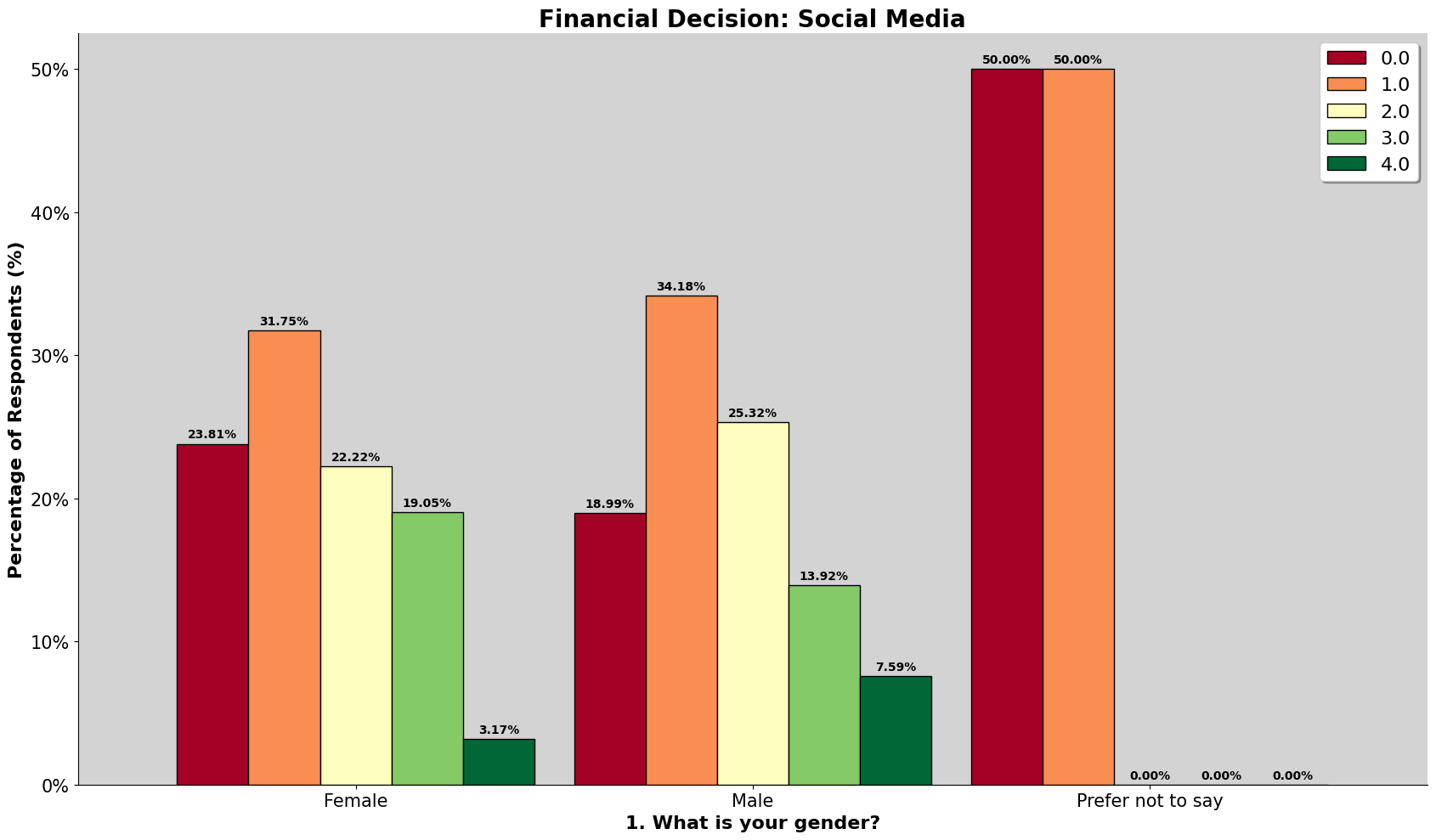

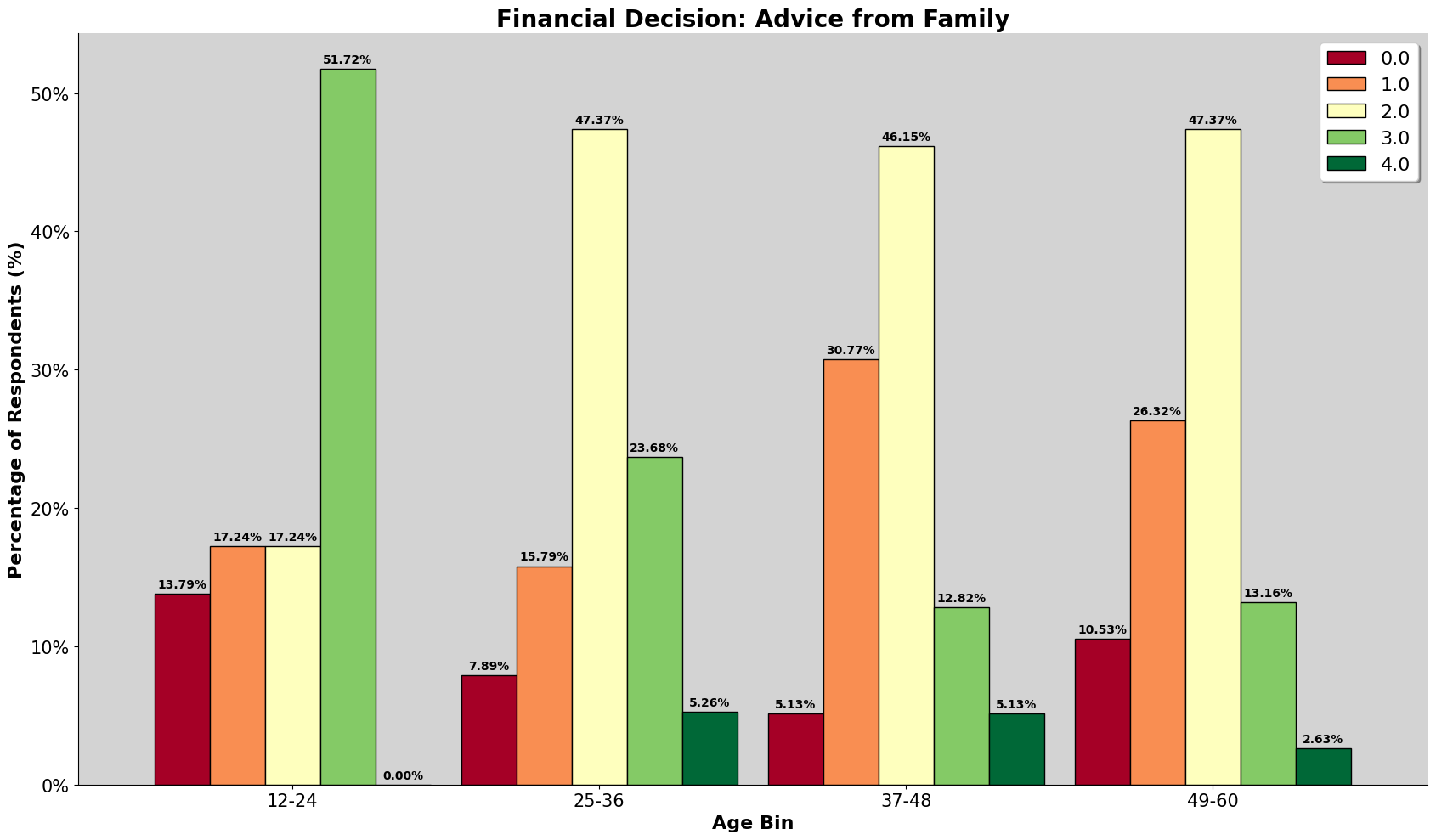

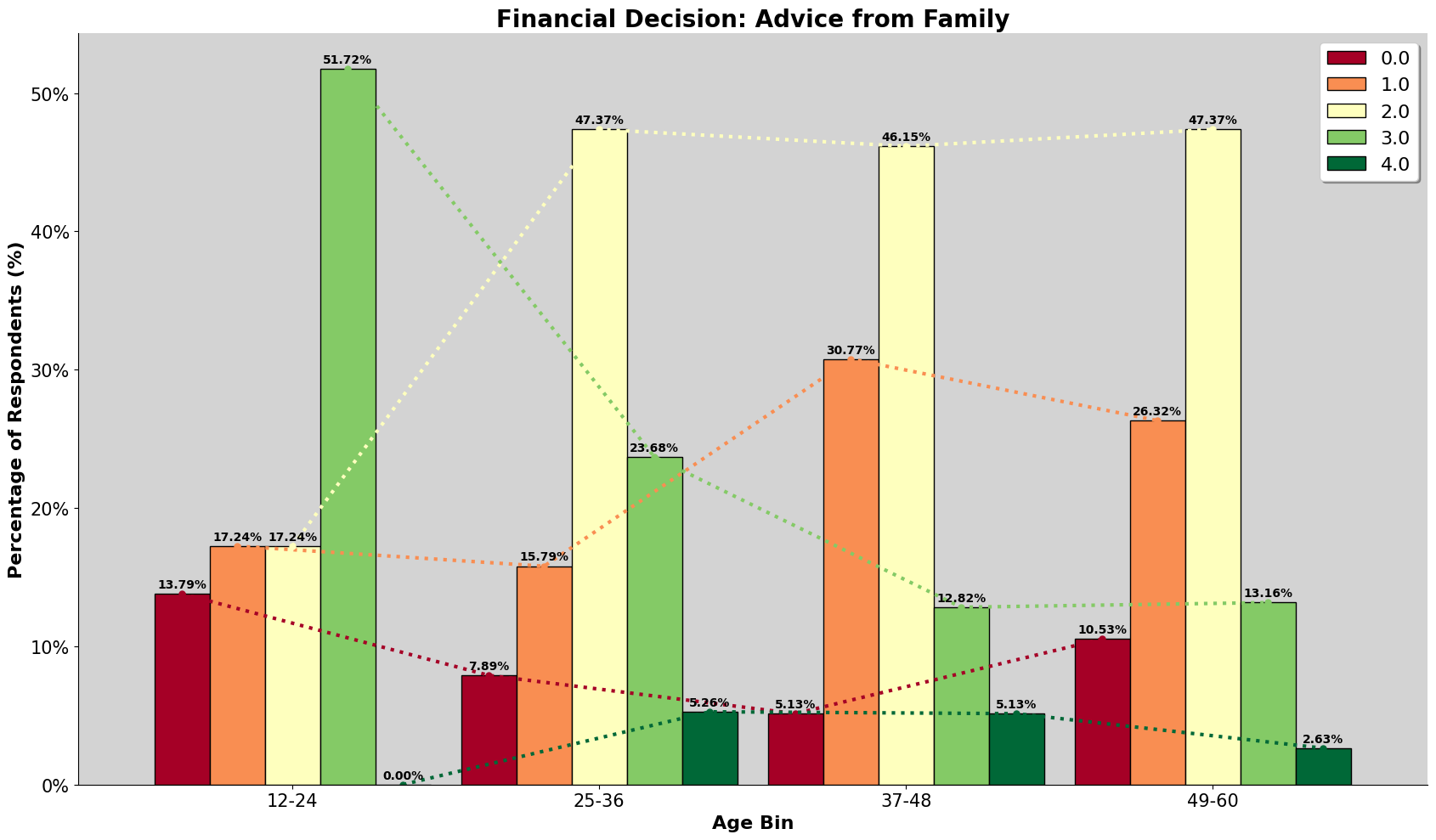

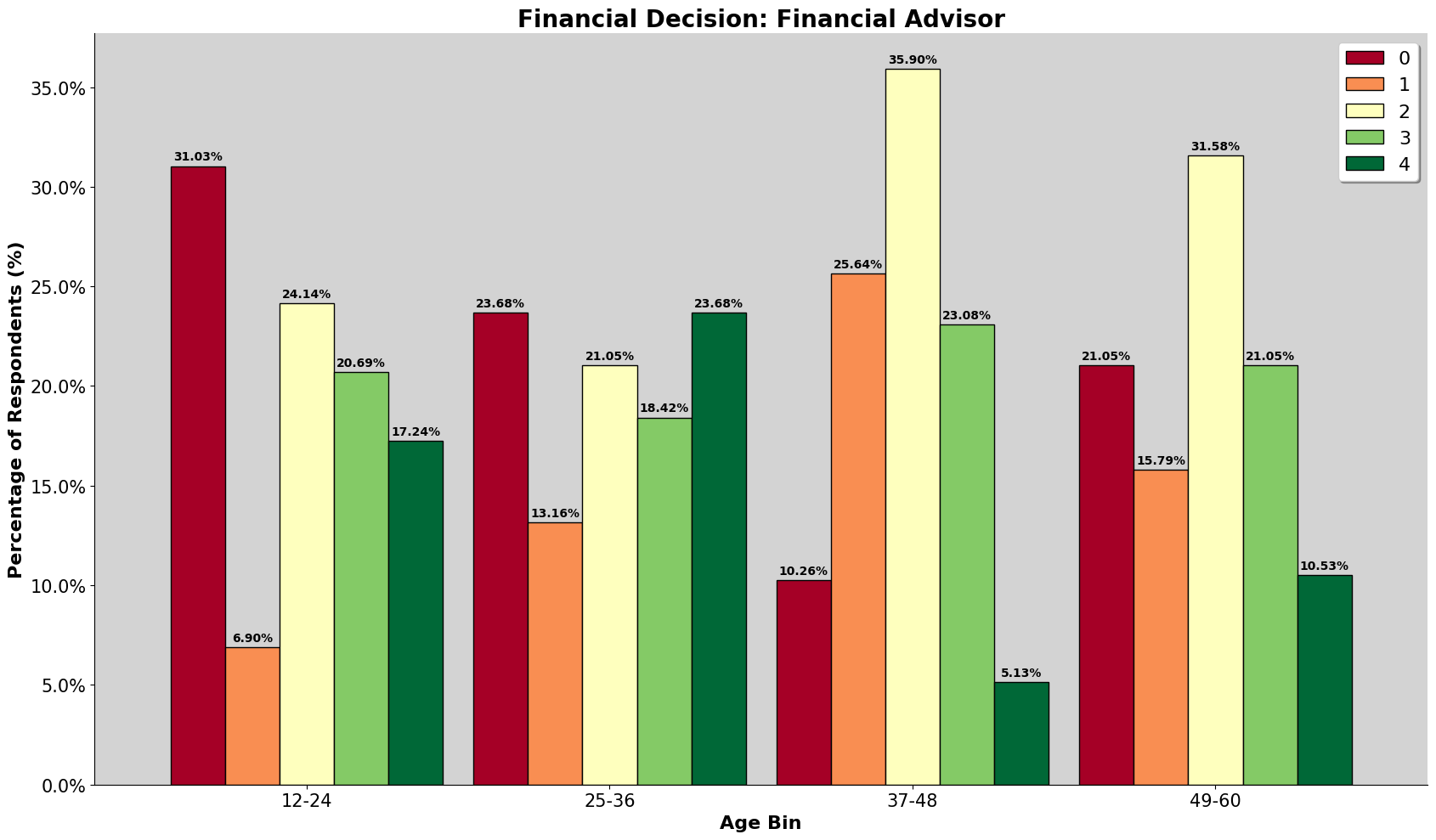

We found that the participants in our dataset, who are mostly urban Malaysians, rely a lot more on "Social Media" and "Advice From Family" for financial advice. This is different from the Romanian dataset, where they favor "Mass Media" (TV and Radio) and "Personal Experience". We also noted that the individuals with high financial well-being in our group relied less on professional financial advisors. This challenges the idea that once you have more money, you would hire a professional to manage it.

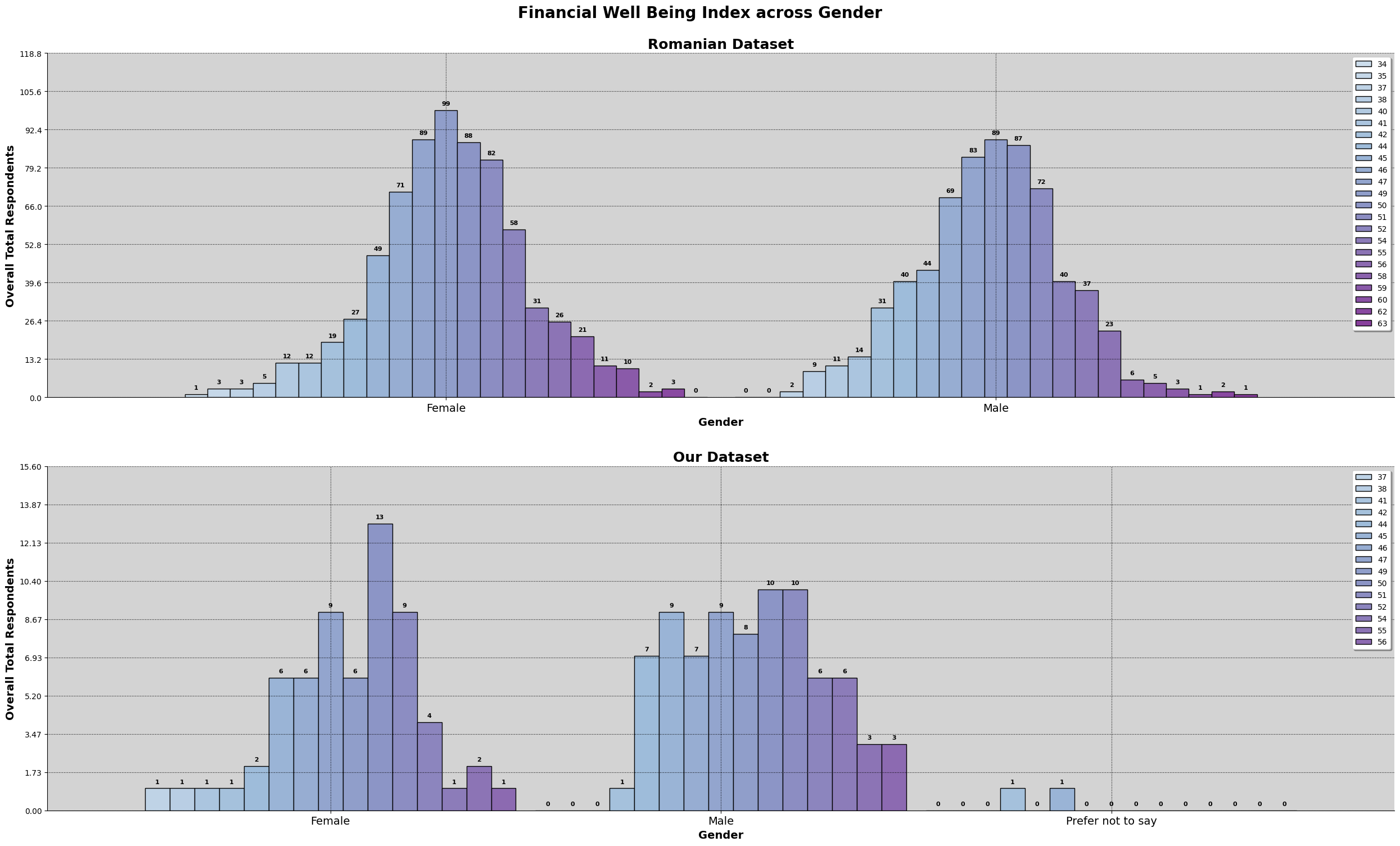

Does Gender affect Financial Outcomes?

For the Romanian dataset, we saw that financial well-being was quite equal between genders. However, in our dataset, we observed a difference. The group with "High Financial Well-Being" (those scoring 1 standard deviation above the mean) was mostly Male (about 75%), even though females had similar financial literacy scores in the middle ranges. This suggests there might be other factors affecting well-being outside of just financial knowledge.

Conclusion

So, to answer our initial research questions:

-

What are sociodemographic conditions that affect the financial literacy and financial well-being of an individual?

We found that education and income are generally good predictors for financial literacy, similar to what the Romanian study found. However, for financial well-being in our Malaysian context, being Male and having a higher income seemed to be the strongest traits for the "high well-being" group. Surprisingly, we also found that high income and education sometimes led to less strict financial recording, with people relying more on mental tracking.

-

Does possessing financial literacy lead to financial well-being?

In our study, the answer is: not necessarily. While participants in our dataset had higher financial literacy scores on average than the participants in the romanian dataset, this didn't translate to higher financial well-being scores. In fact, we found a weak negative link between the two. This suggests that just knowing about money isn't enough to guarantee feeling financially secure, especially for the younger urban demographic we surveyed.

Limitation of Research

Causaction and Correlation

The findings in this project are mainly correlation and relationship between factors and/or characteristics of the dataset and survey participants. We cannot fully conclude a direct causation in the findings. For example, it might be because of having higher financial literacy that causes one to have higher income due to having financial knowledge on how to manage money, But it also can be argued that because one has achieved a higher income, they will have increased financial literacy as it is needed to extend and further understand the management of money.

Sample Limitations

For our dataset, we were only able to achieve 144 survey responses and they are mainly based in Kuala Lumpur, one of the city area of Malaysia, and majority of them are young adults. Hence, it will not be a good representation of whole country of Malaysia. Additionally, because we employed word of mouth and snowball sampling method, we were able to extend the target audience to those that are above 35. However, they were not sufficient to build a good representation of these age group, which affects the findings later on, where trend and patterns might not be identifiable.

Data Pre-processing and Exploratory Analysis

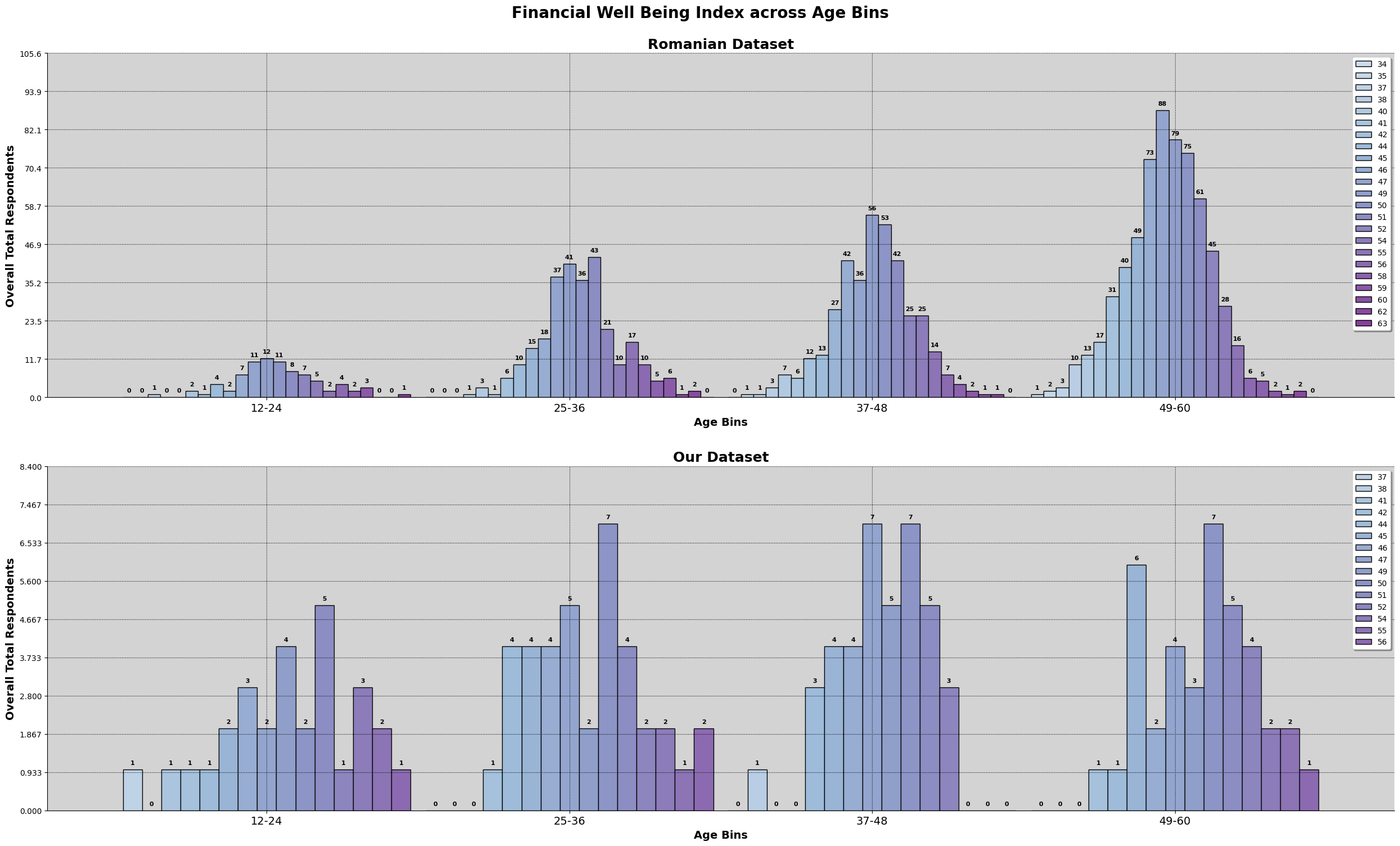

Age Distribution

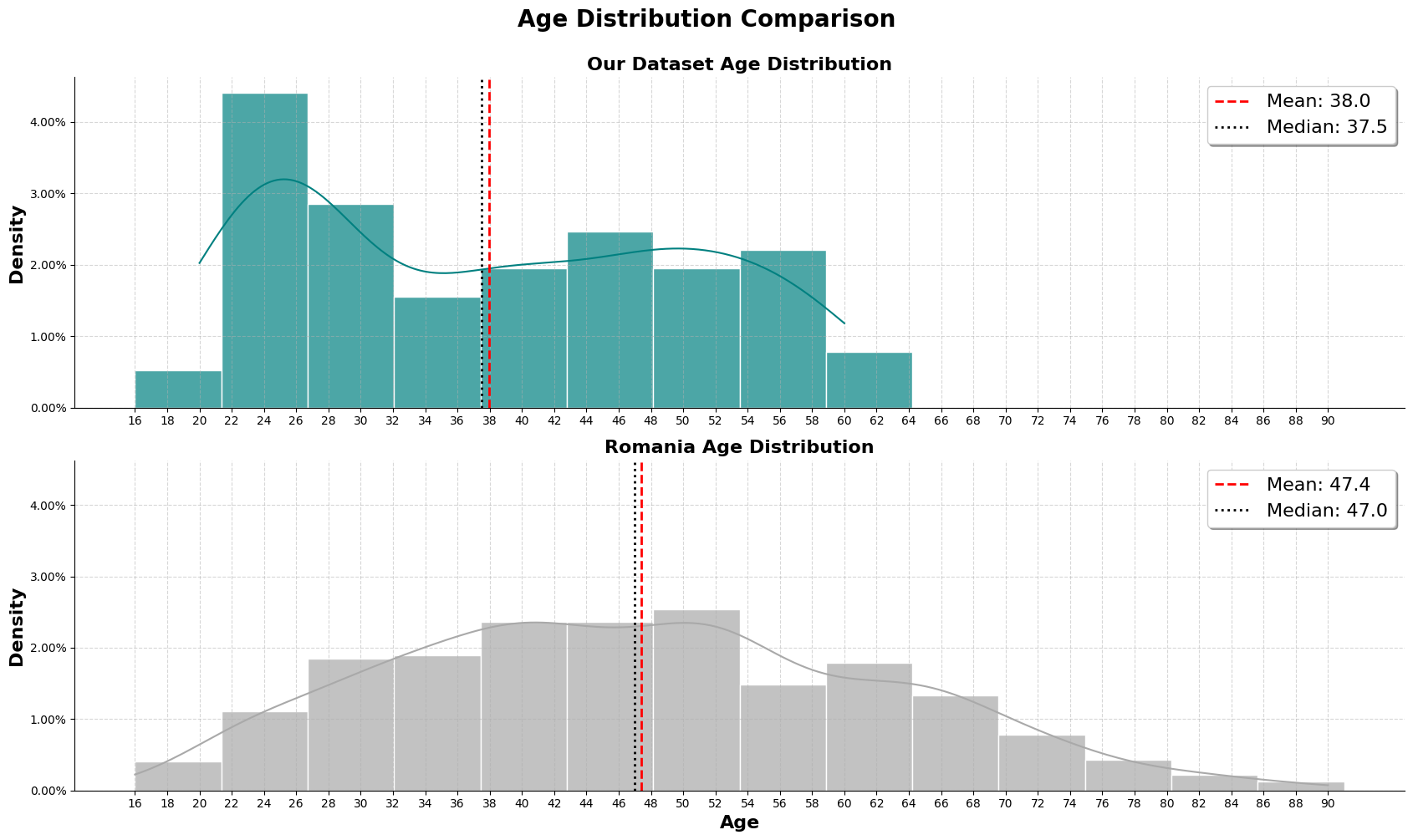

Because the survey was designed to collect discrete individual ages, rather than in range of age like (18 - 30, 31 - 40, etc), so that we can fine tune the data afterwards. We initially aim to collect data from survey participants aged between 18 to somewhere late 30s. Hence, during the survey design process, we decided to cap the age at 60, and allowed those above 60 to select the option ">60", if there were any. To ensure we had no input error/mistakes by the participates, we used drop down list from 18 to 60, and ">60".

Actual Distribution

As shown in the graph, our dataset has a limitation where an individual might be older than 60, but it cannot be accurately shown in the graph. Our dataset heavily skewed towards 18 - 35, even with the limitation mentioned.

For the romanian dataset, we can observe that there is a good general spread of population throught the age range, peaking around the ages 40 - 60.

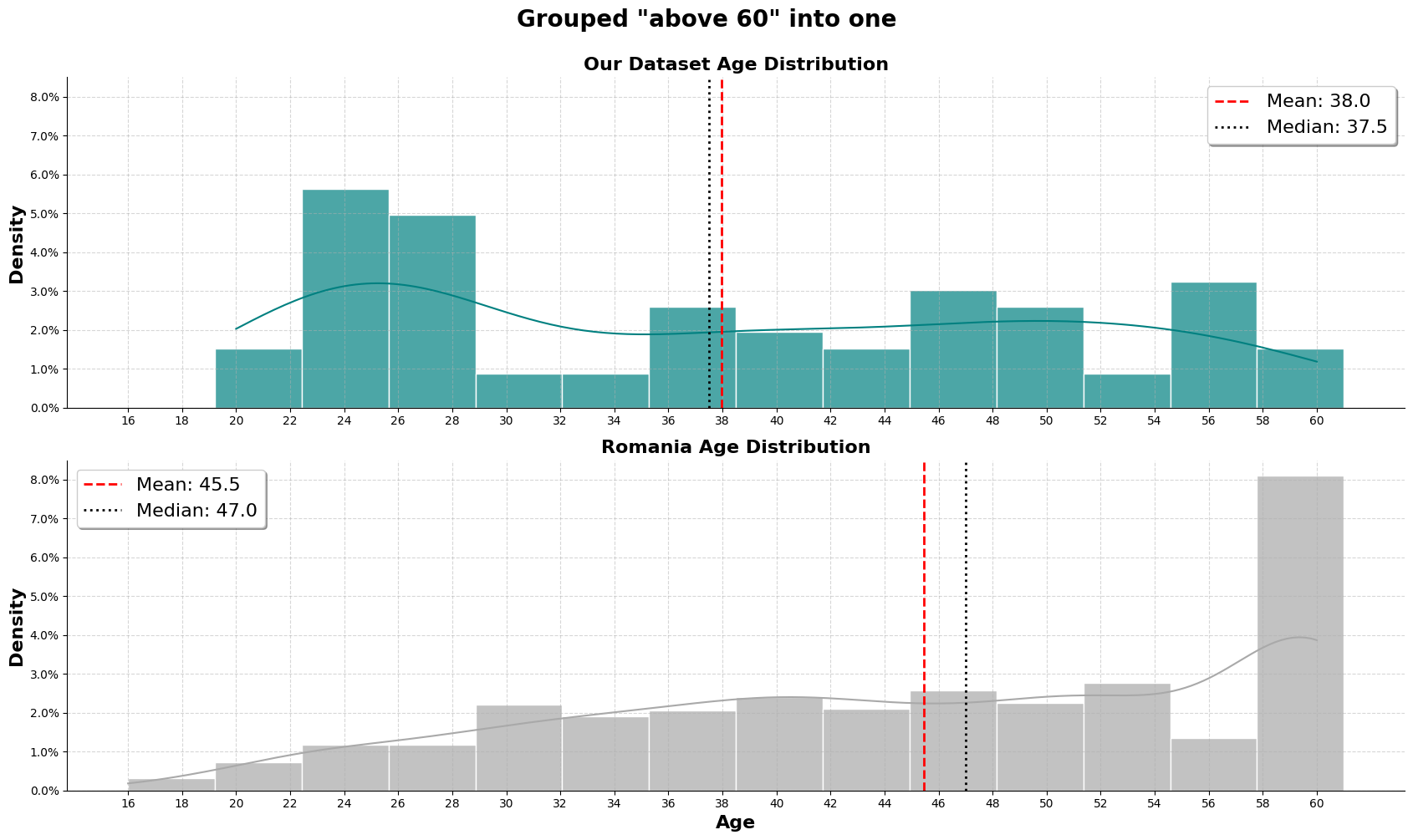

Treating 'above 60' as a group

To apply the same standards between both dataset, we will treat those that are above 60, as one group. As shown in the graph, the romanian dataset will then have a heavy skew to the right, with over 8% of the population in the '>60' category.

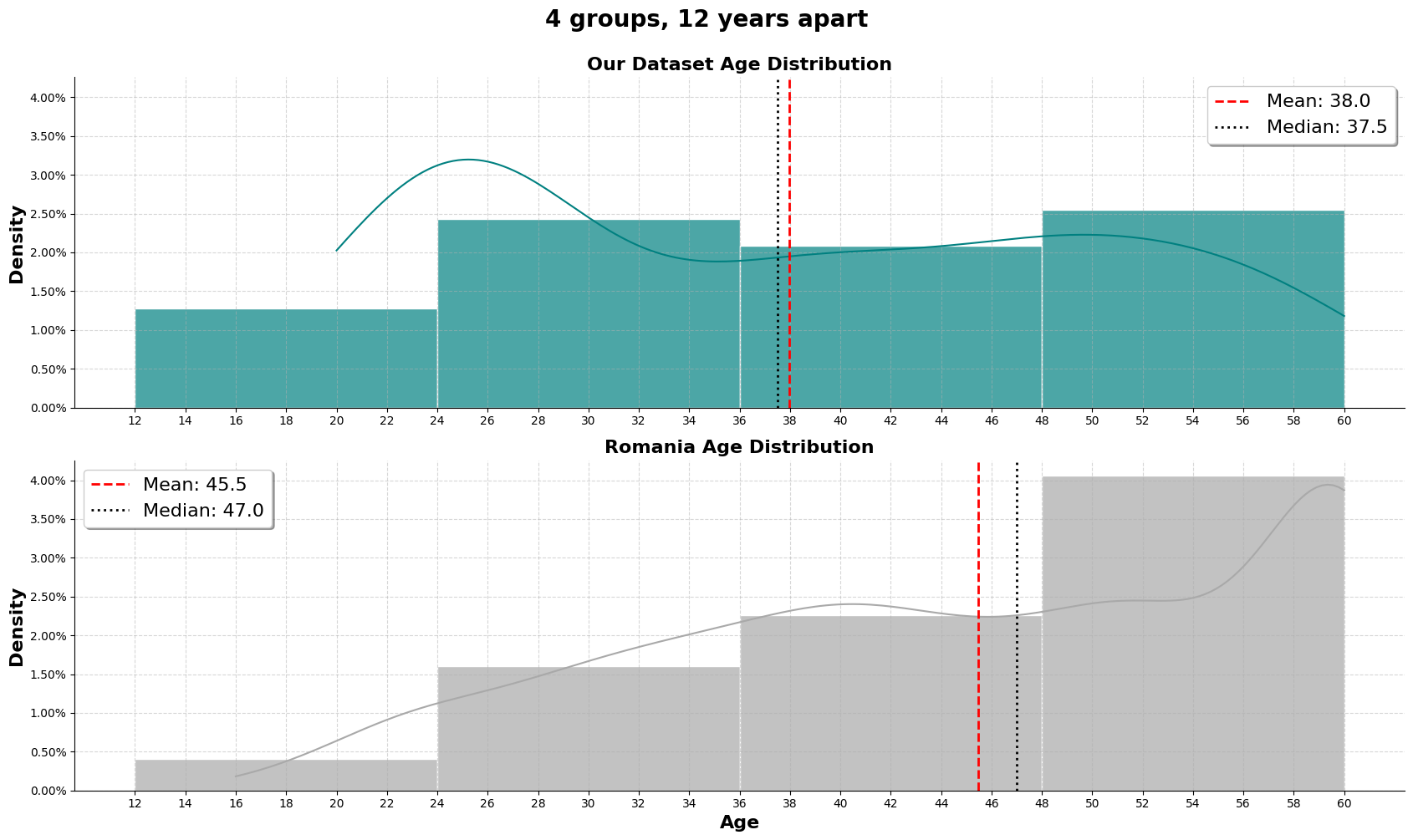

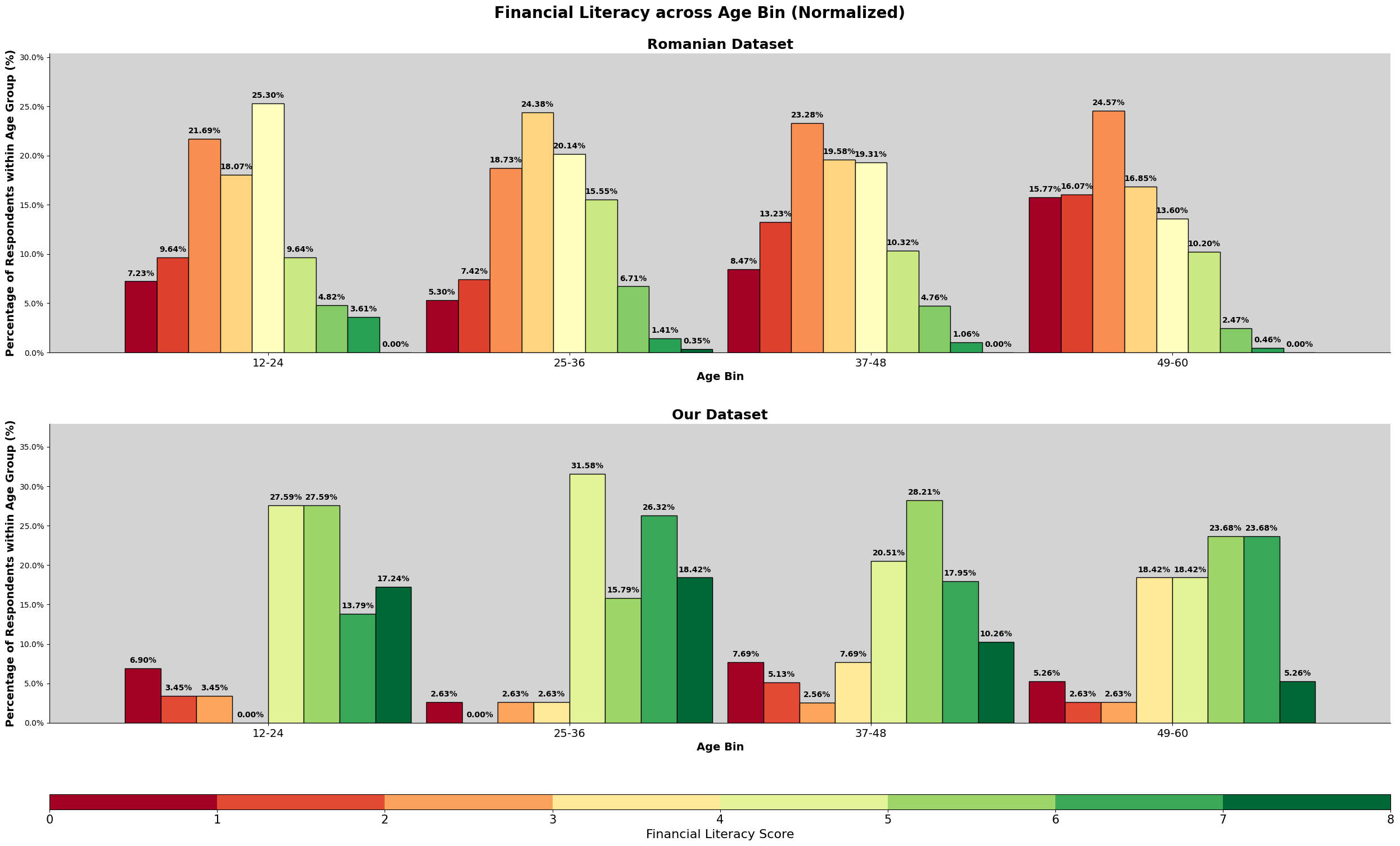

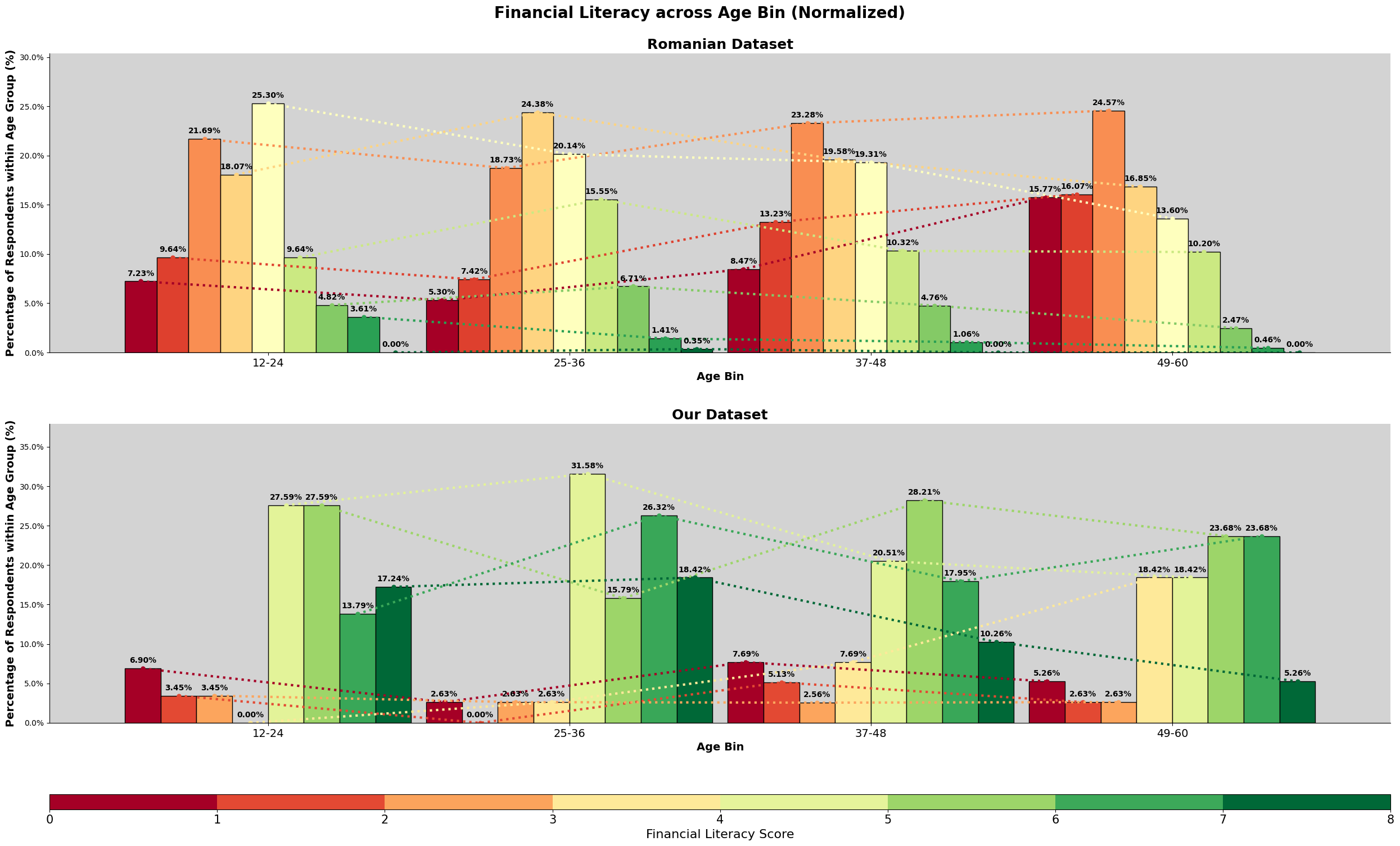

Split into groups of 4, 12 years apart

Then, proceeded to group them into 4 groups, 12 years apart. For our dataaset, the group seem to relatively equal for the last 3 groups, while for the romanian dataset, the split has made each ascending group to have more population. We are aware that the age bin of 12 - 24, even though there is no data indicating age of 16 and below, we decided to stick with it because during trial and error, the starting age of 12 and then continuously jumping 12 years for each group seem fitting.

def create_age_distribution_chart(our_dataset, romania_dataset, min_age, max_age, bin, suptitle):

# Initialize figure

fig, (ax1, ax2) = plt.subplots(2, 1, figsize=(17, 10), facecolor='white', sharey=True)

# Setting values for loop

datasets = [

('Our Dataset', our_dataset, 'teal', ax1),

('Romania', romania_dataset, 'darkgray', ax2)

]

# Loop through the values set

for country, df, color, ax in datasets:

# Get age column

age_col = 'SD3' if country == 'Romania' else [c for c in df.columns if 'age' in c.lower()][0]

data = df[age_col]

# Plot Histogram + KDE

sns.histplot(data, bins=bin, kde=True, color=color, alpha=0.7, ax=ax, stat="density",

edgecolor='white', linewidth=1)

# Set mean and median

mean_val = data.mean()

median_val = data.median()

ax.axvline(mean_val, color='red', linestyle='--', linewidth=2, label=f'Mean: {mean_val:.1f}')

ax.axvline(median_val, color='black', linestyle=':', linewidth=2, label=f'Median: {median_val:.1f}')

# Styling

ax.set_title(f'{country} Age Distribution', fontsize=16, fontweight='bold')

if ax == ax2:

ax.set_xlabel('Age', fontsize=16, fontweight='bold')

else:

ax.set_xlabel('')

ax.set_ylabel('Density', fontsize=16, fontweight='bold')

ax.set_xticks(range(min_age,max_age,2))

ax.legend(frameon=True, fontsize=16, shadow=True)

ax.grid(axis='x', alpha=0.5, linestyle='--')

ax.grid(axis='y', alpha=0.5, linestyle='--')

ax.spines['top'].set_visible(False)

ax.spines['right'].set_visible(False)

fig.suptitle(suptitle,

fontsize=20, fontweight='bold', y=1)

formatter = mtick.PercentFormatter(xmax=1.0)

ax.yaxis.set_major_formatter(formatter)

plt.tight_layout()

plt.show()

# Generate Plots

# ================

# Age Distribution Comparison

create_age_distribution_chart(our_dataset, romanian_dataset, 16, 91, np.linspace(16,91,15),

'Age Distribution Comparison')

# Replacing anything above 60, into 60

romanian_dataset['SD3'] = romanian_dataset['SD3'].where(

romanian_dataset['SD3'] <= 60, 60

)

# Grouping 'above 60' as 60

create_age_distribution_chart(our_dataset, romanian_dataset, 16, 61, np.linspace(16,61,15),

'Grouped "above 60" into one')

# Splitting into groups of 4, 12 years apart

create_age_distribution_chart(our_dataset, romanian_dataset, 12, 61, np.histogram_bin_edges([12,24,36,48,60],4),

'4 groups, 12 years apart')

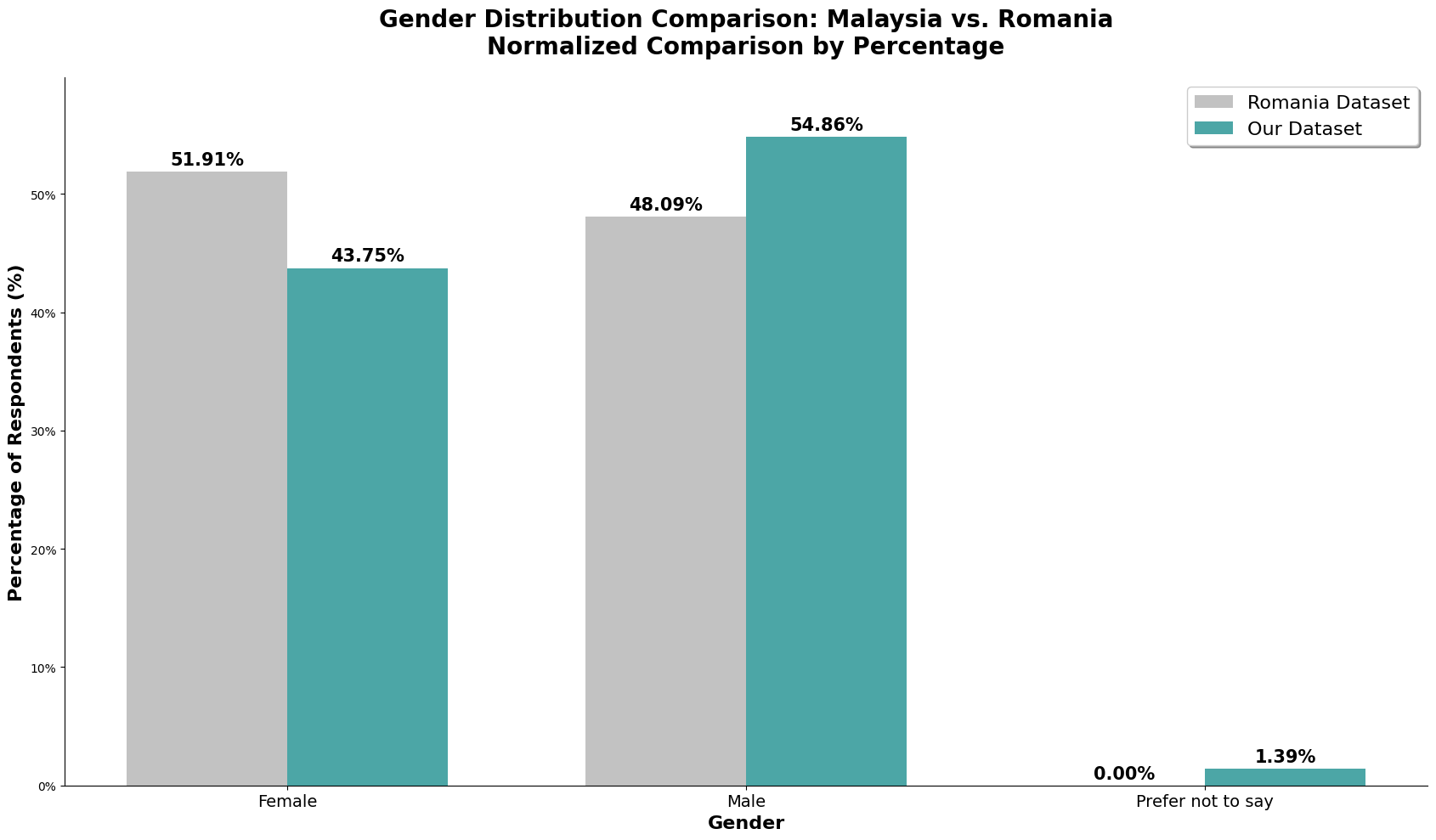

Gender Distribution

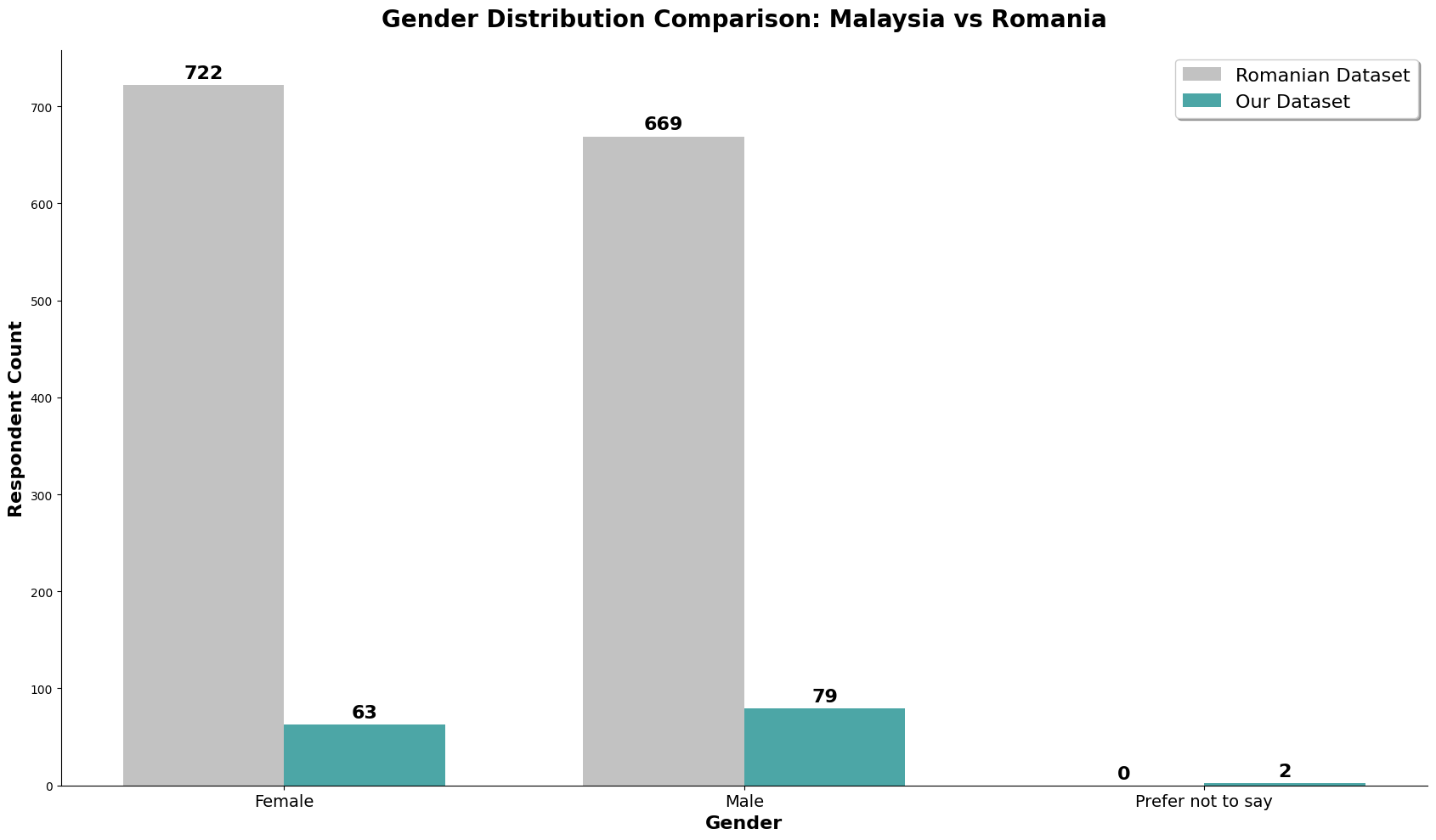

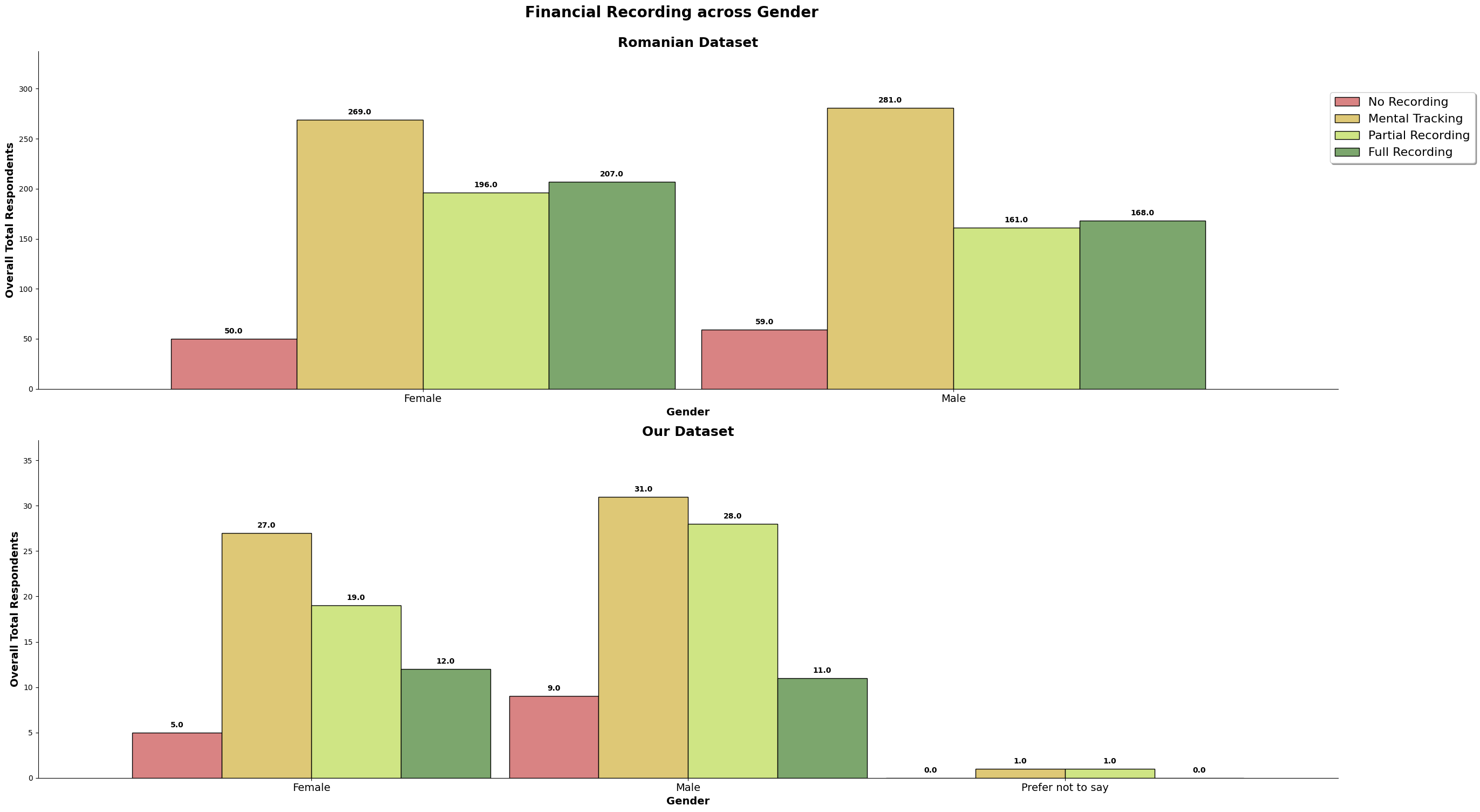

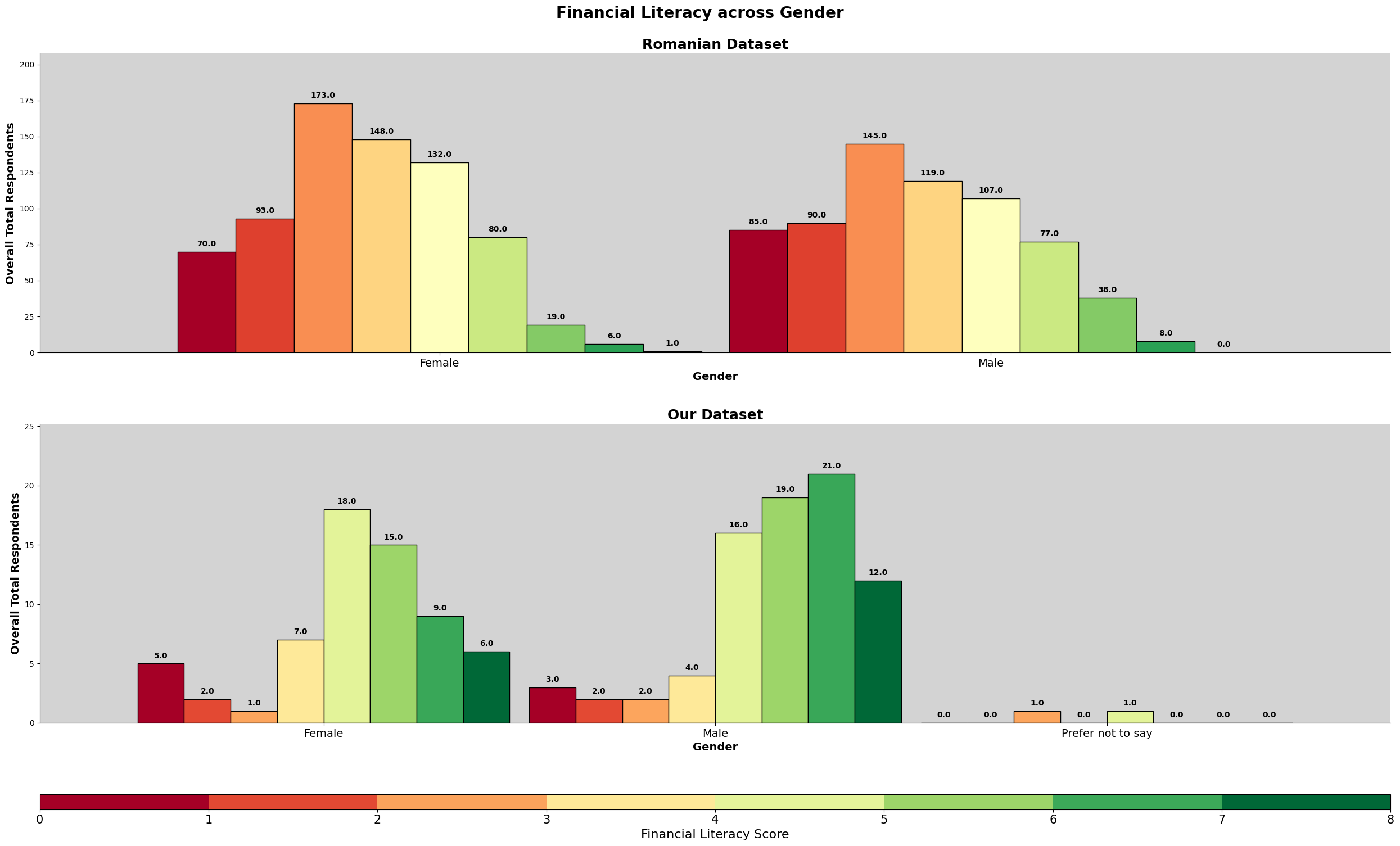

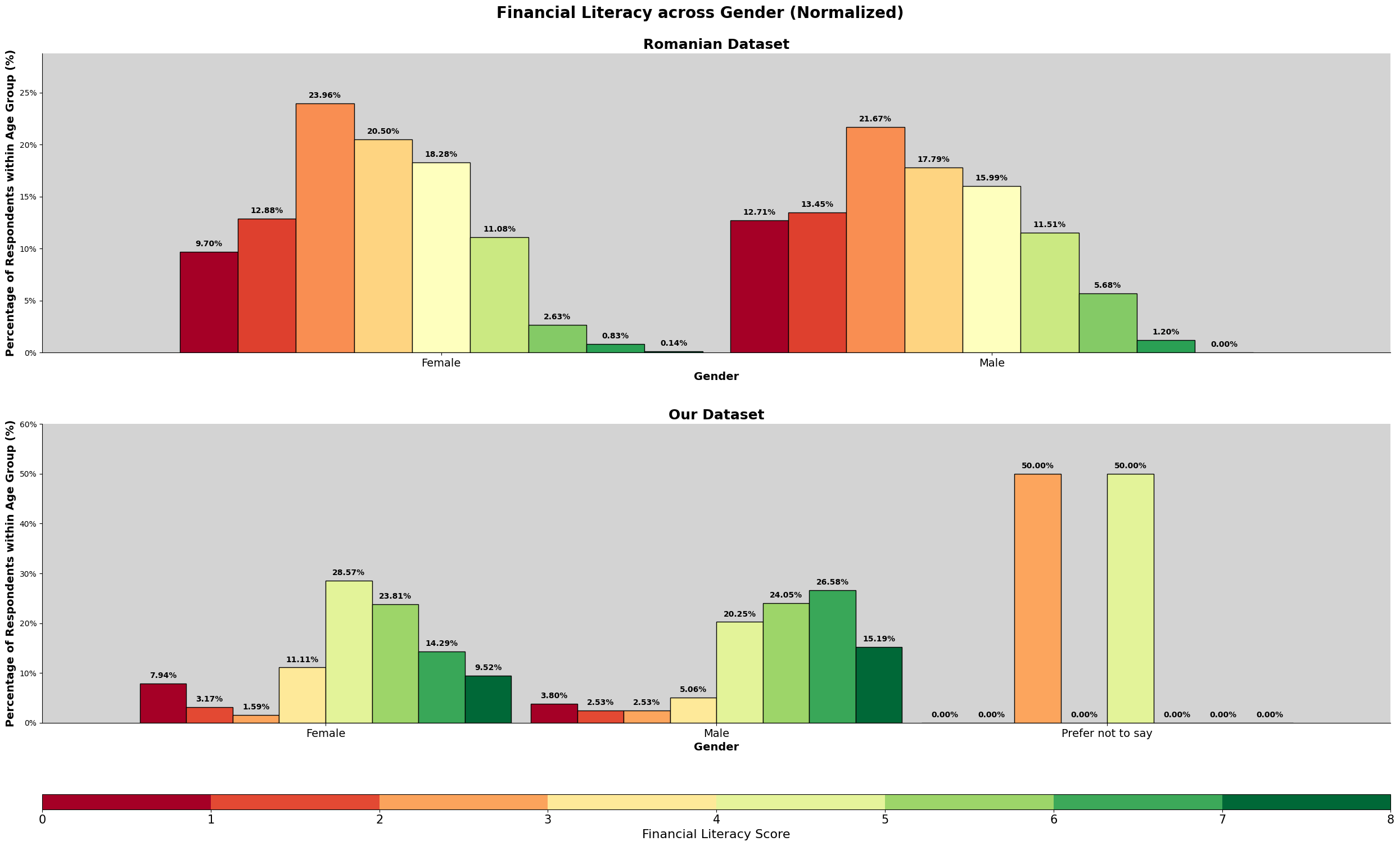

The chart above is the gender count for both datasets.

The chart above is the gender count normalized. We can observe that the romanian dataset has almost a perfect 50/50, almost 4% more females. On the other hand, our dataset has about 11% more males, in which we should take note in our analysis later.

# Data Preparation

# ================

# Set labels

genders = ["Female", "Male", "Prefer not to say"]

# Get the count of the unique values of both datasets

romanian_dataset_gender_count = getCount(romanian_dataset['SD2'])

our_dataset_gender_count = getCount(our_dataset[getOurString('gender', our_columns)])

# Adding 'Prefer not to say' to Romania

romanian_dataset_gender_count["Prefer not to say"] = 0

# Sorting them

romanian_dataset_gender_count = dict(sorted(romanian_dataset_gender_count.items()))

our_dataset_gender_count = dict(sorted(our_dataset_gender_count.items()))

# Store and sort gender ratio

our_dataset_gender_ratio = our_dataset_gender_count.copy()

for key in our_dataset_gender_ratio:

our_dataset_gender_ratio[key] /= our_total_respondent

our_dataset_gender_ratio = dict(sorted(our_dataset_gender_ratio.items()))

romanian_dataset_gender_ratio = romanian_dataset_gender_count.copy()

for key in romanian_dataset_gender_ratio:

romanian_dataset_gender_ratio[key] /= romanian_total_respondent

romanian_dataset_gender_ratio = dict(sorted(romanian_dataset_gender_ratio.items()))

gender_ratio_datasets = [romanian_dataset_gender_ratio, our_dataset_gender_ratio]

# Count Chart

# ==============

# Initialize the plots using Object-Oriented API

fig, ax = plt.subplots(figsize=(17, 10))

# Set x values and

x = np.arange(3)

width = 0.35

# Plot both datasets on same axes with appropriate offsets

bar1 = ax.bar(x - width / 2, romanian_dataset_gender_count.values(), width,

label='Romanian Dataset', color='darkgray', alpha=0.7)

ax.bar_label(bar1, padding=3, fontsize=16, fontweight="bold")

bar2 = ax.bar(x + width / 2, our_dataset_gender_count.values(), width,

label='Our Dataset', color='teal', alpha=0.7)

ax.bar_label(bar2, padding=3, fontsize=16, fontweight="bold")

# Styling

ax.set_title('Gender Distribution Comparison: Malaysia vs Romania',

fontsize=20, fontweight='bold', pad=20)

ax.set_xlabel('Gender', fontsize=16, fontweight="bold")

ax.set_ylabel('Respondent Count', fontsize=16, fontweight="bold")

ax.legend(frameon=True, shadow=True, fontsize=16)

ax.set_xticks(x)

ax.set_xticklabels(genders, fontsize=14)

ax.spines['top'].set_visible(False)

ax.spines['right'].set_visible(False)

plt.tight_layout()

plt.show()

# Percentage Chart

# ================

# Create Plot

fig, ax = plt.subplots(figsize=(17,10))

# Set x values and width

x = np.arange(3)

width = 0.35

# Plot both datasets on same axes with appropriate offsets

bar1 = ax.bar(x - width/2, gender_ratio_datasets[0].values(), width, label="Romania Dataset", color="darkgray", alpha=0.7)

bar2 = ax.bar(x + width/2, gender_ratio_datasets[1].values(), width, label="Our Dataset", color="teal", alpha=0.7)

for bar in [bar1, bar2]:

ax.bar_label(bar, fmt='{:.2%}', fontsize=15, fontweight='bold', padding=3)

# Styling

ax.set_ylabel('Percentage of Respondents (%)', fontsize=16, fontweight='bold')

ax.set_xlabel('Gender', fontsize=16, fontweight='bold')

ax.set_title('Gender Distribution Comparison: Malaysia vs. Romania\nNormalized Comparison by Percentage',

fontsize=20, fontweight='bold', pad=20)

ax.set_xticks(x)

ax.set_xticklabels(genders, fontsize=14)

ax.set_ylim(0, max(max(gender_ratio_datasets[0].values()), max(gender_ratio_datasets[1].values())) + 0.05)

ax.legend(shadow=True, frameon=True, fontsize=16)

ax.spines['right'].set_visible(False)

ax.spines['top'].set_visible(False)

formatter = mtick.PercentFormatter(xmax=1.0)

ax.yaxis.set_major_formatter(formatter)

plt.tight_layout()

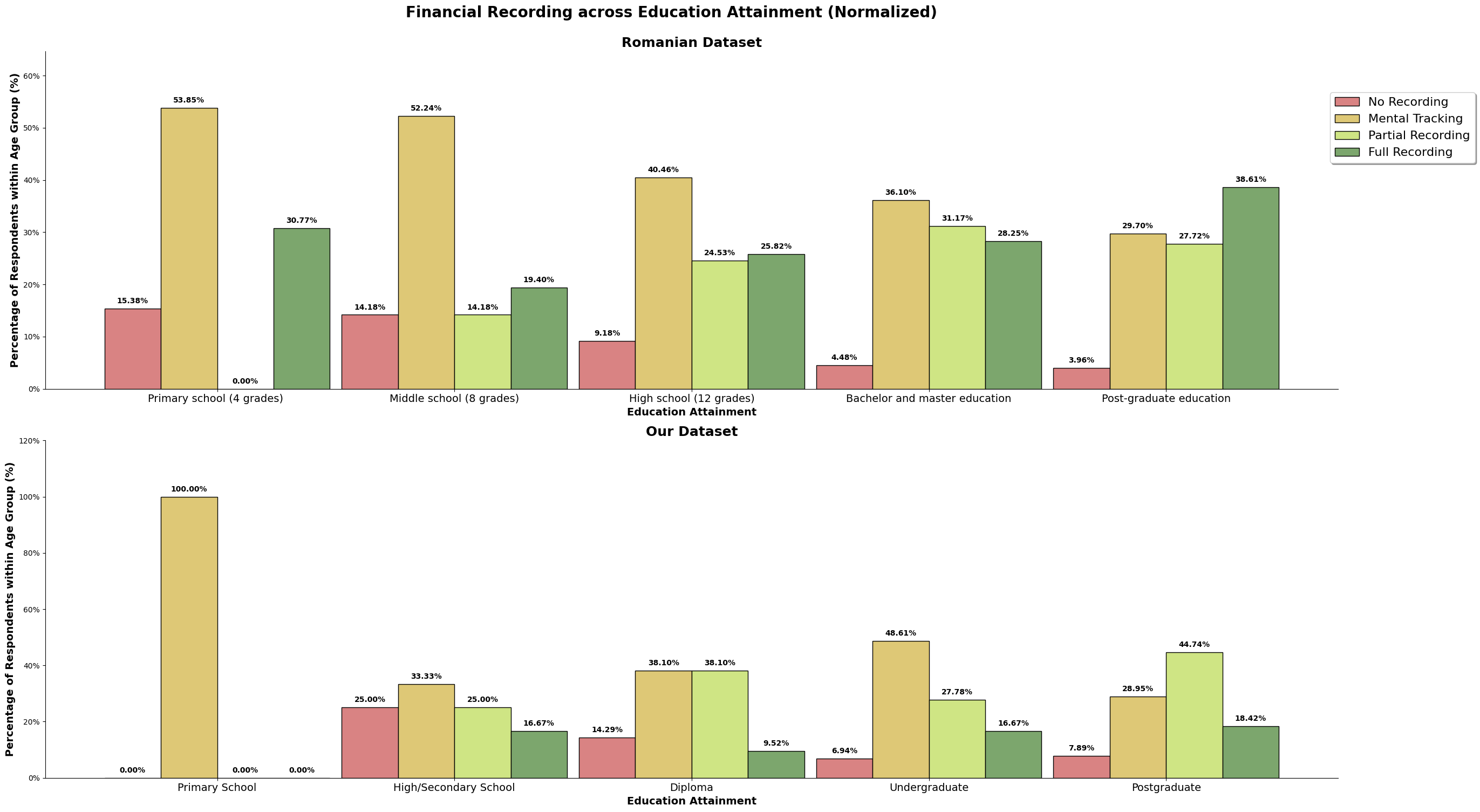

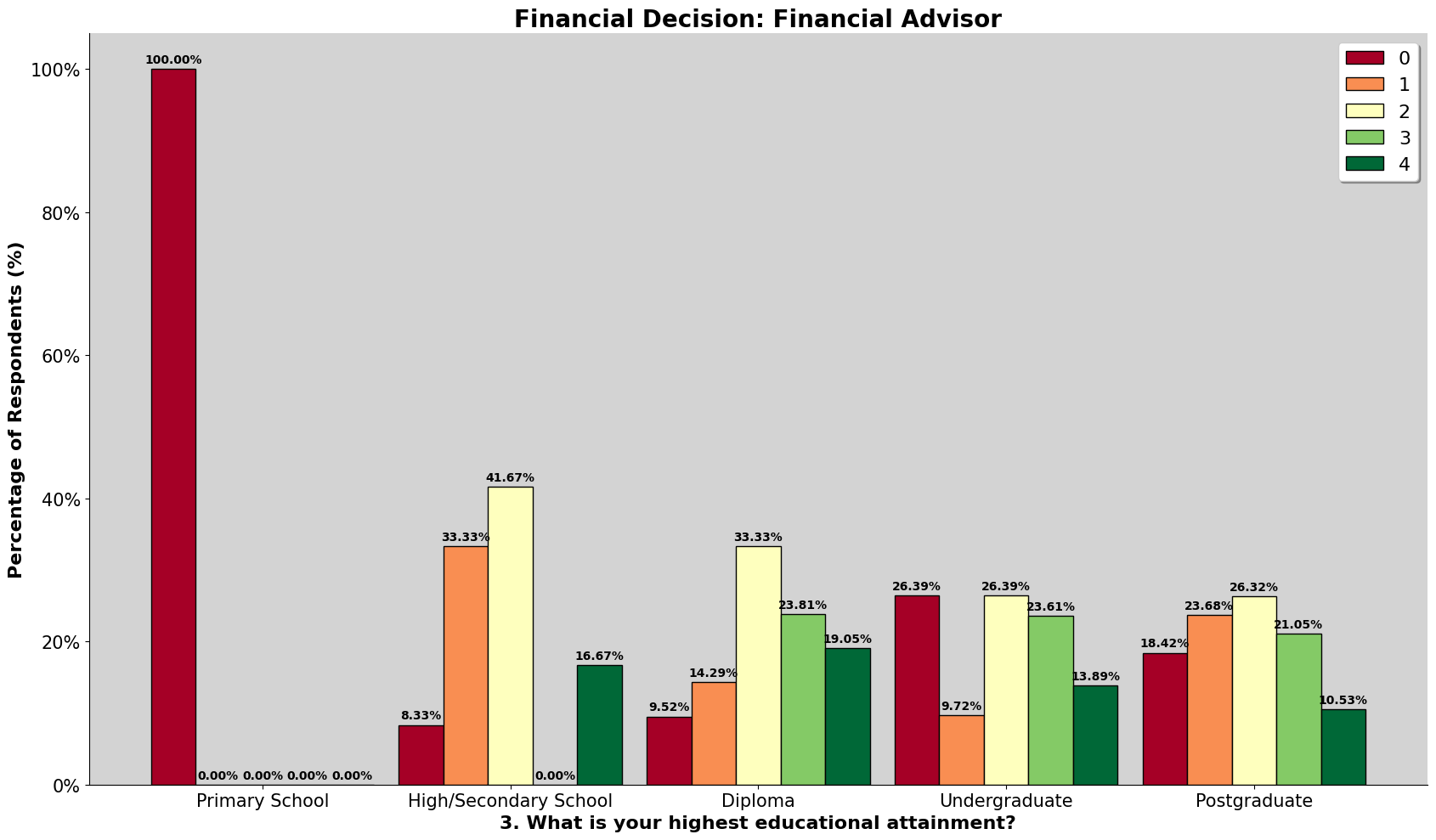

plt.show()Education Attainment

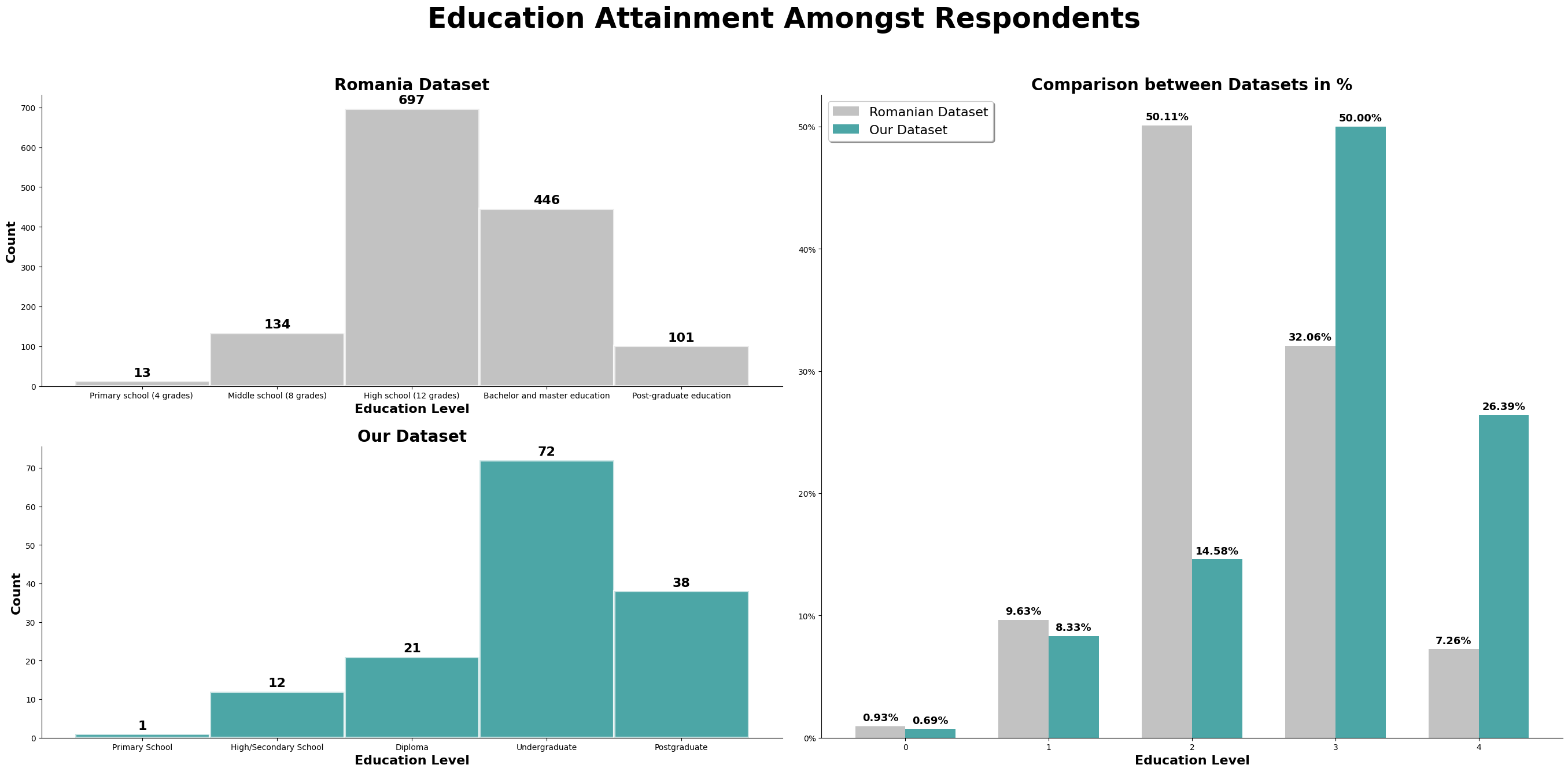

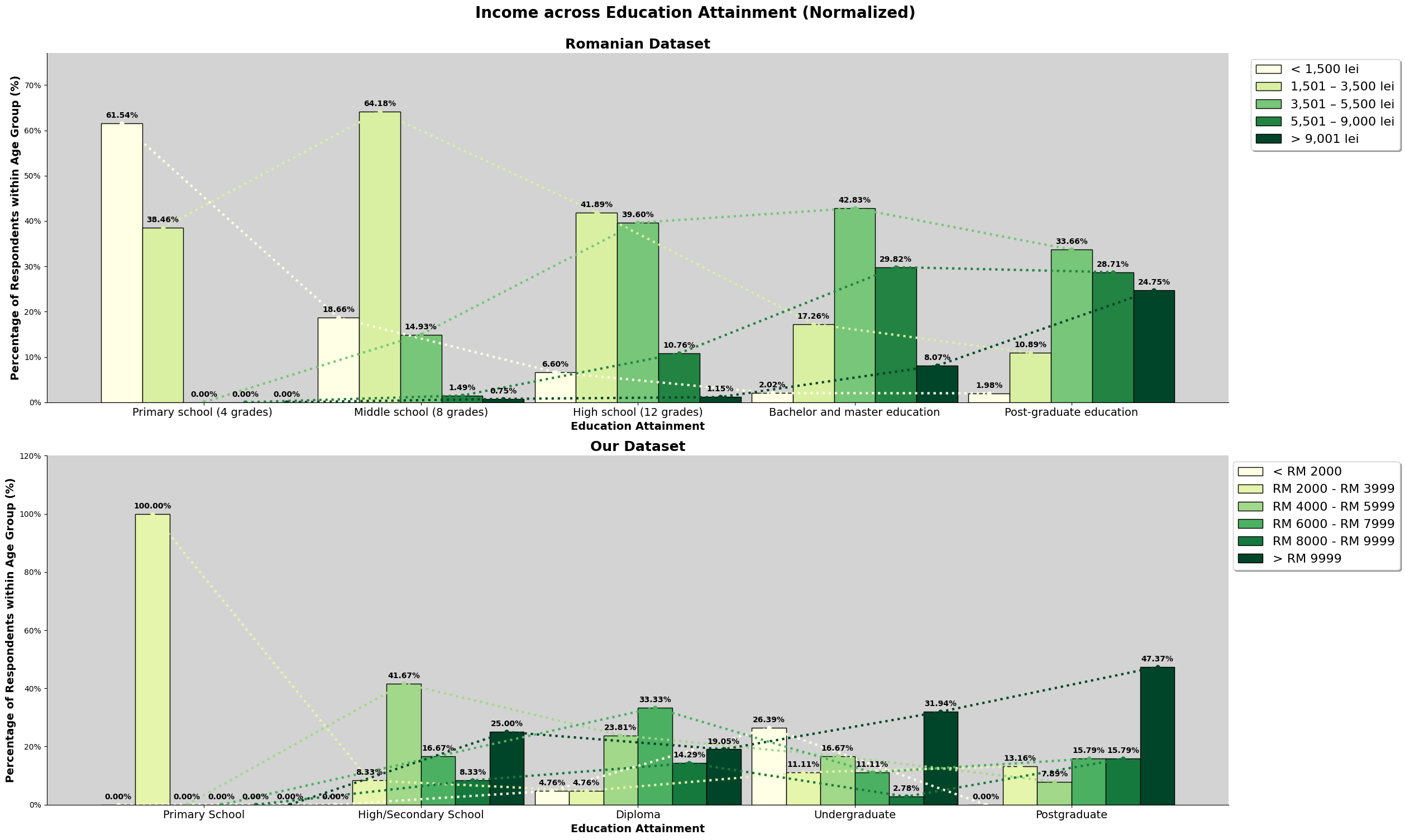

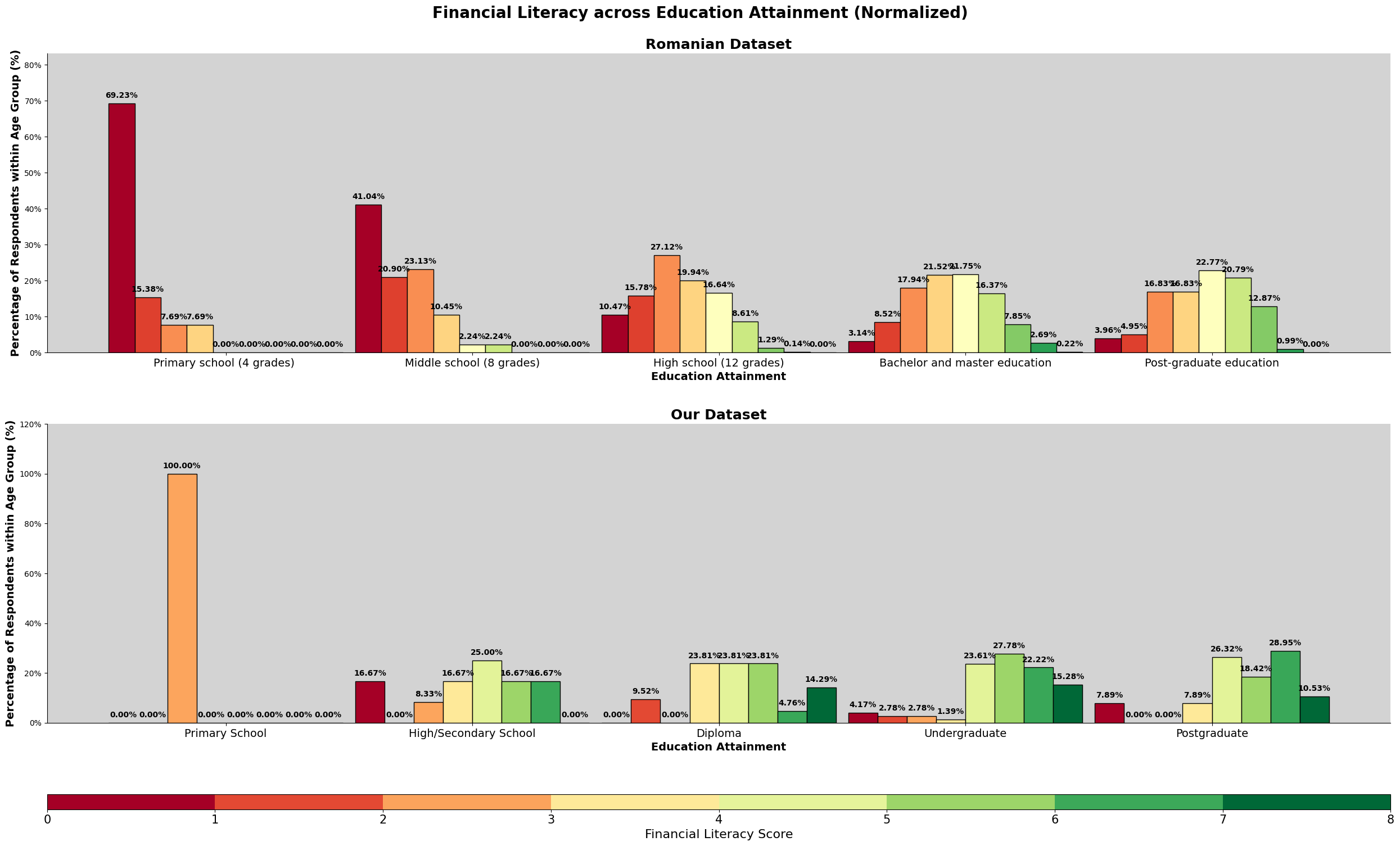

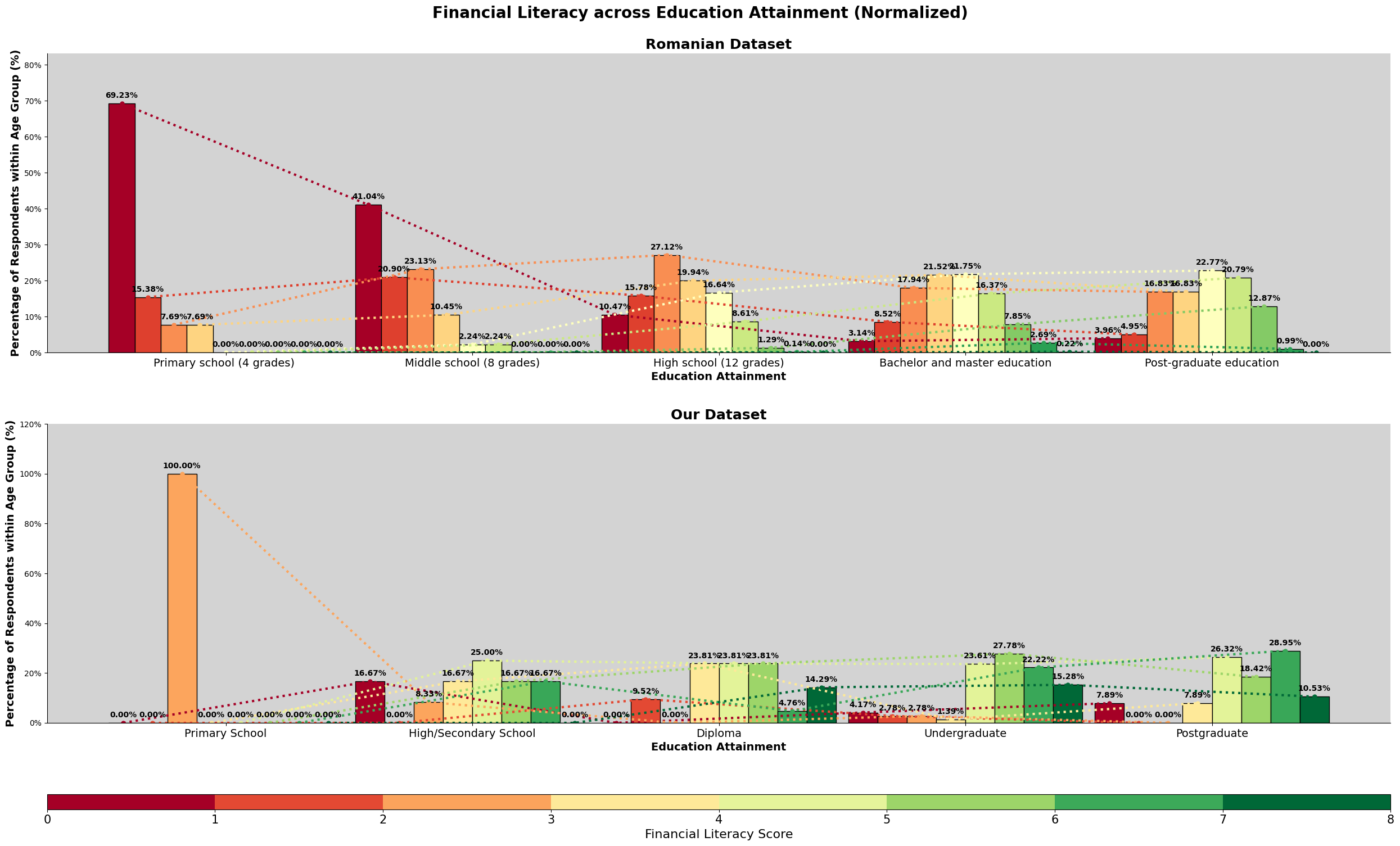

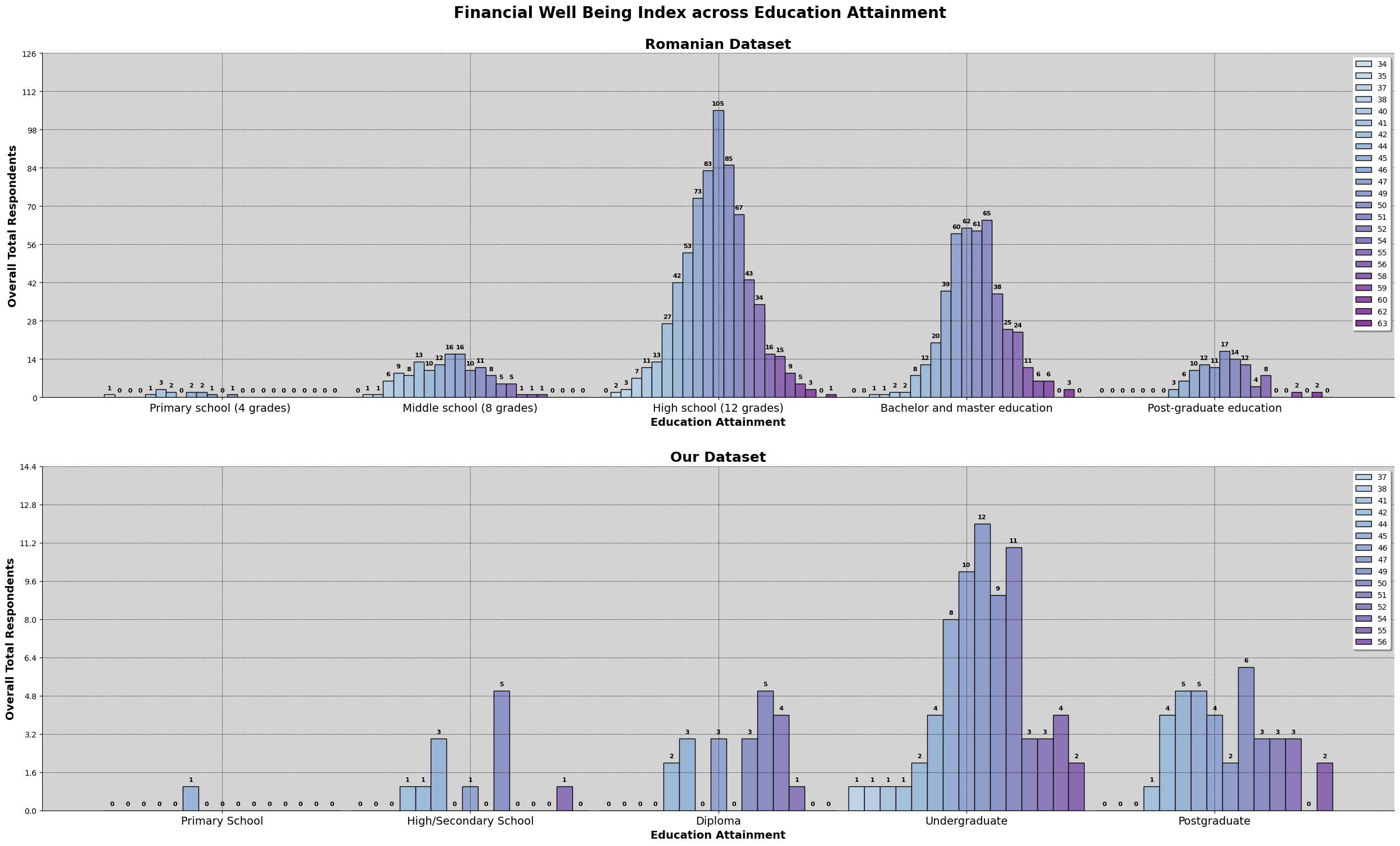

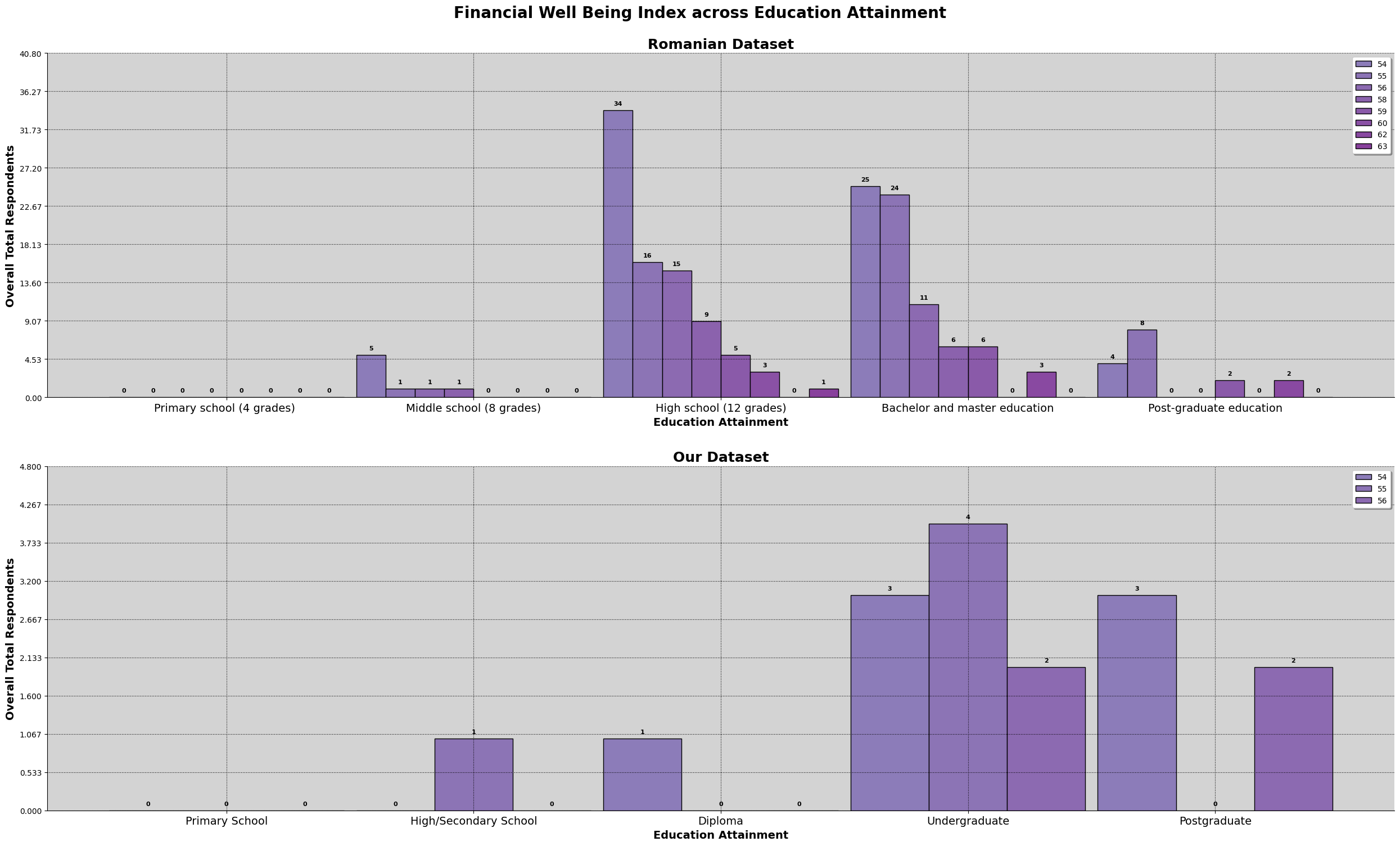

This chart above is a combined chart. It shows the number of respondent and the education level attained. The plot on the left shows the normalized value of both dataset, so we can compare to it directly.

However, we also need to take note that there are differences between the education level listed in both survey. The third level of education attaiment for the romanian dataset is 'High School (12 Grade)', which is equivalent to a college entrance exam, or Form 6 in Malaysia. However, taking up Form 6 level education in Malaysia is not a common education path, especially in Kuala Lumpur. Hence, we have made the changes to the survey question, changing 'High School (12 Grade)' to 'Diploma', making the 3rd level of education attainment not directly comparable, do refer the following link for more details on the changes made from the romanian study.

We can observe that for the romanian dataset, most of the respondents' highest education attainment is 'High School (12 Grade)'. For our dataset, it is an undergraduate degree. Both dataset has 50% of the respondents obtaining the respective common education attainment.

# Data Prepartion

# =================

# Store the column

romanian_dataset_education = romanian_dataset['SD4']

# Print the unique values

print('Unique Values (Romanian Dataset): ', list(set(romanian_dataset_education)))

# Assign a value to the unique values, according to the level of education

custom_dict_romania_education = {

'Primary school (4 grades) ': 0,

'Middle school (8 grades)': 1,

'High school (12 grades)': 2,

'Bachelor and master education': 3,

'Post-graduate education': 4

}

# Sort the dataset according the custom dict above

romanian_dataset_education = romanian_dataset_education.sort_values(

key=lambda x: x.map(custom_dict_romania_education))

# Get the count of all unique values

romanian_dataset_education_dict = getCount(romanian_dataset_education)

# Get the column string for educational attainment

our_dataset_education_string = [column for column in our_columns if 'educational' in column][0]

# Store the column

our_dataset_education = our_dataset[our_dataset_education_string]

# Print the unique values

print('Unique Values (Our Dataset): ', list(set(our_dataset_education)))

# Assign a value to the unique values, according to the level of education

custom_dict_our_education = {

'Primary School':0,

'High/Secondary School':1,

'Diploma':2,

'Undergraduate':3,

'Postgraduate': 4

}

# Sort the dataset according to the custom dict above

our_dataset_education = our_dataset_education.sort_values(key=lambda x: x.map(custom_dict_our_education))

# Get the count of all unique values

our_dataset_education_dict = getCount(our_dataset_education)

# Store the educational attainment

romanian_dataset['Educational Attainment'] = romanian_dataset['SD4'].map(custom_dict_romania_education)

our_dataset['Educational Attainment'] = our_dataset[our_dataset_education_string].map(custom_dict_our_education)

# Create percentage/ratio dataset

our_dataset_education_dict_ratio = our_dataset_education_dict.copy()

romanian_dataset_education_dict_ratio = romanian_dataset_education_dict.copy()

for key in our_dataset_education_dict_ratio:

our_dataset_education_dict_ratio[key] /= our_total_respondent

for key in romanian_dataset_education_dict_ratio:

romanian_dataset_education_dict_ratio[key] /= romanian_total_respondent

# Plot Figure

# ============

# Getting Labels

our_education_labels = list(our_dataset_education_dict.keys())

romanian_education_labels = list(romanian_dataset_education_dict.keys())

# Set figure

fig = plt.figure(layout='constrained', figsize=(27,12))

gs = GridSpec(2, 2, figure=fig) # Set two 2 x 2 grid

ax1 = fig.add_subplot(gs[0, 0]) # takes grid position 0,0 - top left

ax2 = fig.add_subplot(gs[1, 0]) # takes grid position 1,0 - bottom left

ax3 = fig.add_subplot(gs[:, 1]) # takes grid position :,0 - full right

fig.suptitle("Education Attainment Amongst Respondents", fontsize=35, fontweight='bold', y=1.1)

# Set x values and width

x = np.arange(5)

width = 0.35

# Set values to loop

datasets = [

('Romania Dataset', romanian_dataset_education_dict.values(), romanian_education_labels , 'darkgray', ax1),

('Our Dataset',our_dataset_education_dict.values(), our_education_labels, 'teal', ax2)

]

# First Column

# ==============

# Looping through values

for title, dataset, labels, color, ax in datasets:

# Set bar

bar = ax.bar(x, dataset, width=1, label=title, color=color, alpha=0.7, edgecolor='white', linewidth=3)

# Styling

ax.set_title(title, fontweight='bold', fontsize=20)

ax.set_ylabel('Count', fontweight='bold', fontsize='16')

ax.set_xlabel('Education Level', fontweight='bold', fontsize='16')

ax.bar_label(bar, padding=3, fontsize=16, fontweight='bold')

ax.set_xticks(x)

ax.set_xticklabels(labels)

ax.spines[['top', 'right']].set_visible(False)

# Second Column

# ==============

# Set bar

bar1 = ax3.bar(x - width/2, romanian_dataset_education_dict_ratio.values(), width, label = 'Romanian Dataset', color='darkgray', alpha=0.7)

bar2 = ax3.bar(x + width/2, our_dataset_education_dict_ratio.values(), width, label='Our Dataset', color='teal', alpha=0.7)

# Set bar labels

for bar in [bar1, bar2]:

ax3.bar_label(bar, fmt='{:.2%}', fontsize=13, fontweight='bold', padding=4)

# Styling

ax3.spines[['top', 'right']].set_visible(False)

ax3.legend(shadow=True, fontsize=16, loc='upper left')

ax3.set_xlabel('Education Level', fontweight='bold', fontsize='16')

ax3.set_title('Comparison between Datasets in %', fontweight='bold', fontsize=20)

formatter = mtick.PercentFormatter(xmax=1.0)

ax3.yaxis.set_major_formatter(formatter)

plt.show()Income Distribution

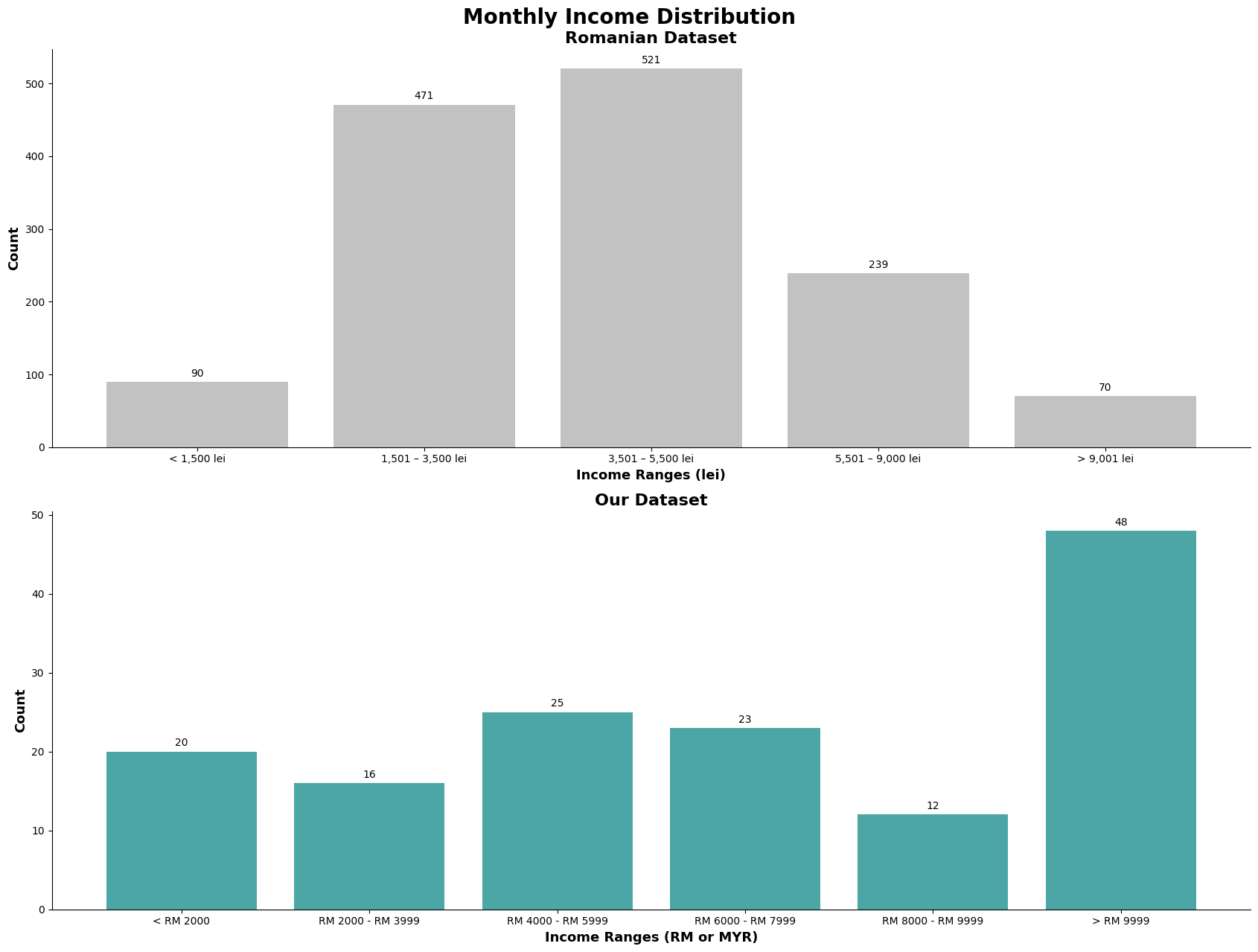

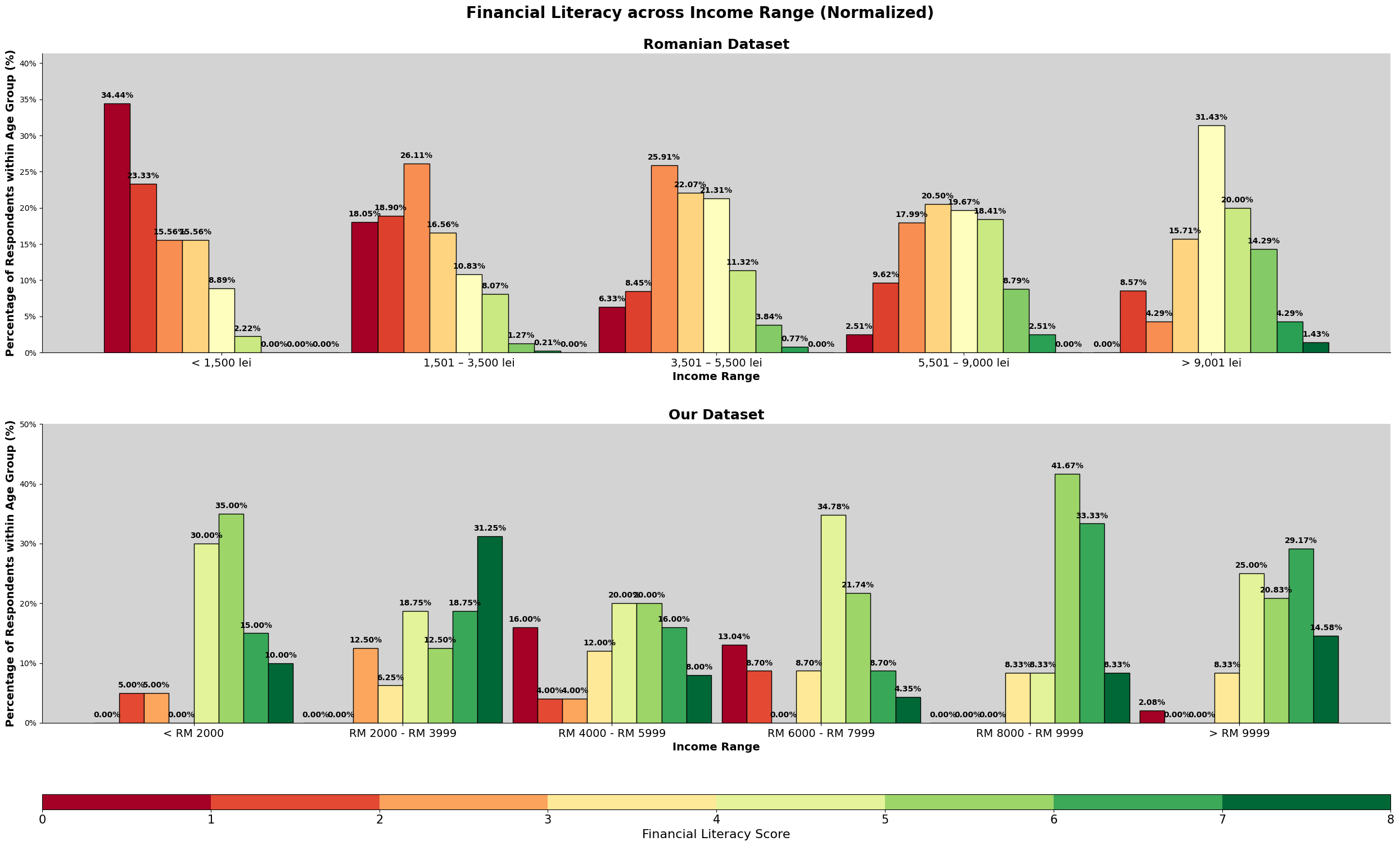

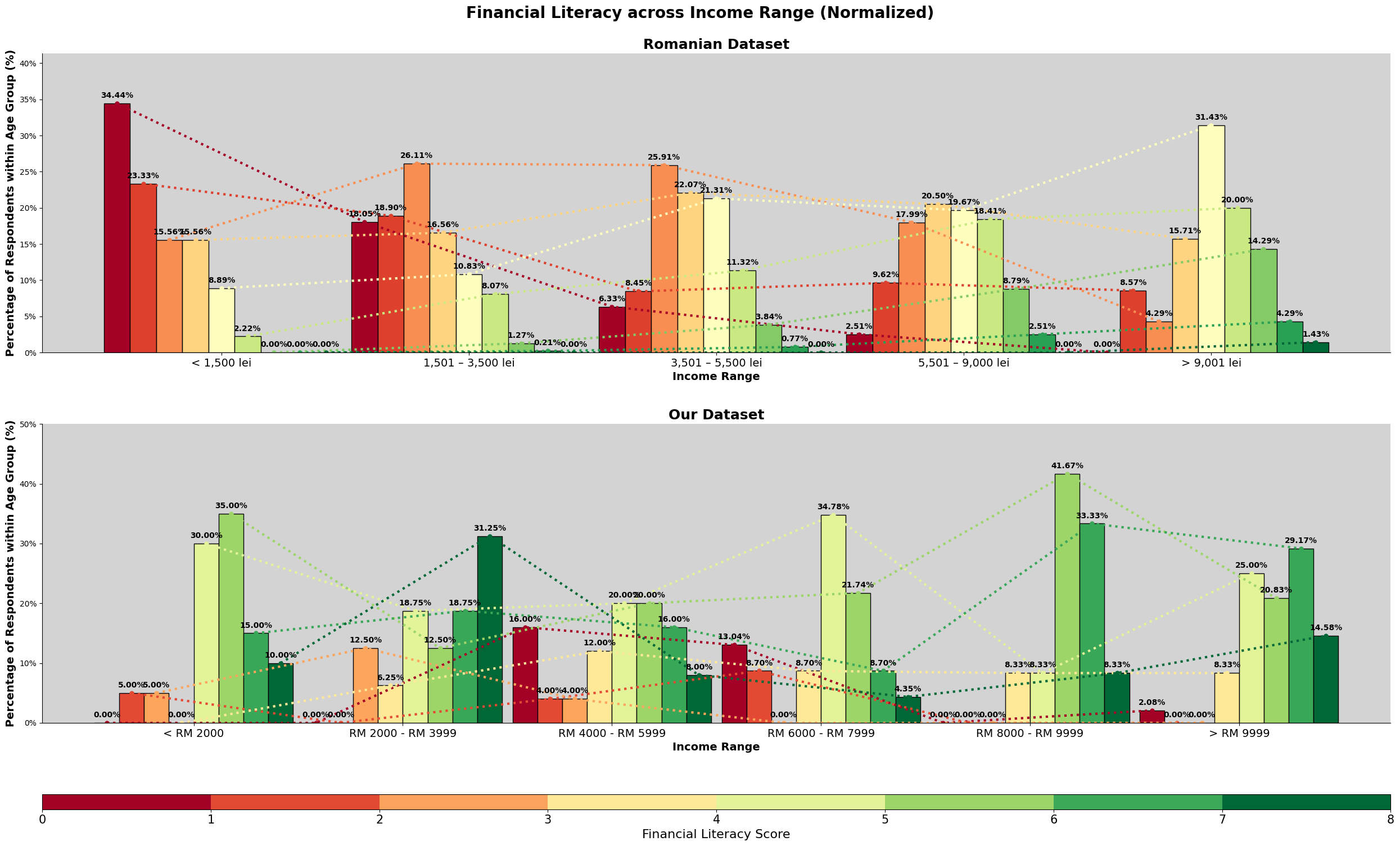

One thing to note is that, based on International Monetary Fund, for the Romanian Stats, and for the Malaysian stat. As of October 2023, we can see that Malaysia's GDP is US$430.90 billion, and the GDP per capita is US$13.03 thousands while for Romania, their GDP is US$350.41 billion and the GDP per capita is US$18.41 thousands. GDP and GDP per capita is not the ultimate financial indicator, but it is usually used as a quick overview, based on this finding, we can see that both economies have similar, but Romania has better GDP per capita as they have a population of 19 million people while Malaysia has 33 million. Additionally, 1 Romanian Leu is equivalent to 1.02 Malaysia Ringgit, which further shows the similarity in financial performance of the two countries.

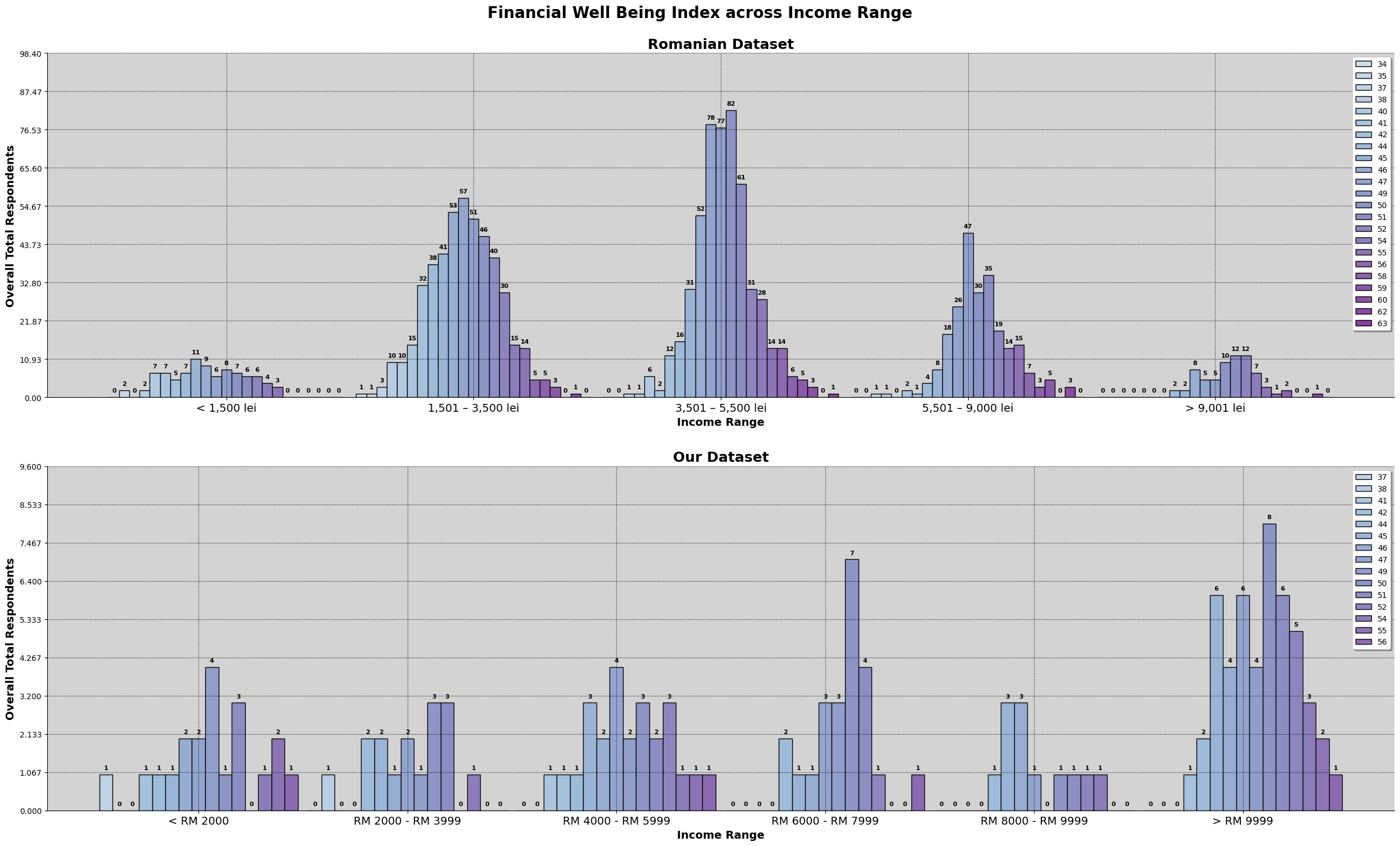

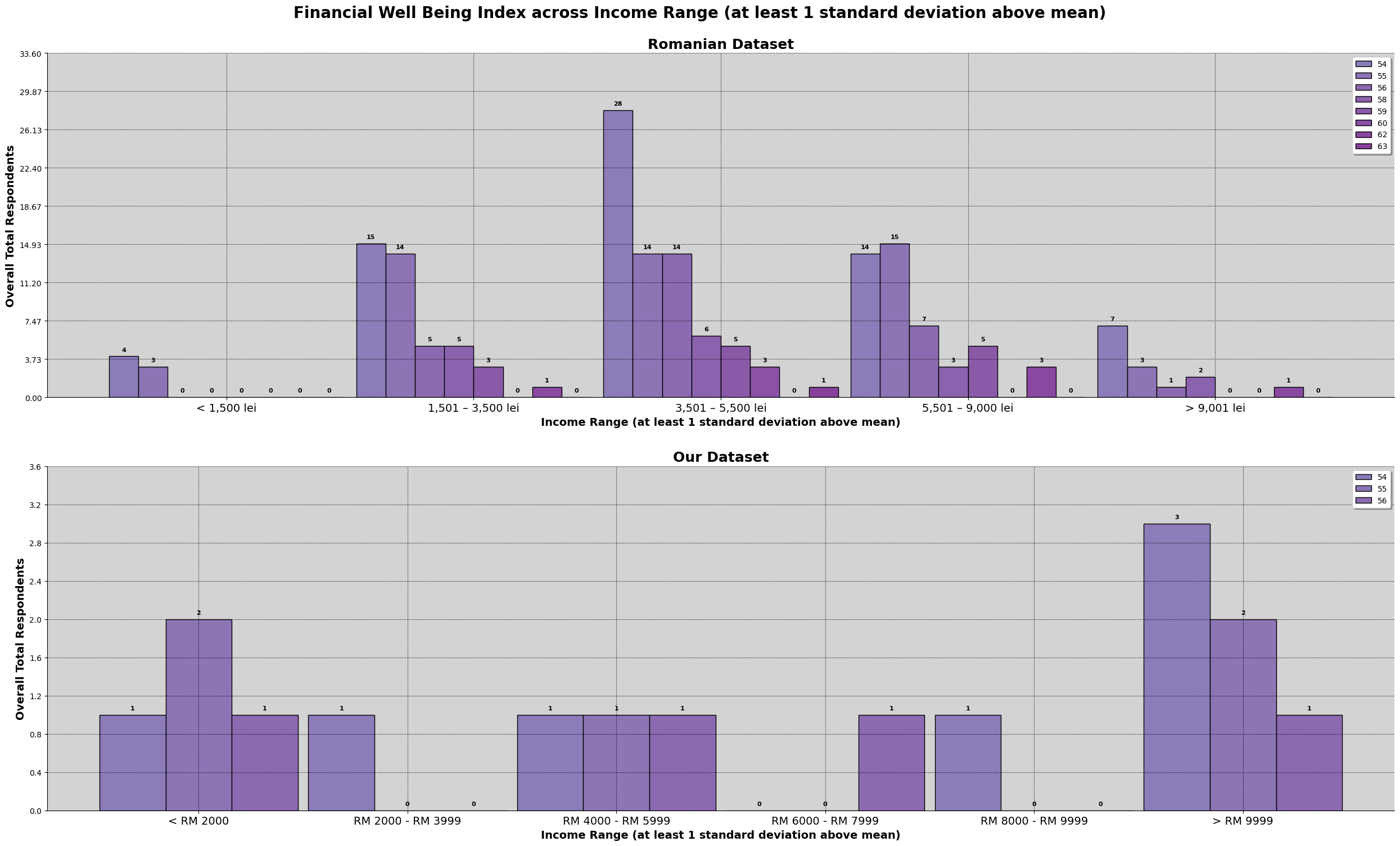

Based on the chart above, we can observe that they are many survey participants in our dataset making above the given income range set in the survey question. We will further explore income again later, like the sociodemographic make up for those who earned above RM9999. As mentioned in earlier section, there is a bias of the target audience specifically being in the area of Kuala Lumpur.

For the romanian dataset, we can see that the graph resemble a normal distribution. Meanwhile, for our dataset, about 33% of are in the '>RM9999', with an almost equal spread around the other price ranges.

# Data Preparation

# =================

romanian_dataset_income = romanian_dataset['SD7']

our_dataset_income_string = [column for column in our_columns if ' income' in column][0]

our_dataset_income = our_dataset[our_dataset_income_string]

# Print to check values - to create custom dict

print('Unique Values (Romanian Dataset):', list(set(romanian_dataset_income)))

print('Unique Values (Our Dataset): ', list(set(our_dataset_income)))

# Custom dict for sorting

custom_dict_romania_income = {

'< 1,500 lei': 0,

'1,501 – 3,500 lei': 1,

'3,501 – 5,500 lei': 2,

'5,501 – 9,000 lei': 3,

'> 9,001 lei': 4

}

custom_dict_our_income = {

'< RM 2000':0,

'RM 2000 - RM 3999':1,

'RM 4000 - RM 5999':2,

'RM 6000 - RM 7999':3,

'RM 8000 - RM 9999':4,

'> RM 9999':5,

}

# Sort the column based on the custom dict

romanian_dataset_income = romanian_dataset_income.sort_values(

key=lambda x: x.map(custom_dict_romania_income)

)

our_dataset_income = our_dataset_income.sort_values(

key=lambda x: x.map(custom_dict_our_income)

)

# Get the count values for each of the dataset

romanian_dataset_income_dict = getCount(romanian_dataset_income)

our_dataset_income_dict = getCount(our_dataset_income)

# Plot Figure

# =============

# Initialize figure

fig, (ax1, ax2) = plt.subplots(2, 1, figsize=(17, 13))

fig.suptitle('Monthly Income Distribution',

fontweight="bold", size=20)

# Set values for loop

datasets = [

(romanian_dataset_income_dict, 'darkgray', 'lei', 'Romanian Dataset', ax1),

(our_dataset_income_dict, 'teal', 'RM or MYR', 'Our Dataset', ax2)

]

# Loop values

for dataset, color, currency, title, ax in datasets:

# Set bar

bar = ax.bar(dataset.keys(), dataset.values(), color=color, alpha=0.7)

# Styling

ax.bar_label(bar, padding=3)

ax.set_xlabel(f'Income Ranges ({currency})', fontsize=13, fontweight='bold')

ax.set_ylabel('Count', fontsize=13, fontweight='bold')

ax.set_title(title, fontsize=16, fontweight='bold')

ax.spines[['top', 'right']].set_visible(False)

plt.tight_layout()

plt.show()Financial Behaviour

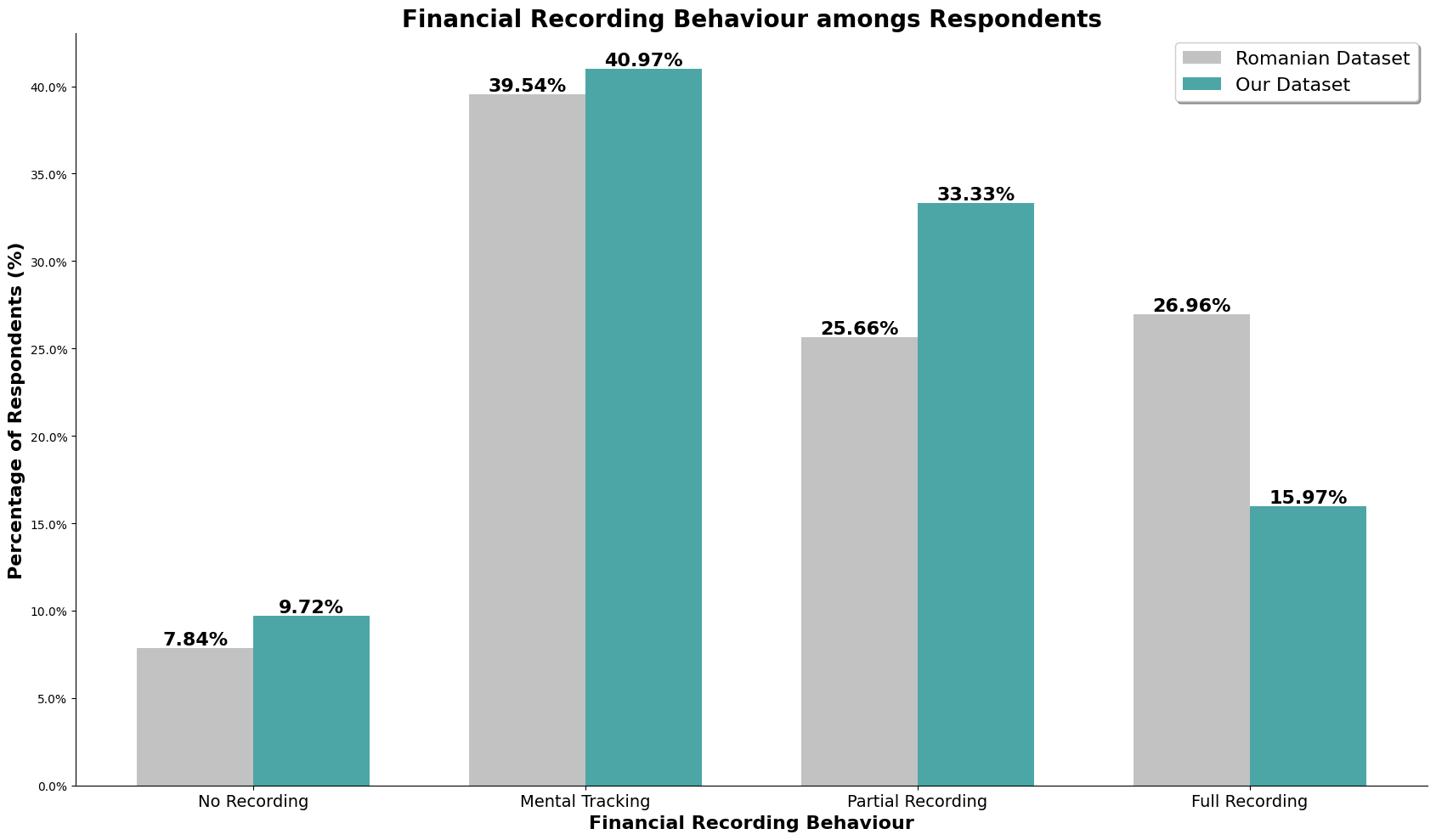

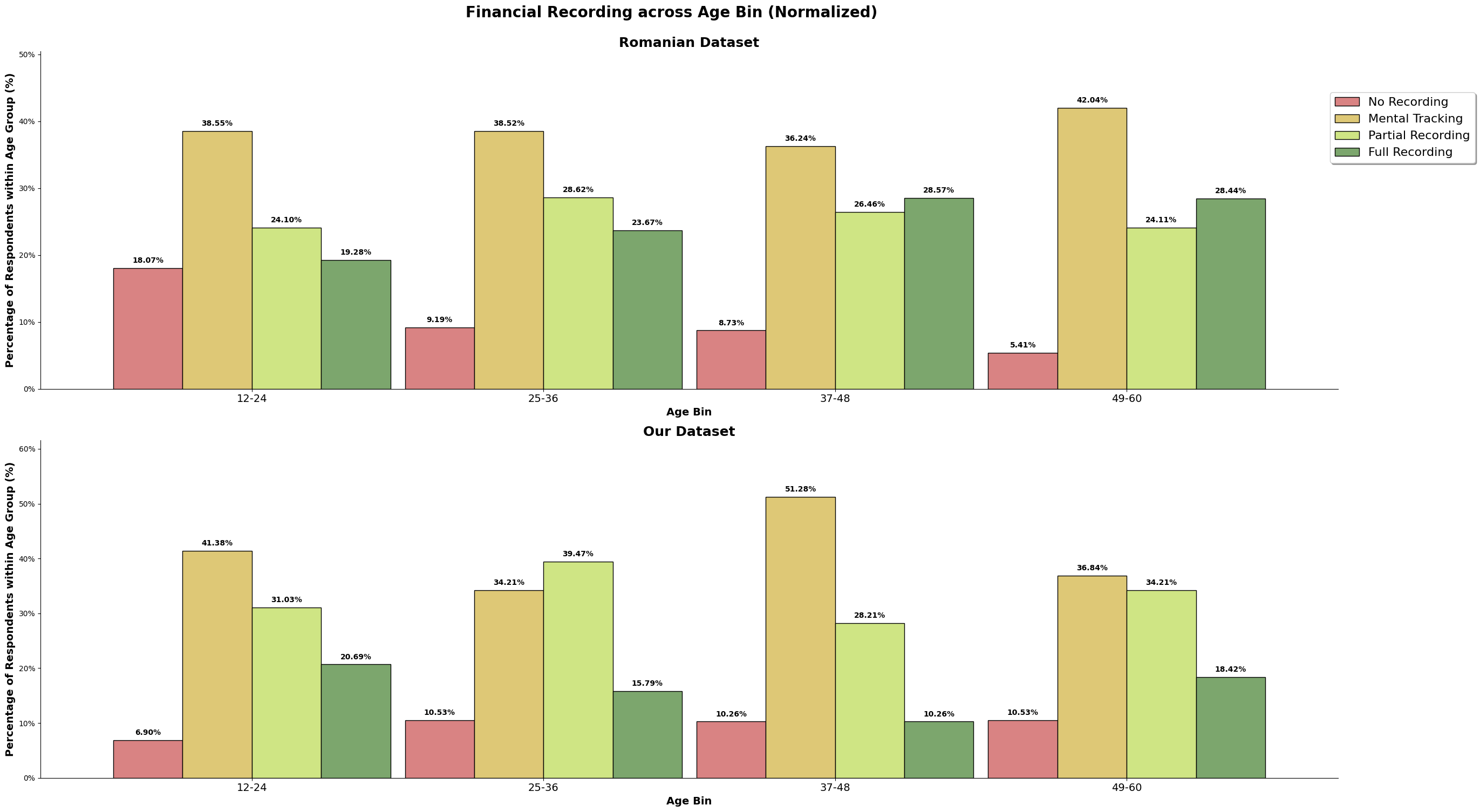

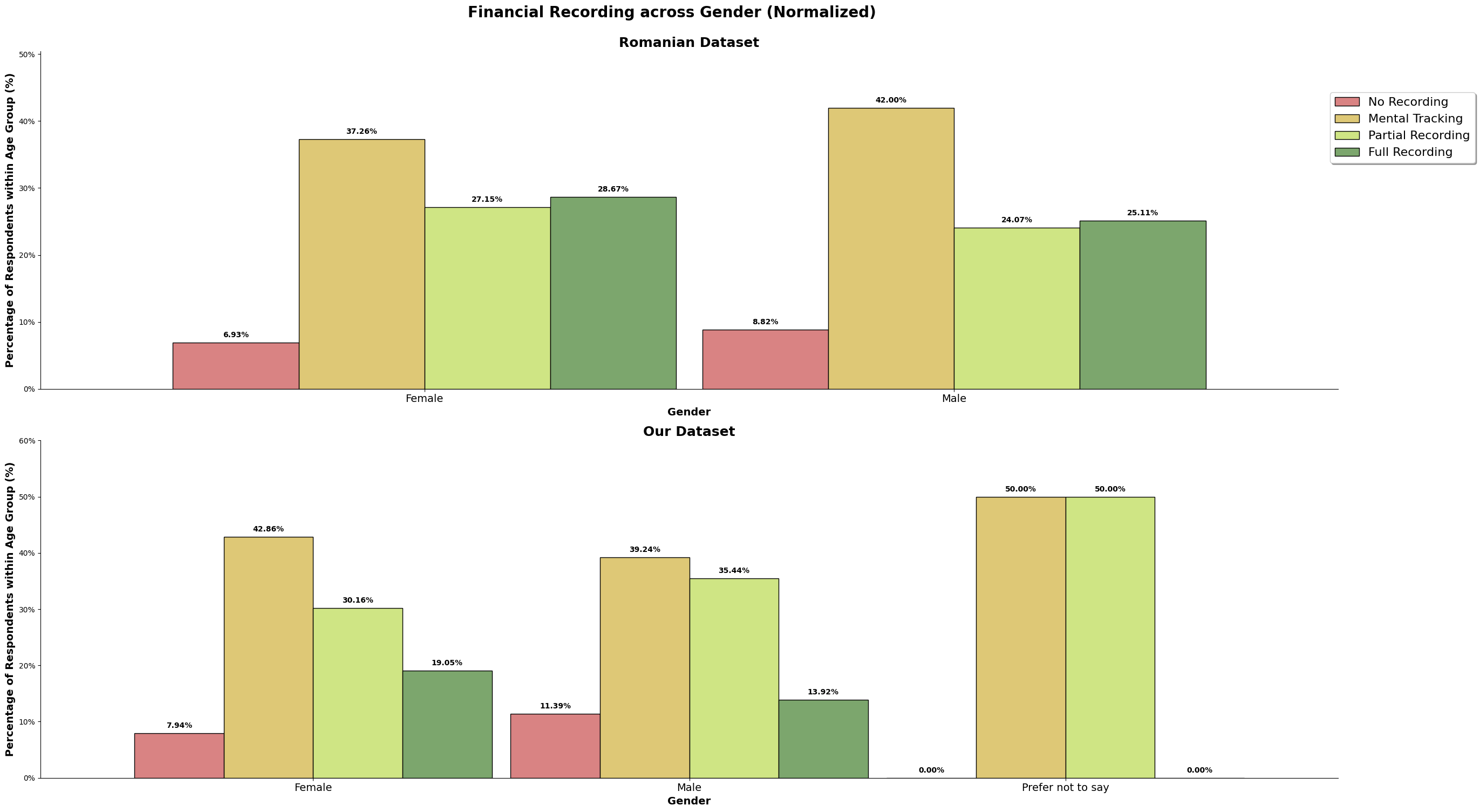

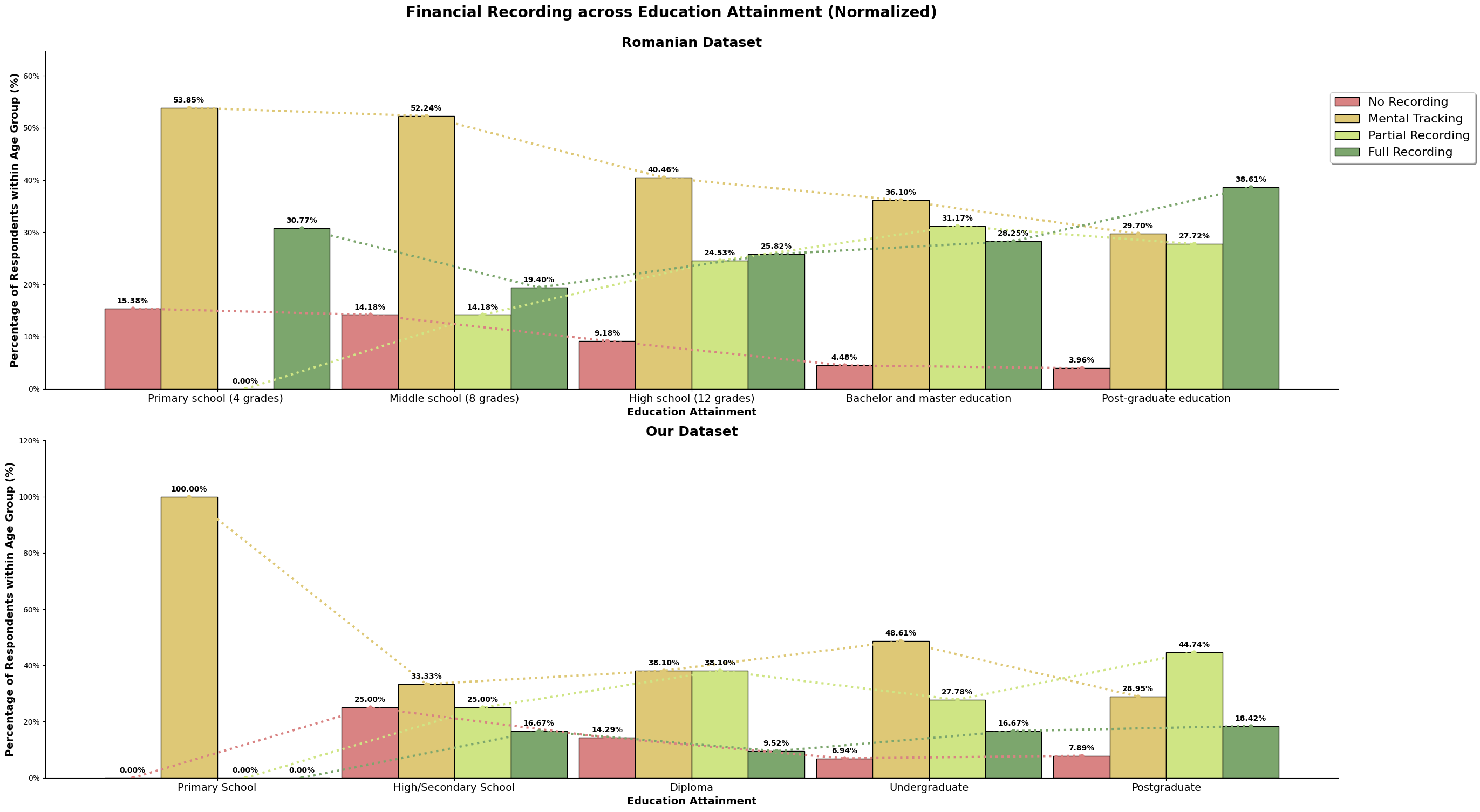

In the surveys that were conducted on our own and the Romanian study, the questions in the Financial Behaviour section were not easily coverted into quantitative or relative value that can be used to compare, except for the act of keep financial records. Hence, we will be using 'Financial Recording' question, and converting into a quantitative value. The list of questions relevant to Financial Behaviour, can be referred in the link.

Financial Recording

This is the question in the survey:

- Yes, we keep records of all revenues and all expenses.

- Yes, we keep records, but not all revenues and expenses are recorded.

- No, we don’t keep records, but we know how much money we earn and spend during a month.

- No, we don’t keep records, and we don’t know how much money we earn and spend during a month.

For the sake of simplifying the graph, we will convert the answers 1 - 4 shown above, to 'Full Recording', 'Partial Recording', 'Mental Recording' and 'No Recording'.

The above chart is the normalized value for both the dataset, so we can directly compare it. For the romanian dataset, there is about a quarter of its population that does full recording, and our dataset, there is only about 15% that does full recording. Majority population for both our and the romanian dataset only does mental tracking, where they do not keep track but understands their incomes and spending. Our dataset also has higher number of survey participants (almost 10%) who does not track at all when compared to the romanian dataset, almost 8%.

Our dataset may consist of higher number of high-earners, but we still observe our dataset having more participants that do not track their incomes and expenses, and lesser number of participants performing full recording. It could also be because our dataset is skewed to a younger audience, which is still picking up and honing their financial management skills, or it could be because high-earners is able to afford not full tracking to not tracking their income and expenses when they have understand the financial structure and habits that has been established.

# Data Preparation

# ==================

# Get our column

our_finance_record_string = getOurString(

'Do you or other person in your household keep a record of income and expenses on a monthly basis?',

our_columns)

our_dataset_finance_record = our_dataset.filter(

items=[

our_age_string,

our_finance_record_string

])

# Get romanian column

romanian_dataset_finance_record = romanian_dataset.filter(items=['SD3','I1'])

# Print unique values for custom dict

print(romanian_dataset_finance_record['I1'].unique())

print(our_dataset_finance_record[our_finance_record_string].unique())

# Create custom dict / value representation

custom_dict_our_financial_record = {

'Yes, we keep records of all income and all expenses':0,

'Yes, we keep records, but not all income and expenses are recorded':1,

'No, we don’t keep records, but we know how much money was spent during a month':2,

'No, we don’t keep records, and we don’t know how much money was spent during a month':3

}

custom_dict_romanian_financial_record = {

'Yes, we keep records of all revenues and all expenses':0,

'Yes, we keep records, but not all revenues and expenses are recorded':1,

'No, we don’t keep records, but we know how much money we earn and spend during a month': 2,

'No, we don’t keep records, and we don’t know how much money we earn and spend during a month':3

}

reverse_values = {0: 3, 1: 2, 2: 1, 3: 0}

romanian_dataset['Financial Recording'] = \

romanian_dataset['I1'].map(custom_dict_romanian_financial_record)\

.map(reverse_values)

our_dataset['Financial Recording'] = \

our_dataset[our_finance_record_string].map(custom_dict_our_financial_record)\

.map(reverse_values)

our_dataset_financial_recording_dict = our_dataset['Financial Recording']\

.value_counts(normalize=True)\

.sort_index().to_dict()

romanian_dataset_financial_recording_dict = romanian_dataset['Financial Recording']\

.value_counts(normalize=True)\

.sort_index().to_dict()

# Plot Figure

# ===========

# Create figure

fig, ax = plt.subplots(figsize=(17,10))

# Custom Label

financial_recording_label = ['No Recording', 'Mental Tracking', 'Partial Recording', 'Full Recording' ]

# Set x values and width

x = np.arange(4)

width = 0.35

# Plot both datasets on same axes with appropriate offsets

bar1 = ax.bar(x - width/2, romanian_dataset_financial_recording_dict.values(), width, label='Romanian Dataset',

color='darkgray', alpha=0.7)

bar2 = ax.bar(x + width/2, our_dataset_financial_recording_dict.values(), width, label='Our Dataset',

color='teal', alpha=0.7)

for bar in [bar1, bar2]:

ax.bar_label(bar, fontsize='16', fontweight='bold', fmt='{:.2%}')

# Styling

ax.set_title('Financial Recording Behaviour amongs Respondents', fontsize='20', fontweight='bold')

ax.set_ylabel('Percentage of Respondents (%)', fontsize=16, fontweight='bold')

ax.set_xlabel('Financial Recording Behaviour', fontsize=16, fontweight='bold')

ax.set_xticks(x)

ax.set_xticklabels(financial_recording_label, fontsize=14)

ax.spines[['top', 'right']].set_visible(False)

ax.legend(shadow=True, fontsize='16')

formatter = mtick.PercentFormatter(xmax=1.0, decimals=None)

ax.yaxis.set_major_formatter(formatter)

plt.tight_layout()

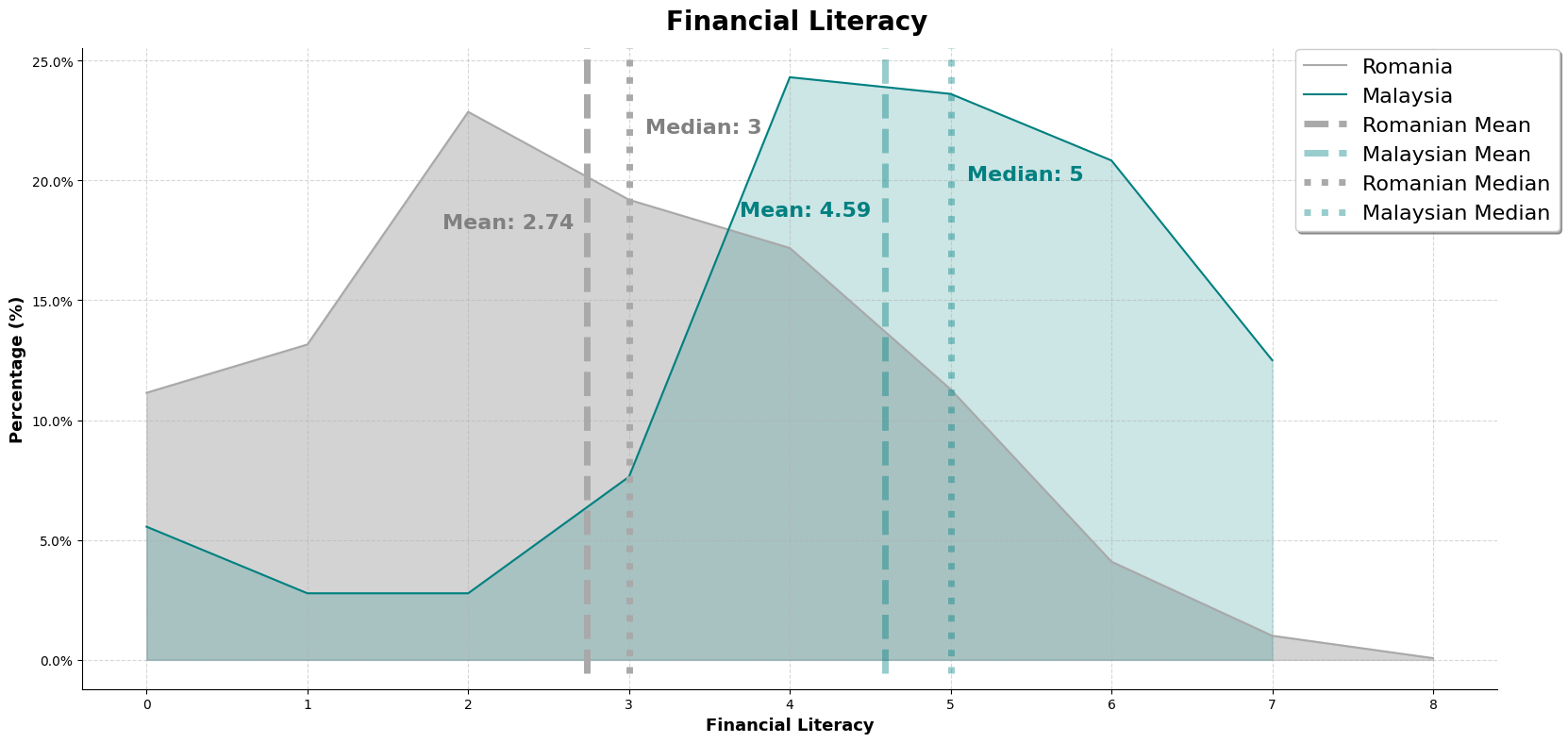

plt.show()Financial Literacy

Based on the Romanian study, financial literacy is calculate by the sum of all the correct answer, each having 1 point, and a maximum of 8. They have included the 'Big Three' and 'Big Five' question, referenced from Lusardi and Mitchell. This can be seen being utilized by Global Financial Literacy Excellence Center shown in the following link. The 'Big Three' and 'Big Five' Questions for Financial Literacy.. Also, by the Financial Industry Regulatory Authority (FINRA), as shown in the following link, financial knowlege quiz by FINRA.

So, we have to aggregate the scores from the survey and get the financial literacy score for each particpants. The list of questions in the survey can be referred here.

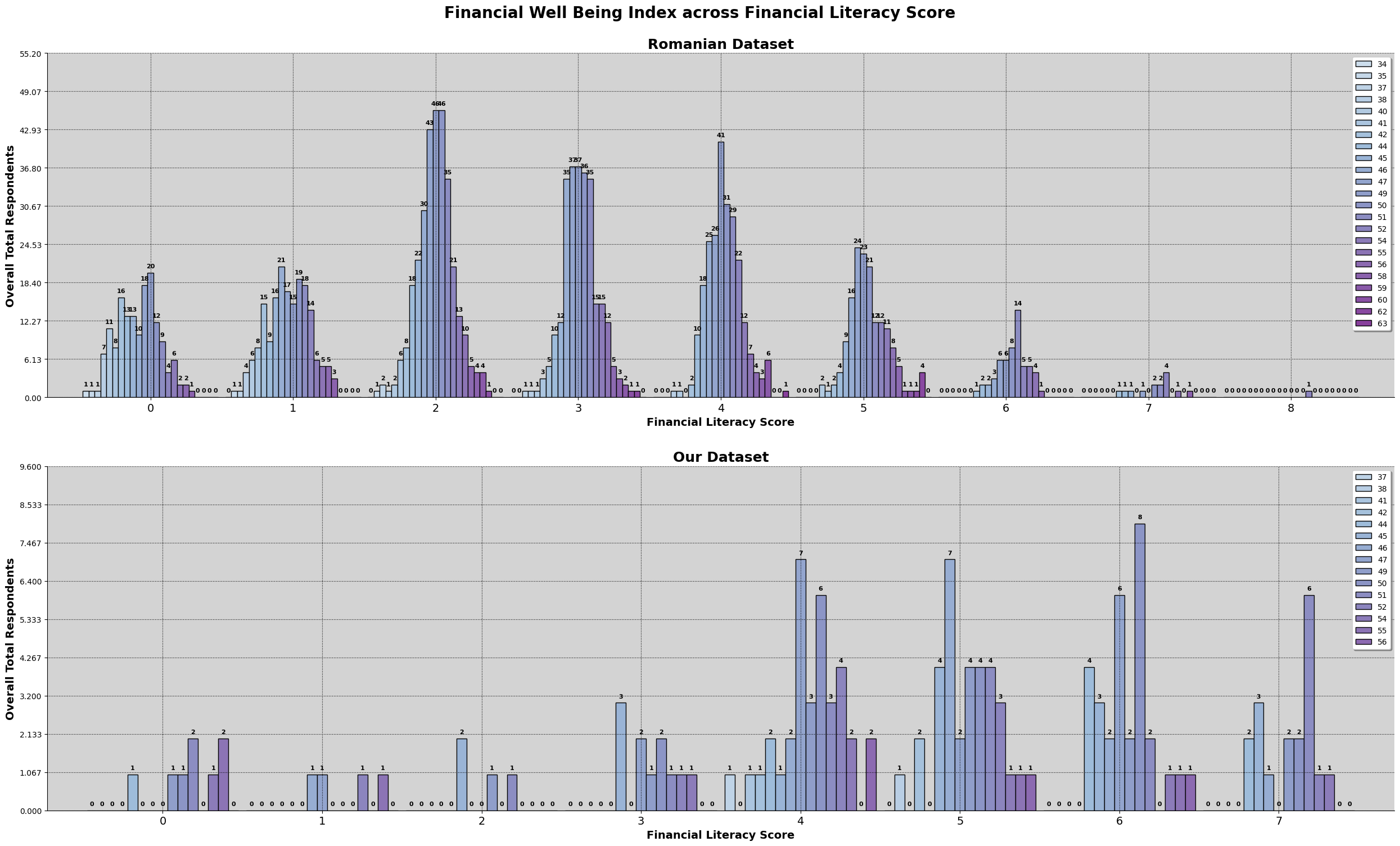

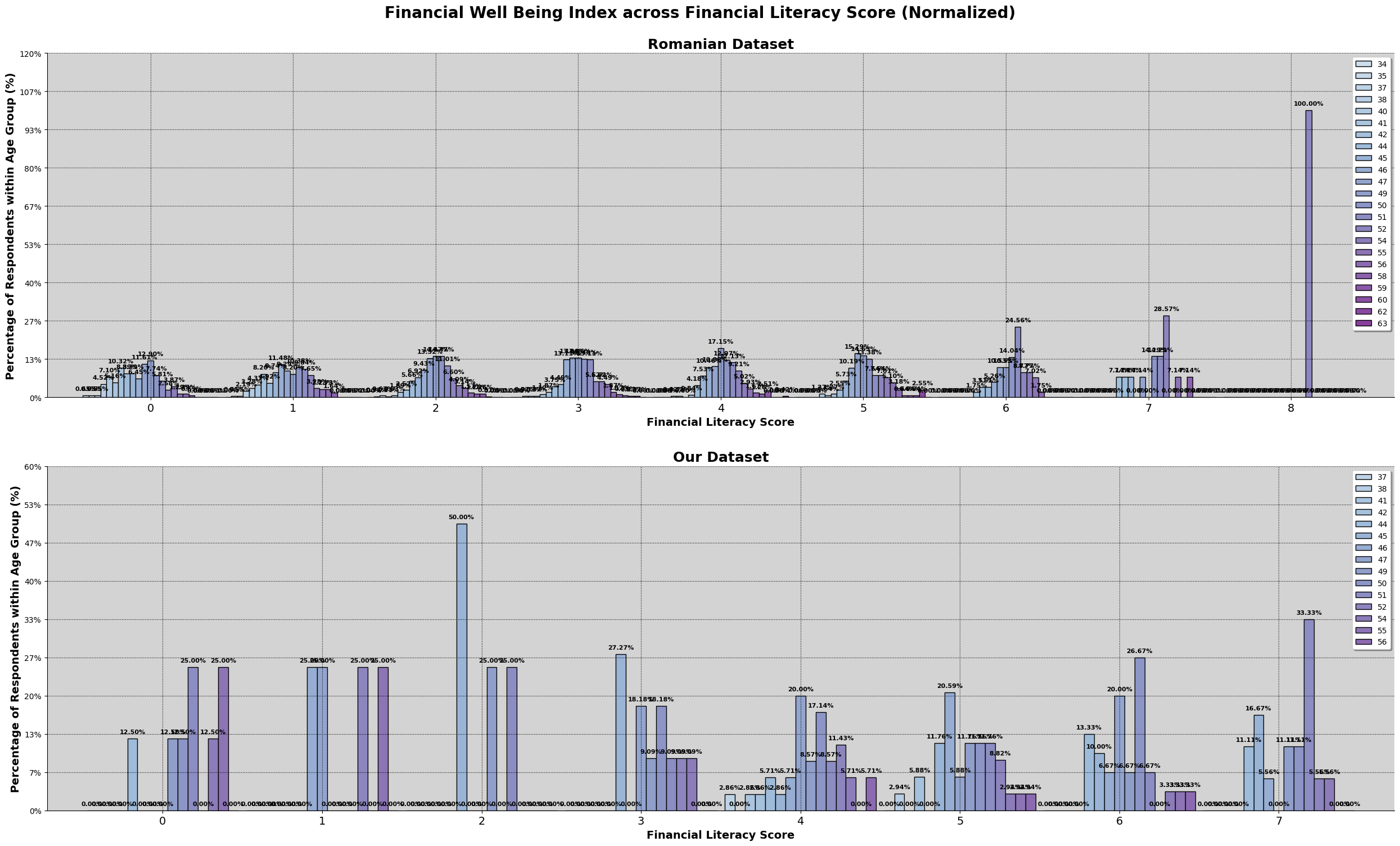

As shown by the result, there are a higher percentage of romanian participants scoring 2 while malaysian participants are scoring at 4. This is also evident by the mean and median line shown. But there are instances of romanian participants scoring above 6 while malaysian does not have any. We will further explore the relationship between financial literacy, financial well being and the sociodemographic and financial attitudes factors.

# Score Aggregation

# ==================

# Function to replace values in the column

def replace_values(col_no, answer, dataset, col_set):

# Replacing correct answer with 1

dataset[col_set[col_no]] = dataset[col_set[col_no]].replace(answer, 1)

# Replacing wrong answer with 0

dataset[col_set[col_no]] = np.where(

dataset[col_set[col_no]] != 1, 0, dataset[col_set[col_no]]

)

return dataset

# To store the required columns -- For Romanian Dataset

romanian_financial_literacy_columns = []

# Base String

base_string = 'C'

# Loop from 1 to 8

for sub_string in range(1,9):

romanian_financial_literacy_columns.append(

base_string + str(sub_string)

)

# To store the require columns -- For Our Dataset

our_financial_literacy_columns = [our_columns[x] for x in range(42,50)]

# Printing unique values for reference

for col in romanian_financial_literacy_columns:

print(romanian_dataset[col].unique())

# Printing unique values for reference

for col in our_financial_literacy_columns:

print(our_dataset[col].unique())

# Coverting answeres into values

# =====================================

romanian_financial_literacy = romanian_dataset[romanian_financial_literacy_columns]

our_financial_literacy = our_dataset[our_financial_literacy_columns]

# Probability

column_no = 0

romanian_financial_literacy = replace_values(

column_no, '1 in 1,000,000', romanian_financial_literacy, romanian_financial_literacy_columns

)

our_financial_literacy = replace_values(

column_no, '1 in 100000', our_financial_literacy, our_financial_literacy_columns

)

# Interest Rate

column_no = 1

romanian_financial_literacy = replace_values(

column_no, 'More than LEI 150 ', romanian_financial_literacy, romanian_financial_literacy_columns

)

our_financial_literacy = replace_values(

column_no, 'More than $150', our_financial_literacy, our_financial_literacy_columns

)

# Loan Repayment

column_no = 2

romanian_financial_literacy = replace_values(

column_no, 'True', romanian_financial_literacy, romanian_financial_literacy_columns

)

print(our_financial_literacy[our_financial_literacy_columns[column_no]].unique())

our_financial_literacy = replace_values(

column_no, 'True', our_financial_literacy, our_financial_literacy_columns

)

# Time value of money

column_no = 3

romanian_financial_literacy = replace_values(

column_no, 'My friend', romanian_financial_literacy, romanian_financial_literacy_columns

)

our_financial_literacy = replace_values(

column_no, 'My friend', our_financial_literacy, our_financial_literacy_columns

)

# Inflation

column_no = 4

romanian_financial_literacy = replace_values(

column_no, 'The same', romanian_financial_literacy, romanian_financial_literacy_columns

)

our_financial_literacy = replace_values(

column_no, 'The Same', our_financial_literacy, our_financial_literacy_columns

)

# Investment

column_no = 5

romanian_financial_literacy = replace_values(

column_no, 'Multiple business of investments', romanian_financial_literacy, romanian_financial_literacy_columns

)

our_financial_literacy = replace_values(

column_no, 'Multiple Business of Investment', our_financial_literacy, our_financial_literacy_columns

)

# Asset

column_no = 6

romanian_financial_literacy = replace_values(

column_no, 'Stocks', romanian_financial_literacy, romanian_financial_literacy_columns

)

our_financial_literacy = replace_values(

column_no, 'Stocks', our_financial_literacy, our_financial_literacy_columns

)

# Risk

column_no = 7

romanian_financial_literacy = replace_values(

column_no, 'Stocks', romanian_financial_literacy, romanian_financial_literacy_columns

)

our_financial_literacy = replace_values(

column_no, 'Stocks', our_financial_literacy, our_financial_literacy_columns

)

# Data Preparation

# ==================

# Getting the score

romanian_financial_literacy['Financial Literacy Score'] = \

romanian_financial_literacy[romanian_financial_literacy_columns]\

.sum(axis=1).astype(int)

our_financial_literacy['Financial Literacy Score'] = \

our_financial_literacy[our_financial_literacy_columns]\

.sum(axis=1).astype(int)

romanian_dataset['Financial Literacy Score'] = romanian_financial_literacy['Financial Literacy Score']

our_dataset['Financial Literacy Score'] = our_financial_literacy['Financial Literacy Score']

# Get unique values of the financial well being index, and sort them in ascending order

# The plot will get wonky if it is not in order

romanian_financial_literacy_x = \

np.sort(romanian_financial_literacy['Financial Literacy Score'].unique())

our_financial_literacy_x = \

np.sort(our_financial_literacy['Financial Literacy Score'].unique())

# Get the value count of each score, and then divide it by the size of each dataset

romanian_financial_literacy_y = \

romanian_financial_literacy['Financial Literacy Score']\

.value_counts().get(romanian_financial_literacy_x)\

/ len(romanian_financial_literacy)

our_financial_literacy_y = \

our_financial_literacy['Financial Literacy Score']\

.value_counts().get(our_financial_literacy_x)\

/len(our_financial_literacy)

# Get the mean value for financial literacy score

romanian_financial_literacy_mean = romanian_financial_literacy['Financial Literacy Score'].mean()

our_financial_literacy_mean = our_financial_literacy['Financial Literacy Score'].mean()

# Get the median values for financial literacy score

romanian_financial_literacy_median = romanian_financial_literacy['Financial Literacy Score'].median()

our_financial_literacy_median = our_financial_literacy['Financial Literacy Score'].median()

# Get the standard deviation value for financial literacy score

romanian_financial_literacy_std = romanian_financial_literacy['Financial Literacy Score'].std()

our_financial_literacy_std = our_financial_literacy['Financial Literacy Score'].std()

# Initializing the figure

figure, ax = plt.subplots(figsize=(17,8))

figure.suptitle(

'Financial Literacy',

fontweight = 'bold',

fontsize = 20

)

# Plot romania data

# =================

ax.plot(

romanian_financial_literacy_x,

romanian_financial_literacy_y,

color = 'darkgray',

label = 'Romania'

)

ax.fill_between(

romanian_financial_literacy_x,

romanian_financial_literacy_y,

alpha = 0.5,

color = 'darkgray'

)

# Plot our data

# ==============

ax.plot(

our_financial_literacy_x,

our_financial_literacy_y,

color = 'teal',

label = 'Malaysia'

)

ax.fill_between(

our_financial_literacy_x,

our_financial_literacy_y,

alpha = 0.2,

color = 'teal'

)

# Mean line and annotations

# ==========================

ax.axvline(

romanian_financial_literacy_mean,

0.025,

ls = '--',

color = 'darkgray',

label = 'Romanian Mean',

linewidth = 5

)

ax.annotate(

f"Mean: {romanian_financial_literacy_mean:.3g}",

xy=(romanian_financial_literacy_mean - 0.9 ,0.18),

fontsize=16, fontweight='bold', color='grey')

ax.axvline(

our_financial_literacy_mean,

0.025,

ls = '--',

color = 'teal',

label = 'Malaysian Mean',

alpha = 0.4,

linewidth = 5

)

ax.annotate(

f"Mean: {our_financial_literacy_mean:.3g}",

xy=(our_financial_literacy_mean - 0.9 ,0.185),

fontsize=16, fontweight='bold', color='teal')

# Median Line and annotations

# =============================

ax.axvline(

romanian_financial_literacy_median,

0.025,

ls = ':',

color = 'darkgray',

label = 'Romanian Median',

linewidth = 5

)

ax.annotate(

f"Median: {romanian_financial_literacy_median:.3g}",

xy=(romanian_financial_literacy_median + 0.1 ,0.22),

fontsize=16, fontweight='bold', color='grey')

ax.axvline(

our_financial_literacy_median,

0.025,

ls = ':',

color = 'teal',

label = 'Malaysian Median',

alpha = 0.4,

linewidth = 5

)

ax.annotate(

f"Median: {our_financial_literacy_median:.3g}",

xy=(our_financial_literacy_median + 0.1 ,0.20),

fontsize=16, fontweight='bold', color='teal')

# Styling

ax.set_ylabel('Percentage (%)', fontsize=13, fontweight='bold')

ax.set_xlabel('Financial Literacy', fontsize=13, fontweight='bold')

ax.legend(fontsize = 16, shadow=True, bbox_to_anchor=(0.85,1.015))

ax.spines[['top', 'right']].set_visible(False)

formatter = mtick.PercentFormatter(xmax=1.0)

ax.yaxis.set_major_formatter(formatter)

ax.grid(alpha=0.5, linestyle='--')

# Optimize layout and show figure

plt.tight_layout()

plt.show()

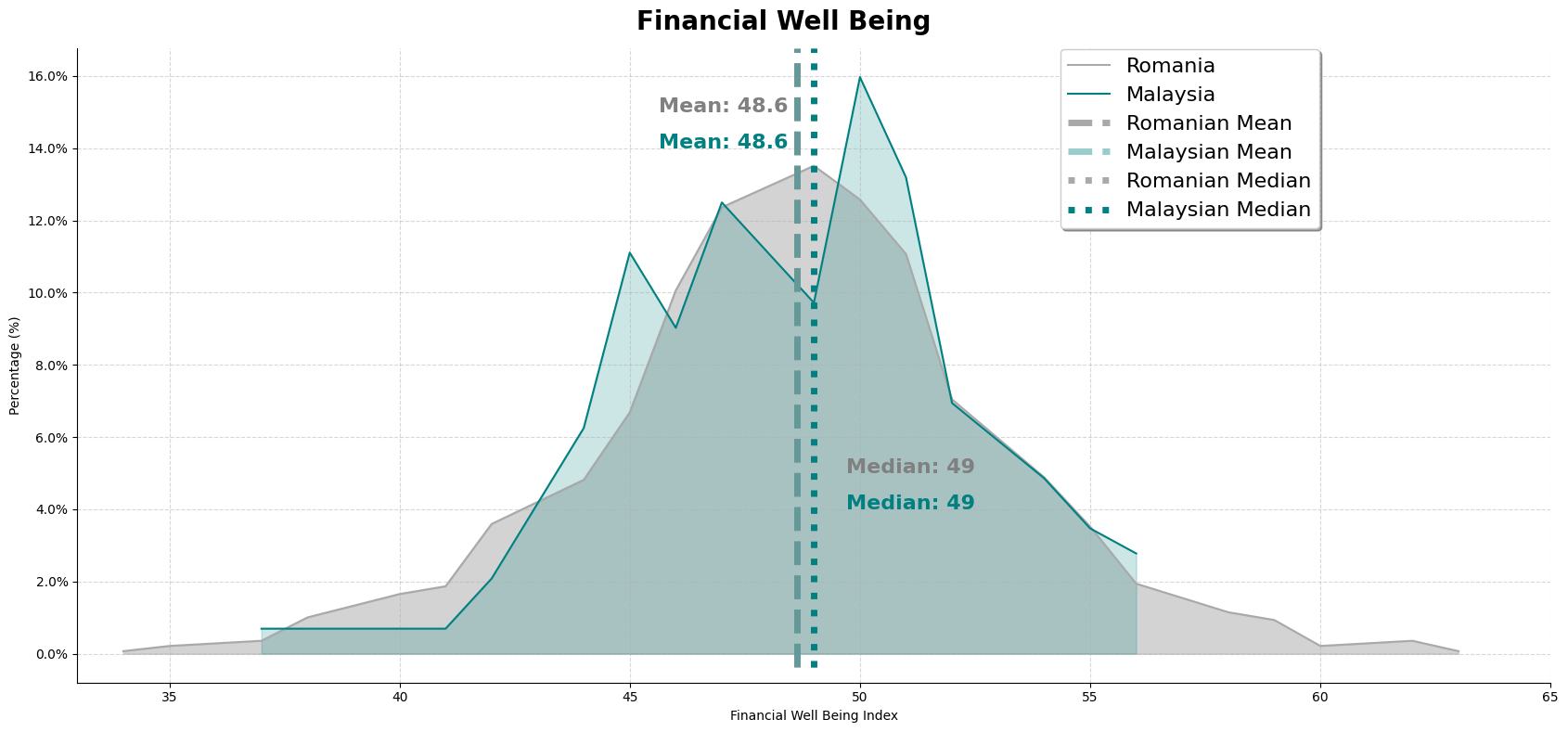

Financial Well-Being

Financial Well-Being is the ability of an individual to fulfill their current and future financial obligations but also unforeseen financial situation and still being able to have the freedom to enjoy life. This was defined in the romanian study, which was referencing the Consumer Financial Protection Bureau (CFPB), which it can be seen in the following link: resources provided by CFPB.

Based on the romanian study, they have applied the method of measuring Financial Well Being, from CFPB and Organisation for Economic Co-operation and Development (OECD). We will be following the methods applied by romanian study, so that we can make direct comparisons to it. The following link: Financial Well Being User Guide Scale is where CFPB explained how to use the questionnaire as well as getting the result. The financial well being score table shown in the appendix is the Financial Well Being Scale score, in which It is also mentioned in the romanian paper that, because score are in between values of 16 to 91, values up to 40 indicate that individuals are facing financial difficulties, values between 41 to 50 are might consider 'living paycheck to paycheck', 51 to 60 are individuals who have more stable finances and for those of higher than 60, represent having financial stability most of the time. Lastly, those who score a value of higher than 70 are people with universal financial security.

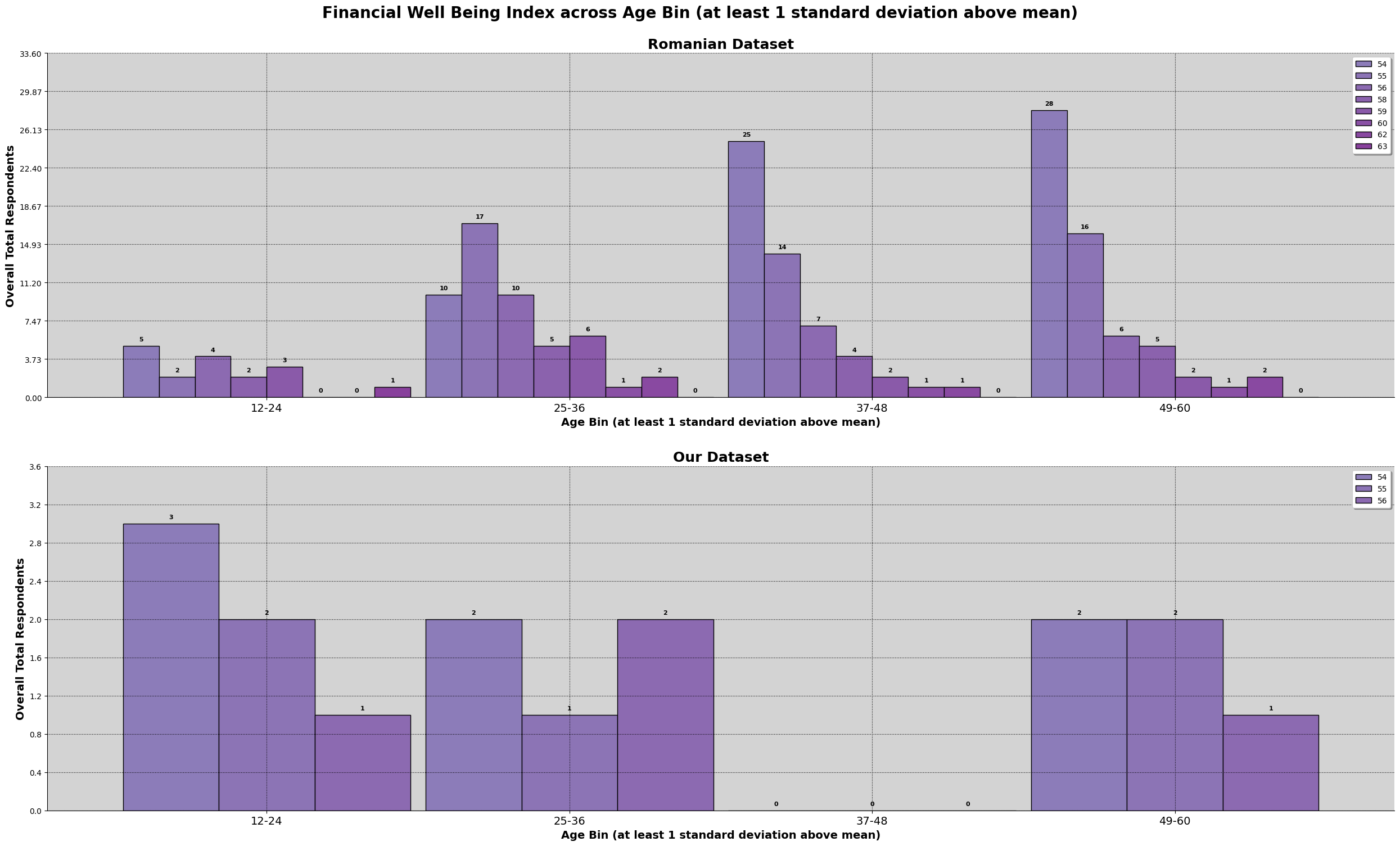

Based on the results, we can observed that the financial well being of both dataset. Romania has a wider range of scores as well as looking normally distributed. Our dataset might be suffering from insufficient data, which is causing the irregular shape.

We can also observe that there are about the same percentage of people experiencing the same amount of financial well being. Furthermore, for the romanian dataset, there are accounts of above 60 while our malaysian dataset, have not scored anything about 60. Furthermore, the mean line for both of the data are identical.

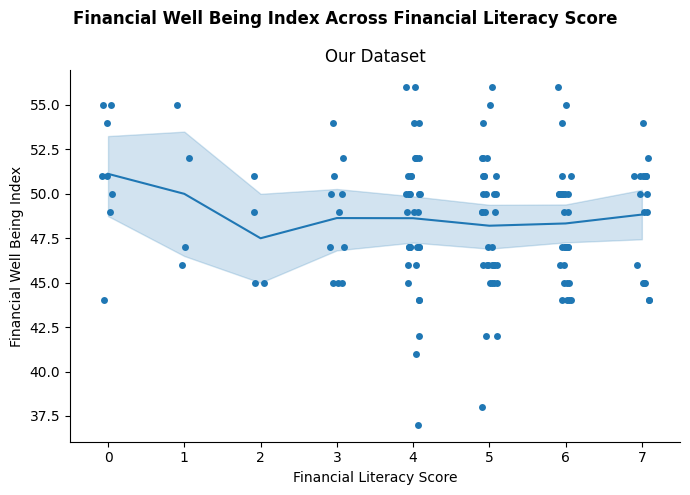

Having seen that our dataset's financial literacy is higher than the romanian dataset, and having more higher earners, we would expect that the financial well being of our dataset should be higher as well. However, we can observe that the maximum score for financial well being does not even pass 57.5.

# Score Aggregation

# ==================

# To store the romanian column indexes

romanian_financial_well_being_columns = []

# Base string is A1 and B1

base_string = ['A1_', 'B1_']

# Print romanian columns to see

print(romanian_dataset.columns)

# Loop from 1 to 6, for base string A

for sub_string in range(1,7):

romanian_financial_well_being_columns.append(

base_string[0] + str(sub_string)

)

# Loop from 1 to 4, for base string B

for sub_string in range(1,5):

romanian_financial_well_being_columns.append(

base_string[1] + str(sub_string)

)

# Too many strings will be required, therefore

# Check for the columns required

for num, column in enumerate(our_columns):

if num > 45 or num < 25:

continue

else:

print( str(num) + '\t' + column)

# Store the required colum

our_financial_well_being_columns = []

for num in range(31, 42):

if num != 37:

our_financial_well_being_columns.append(num)

# Completely = 4

completely_is_4 = [0, 1, 3]

completely_is_4_dict = {

'Completely': 4,

'Very well': 3,

'Somewhat': 2,

'Very little': 1,

'Not at all': 0

}

# Completely = 0

completely_is_0 = [2, 4, 5]

completely_is_0_dict = {

'Completely': 0,

'Very well': 1,

'Somewhat': 2,

'Very little': 3,

'Not at all': 4

}

# Always = 0

always_is_0 = [6, 8, 9]

always_is_0_dict = {

'Always': 4,

'Often': 3,

'Often ': 3,

'Sometimes': 2,

'Rarely': 1,

'Never': 0

}

# Always = 4

always_is_4 = [7]

always_is_4_dict = {

'Always': 0,

'Often': 1,

'Often ': 1,

'Sometimes': 2,

'Rarely': 3,

'Never': 4

}

# For romanian dataset

# Initialize lists to store column

romanian_financial_well_being_columns_completely_is_4 = []

romanian_financial_well_being_columns_completely_is_0 = []

romanian_financial_well_being_columns_always_is_4 = []

romanian_financial_well_being_columns_always_is_0 = []

# Loop through the list to get the columns

for num in completely_is_4:

romanian_financial_well_being_columns_completely_is_4.append(

romanian_financial_well_being_columns[num]

)

for num in completely_is_0:

romanian_financial_well_being_columns_completely_is_0.append(

romanian_financial_well_being_columns[num]

)

for num in always_is_0:

romanian_financial_well_being_columns_always_is_0.append(

romanian_financial_well_being_columns[num]

)

for num in always_is_4:

romanian_financial_well_being_columns_always_is_4.append(

romanian_financial_well_being_columns[num]

)

# Converting the values

romanian_financial_well_being = \

romanian_dataset[

romanian_financial_well_being_columns_completely_is_4

].replace(completely_is_4_dict)

romanian_financial_well_being[romanian_financial_well_being_columns_completely_is_0] = \

romanian_dataset[

romanian_financial_well_being_columns_completely_is_0

].replace(completely_is_0_dict)

romanian_financial_well_being[romanian_financial_well_being_columns_always_is_4] = \

romanian_dataset[

romanian_financial_well_being_columns_always_is_4

].replace(always_is_4_dict)

romanian_financial_well_being[romanian_financial_well_being_columns_always_is_0] = \

romanian_dataset[

romanian_financial_well_being_columns_always_is_0

].replace(always_is_0_dict)

# For our dataset

# Initialize lists to store column

our_financial_well_being_columns_completely_is_4 = []

our_financial_well_being_columns_completely_is_0 = []

our_financial_well_being_columns_always_is_4 = []

our_financial_well_being_columns_always_is_0 = []

# Loop through the list to get the columns

for num in completely_is_4:

our_financial_well_being_columns_completely_is_4.append(

our_columns[our_financial_well_being_columns[num]]

)

for num in completely_is_0:

our_financial_well_being_columns_completely_is_0.append(

our_columns[our_financial_well_being_columns[num]]

)

for num in always_is_0:

our_financial_well_being_columns_always_is_0.append(

our_columns[our_financial_well_being_columns[num]]

)

for num in always_is_4:

our_financial_well_being_columns_always_is_4.append(

our_columns[our_financial_well_being_columns[num]]

)

# Converting the values

our_financial_well_being = \

our_dataset[

our_financial_well_being_columns_completely_is_4

].replace(completely_is_4_dict)

our_financial_well_being[our_financial_well_being_columns_completely_is_0] = \

our_dataset[

our_financial_well_being_columns_completely_is_0

].replace(completely_is_0_dict)

our_financial_well_being[our_financial_well_being_columns_always_is_4] = \

our_dataset[

our_financial_well_being_columns_always_is_4

].replace(always_is_4_dict)

our_financial_well_being[our_financial_well_being_columns_always_is_0] = \

our_dataset[

our_financial_well_being_columns_always_is_0

].replace(always_is_0_dict)

financial_well_being_index_dict = {

0 : 14,

1 : 19,

2 : 22,

3 : 25,

4 : 27,

5 : 29,

6 : 31,

7 : 32,

8 : 34,

9 : 35,

10: 37,

11: 38,

12: 40,

13: 41,

14: 42,

15: 44,

16: 45,

17: 46,

18: 47,

19: 49,

20: 50,

21: 51,

22: 52,

23: 54,

24: 55,

25: 56,

26: 58,

27: 59,

28: 60,

29: 62,

30: 63,

31: 65,

32: 66,

33: 68,

34: 69,

35: 71,

36: 73,

37: 75,

38: 78,

39: 81,

40: 86

}

# Romanian Dataset

# Create a column that takes the sum of all the other columns

romanian_financial_well_being['Score'] = \

romanian_financial_well_being[romanian_financial_well_being_columns]\

.sum(axis=1)

# Given the current score, map it to the financial well being score

romanian_financial_well_being['Financial Well Being Index'] =\

romanian_financial_well_being['Score']\

.map(financial_well_being_index_dict)

# Storing Financial Well Being Index into main dataset

romanian_dataset['Financial Well Being Index'] = romanian_financial_well_being['Financial Well Being Index']

# Our Dataset

# Create a column that takes the sum of all the other columns

our_financial_well_being['Score'] = \

our_financial_well_being[

our_columns[our_financial_well_being_columns]

].sum(axis=1)

# Given the current score, map it to the financial well being score

our_financial_well_being['Financial Well Being Index'] = \

our_financial_well_being['Score']\

.map(financial_well_being_index_dict)

# Storing the Financial Well Being Index into the main dataset

our_dataset['Financial Well Being Index'] = our_financial_well_being['Financial Well Being Index']

# Data Preparation

# ================

# Get unique values of the financial well being index, and sort them in ascending order

# The plot will get wonky if it is not in order

romanian_financial_well_being_x = \

np.sort(romanian_financial_well_being['Financial Well Being Index'].unique())\

our_financial_well_being_x = \

np.sort(our_financial_well_being['Financial Well Being Index'].unique())

# Get the value count of each score, and then divide it by the size of each dataset

romanian_financial_well_being_y = \

(romanian_financial_well_being['Financial Well Being Index']\

.value_counts().get(romanian_financial_well_being_x)\

/ len(romanian_financial_well_being))

our_financial_well_being_y = \

(our_financial_well_being['Financial Well Being Index']\

.value_counts().get(our_financial_well_being_x)\

/ len(our_financial_well_being)

)

# Get mean value of the financial well being index

romanian_financial_well_being_mean = romanian_financial_well_being['Financial Well Being Index'].mean()

our_financial_well_being_mean = our_financial_well_being['Financial Well Being Index'].mean()

# Get median value of the financial well being index

romanian_financial_well_being_median = romanian_financial_well_being['Financial Well Being Index'].median()

our_financial_well_being_median = our_financial_well_being['Financial Well Being Index'].median()

# Get the std value of the financial well being index

romanian_financial_well_being_std = romanian_financial_well_being['Financial Well Being Index'].std()

our_financial_well_being_std = our_financial_well_being['Financial Well Being Index'].std()

# Initialize the figure

figure, ax = plt.subplots(figsize=(17,8))

figure.suptitle(

'Financial Well Being',

fontweight = 'bold',

fontsize = 20

)

# Plot romania data

# ==================

ax.plot(

romanian_financial_well_being_x,

romanian_financial_well_being_y,

color = 'darkgray',

label = 'Romania'

)

ax.fill_between(

romanian_financial_well_being_x,

romanian_financial_well_being_y[romanian_financial_well_being_x],

alpha = 0.5,

color = 'darkgray'

)

# Plot our data

# ===============

ax.plot(

our_financial_well_being_x,

our_financial_well_being_y,

color = 'teal',

label = 'Malaysia'

)

ax.fill_between(

our_financial_well_being_x,

our_financial_well_being_y[our_financial_well_being_x],

alpha = 0.2,

color = 'teal'

)

# Mean line and annotations

# ==========================

ax.axvline(

romanian_financial_well_being_mean,

0.025,

ls = '--',

color = 'darkgray',

label = 'Romanian Mean',

linewidth = 5

)

ax.annotate(

f'Mean: {romanian_financial_well_being_mean:.3g}',

xy=(romanian_financial_well_being_mean - 3, 0.15),

fontsize=16, fontweight='bold', color='grey'

)

ax.axvline(

our_financial_well_being_mean,

0.025,

ls = '--',

color = 'teal',

label = 'Malaysian Mean',

alpha = 0.4,

linewidth = 5

)

ax.annotate(

f"Mean: {our_financial_well_being_mean:.3g}",

xy=(our_financial_well_being_mean - 3 ,0.14),

fontsize=16, fontweight='bold', color='teal')

# Median line and annotations

# ==========================

ax.axvline(

romanian_financial_well_being_median,

0.025,

ls = ':',

color = 'darkgray',

label = 'Romanian Median',

linewidth = 5

)

ax.annotate(

f"Median: {romanian_financial_well_being_median:.3g}",

xy=(romanian_financial_well_being_median + 0.7 ,0.05),

fontsize=16, fontweight='bold', color='grey')

ax.axvline(

our_financial_well_being_median,

0.025,

ls = ':',

color = 'teal',

label = 'Malaysian Median',

linewidth = 5

)

ax.annotate(

f"Median: {our_financial_well_being_median:.3g}",

xy=(our_financial_well_being_median + 0.7 ,0.04),

fontsize=16, fontweight='bold', color='teal')

# Set the x limit, initially used 16 to 91, the limits of the financial well being score, but the plot will look thin

ax.set_xlim(33,65)

# Set x and y label and have a larger legend

ax.set_ylabel('Percentage (%)')

ax.set_xlabel('Financial Well Being Index')

ax.spines[['top', 'right']].set_visible(False)

ax.legend(fontsize = 16, shadow=True, bbox_to_anchor=(0.85, 1.015))

formatter = mtick.PercentFormatter(xmax=1.0)

ax.yaxis.set_major_formatter(formatter)

ax.grid(alpha=0.5, linestyle='--')

# Optimize layout and show the figure

plt.tight_layout()

plt.show()

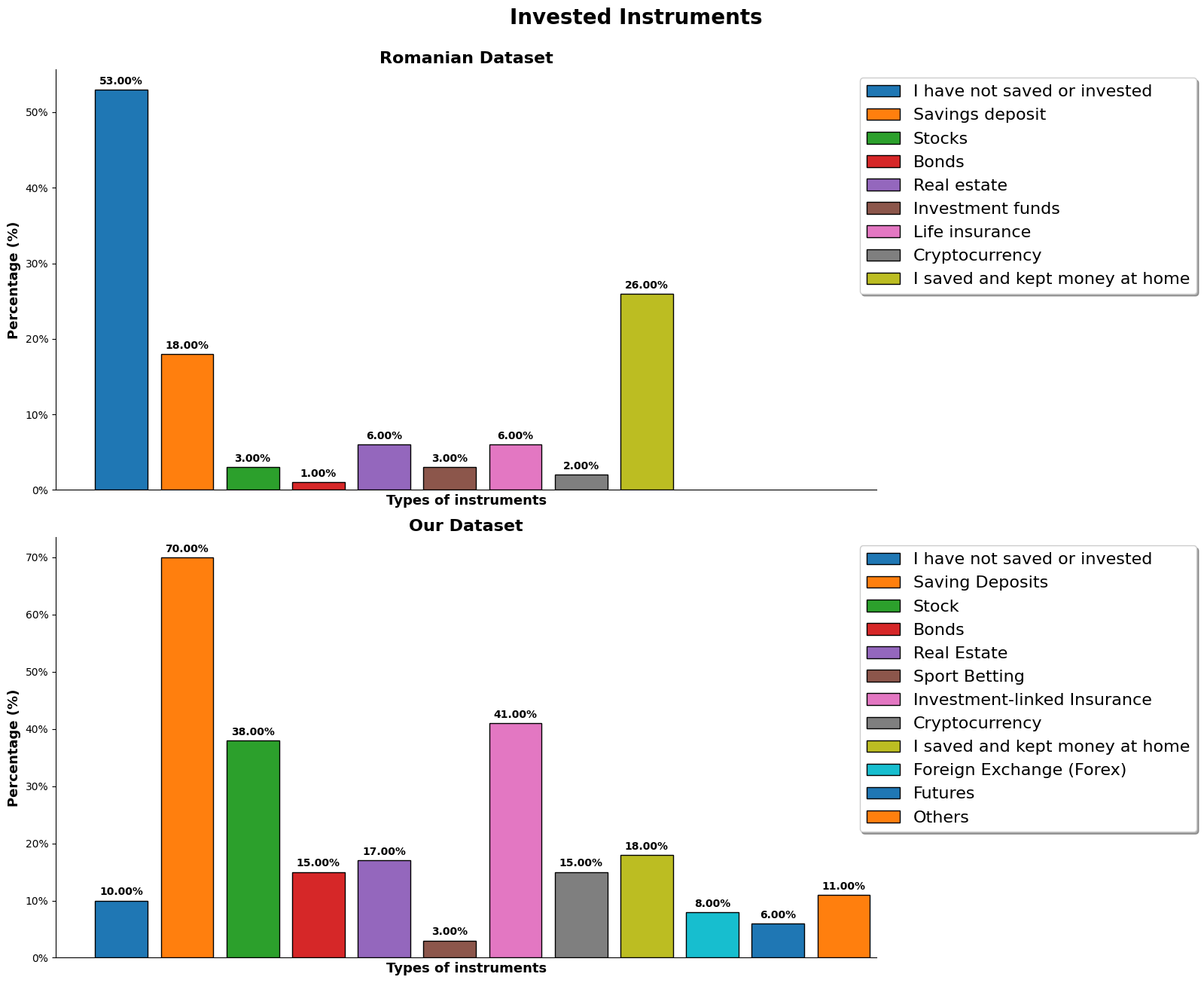

Invested Money in any Financial Instruments

For the romanian dataset, the following table is what the each column represent. We will only be changing the 'yes' and 'no' to 0s and 1s, and create a custom dictionary for labeling the columns.

For the romanian dataset, the following table are the options available for them to choose. They were only able to pick 2 out of the listed choices.

| Column | Financial Instrument |

|---|---|

| I2_1 | Savings deposit |

| I2_2 | Stocks |

| I2_3 | Bonds |

| I2_4 | Real estate |

| I2_5 | Investment funds |

| I2_6 | Life insurance |

| I2_7 | Cryptocurrency |

| I2_8 | I saved and kept money at home |

| I2_0 | I have not saved or invested |

For our dataset and our survey, we have allowed our participants to select whichever is applicable to them, because it is likely to be holding more than 2 choices shown. Additionally, we added more choices of financial instruments, as well as altering one from the ones from the romanian dataset. The additional and alterned choice are as follows:

| Financial Instrument |

|---|

| Life Insurance --> Investment-linked Insurance |

| Sport Betting |

| Foreign Exchange (Forex) |

| Futures |

| Others |

We changed 'Life Insurance' to 'Investement-linked Insurance', because the life insurance schemes here are not really viewed as choices of investement, but a financial protection from accidents. However, there are insurance coverages, including life insurances, that has some form of investment component or feature that comes along with it. Hence, the change of the choice for better clarification.

We can see a drastic difference in the saving habits from our dataset and the romanian dataset, just from the first 2 choices alone. There is only 10% of the our dataset who have not saved and have not invested while there were half of the romanian dataset who does the same. Almost everyone in our dataset has at least got a savings deposit while the romanian dataset has 18%.

# Data Preparation

# =================

# Romanian Dataset ===

# To store the column indexes

romanian_invested_instruments_columns = []

# Base string is I2_

romanian_invested_instruments_string = 'I2_'

# Loop from 0 to 8

for sub_string in range(0,9):

# Store the base string and sub string into the list

romanian_invested_instruments_columns.append(

romanian_invested_instruments_string +

str(sub_string)

)

# Custom dictionary to represent the labels in plot

custom_dict_invested_instruments_romanian_columns = {

'I2_0': 'I have not saved or invested',

'I2_1': 'Savings deposit',

'I2_2': 'Stocks',

'I2_3': 'Bonds',

'I2_4': 'Real estate',

'I2_5': 'Investment funds',

'I2_6': 'Life insurance',

'I2_7': 'Cryptocurrency',

'I2_8': 'I saved and kept money at home'

}

# Changing the 'yes' and 'no' values into binary

romanian_invested_instruments = romanian_dataset[romanian_invested_instruments_columns]\

.replace({'Yes':1 , 'No':0})

# Storing new names for the processed columns

processed_columns = []

base_string = 'Saved or Invested in '

for col in romanian_invested_instruments_columns:

processed_columns.append(

base_string +

custom_dict_invested_instruments_romanian_columns[col])

# Store the new processed columns into main dataset

romanian_dataset[processed_columns] = romanian_invested_instruments

# Our Dataset ==

# Get the column string

our_invested_instruments_string = getOurString('saved or invested money', our_columns)

# Split each row as it contains multiple entries

our_invested_instruments = our_dataset[our_invested_instruments_string]\

.str.split(',', expand=True).stack()

# Take the values and turn it into columns, and fill the blanks with 0s

our_invested_instruments = pd.get_dummies(our_invested_instruments)\

.groupby(level=0).sum()

# Print the columns for custom dict

print('Columns: ', our_invested_instruments.columns)

# Custom dictionary to arrange the columns similar to the above

custom_dict_invested_instruments_our_columns = {

0:'I have not saved or invested',

1:'Saving Deposits',

2:'Stock',

3:'Bonds',

4:'Real Estate',

5:'Sport Betting',

6:'Investment-linked Insurance',

7:'Cryptocurrency',

8:'I saved and kept money at home',

9:'Foreign Exchange (Forex)',

10:'Futures',

11:'Others'

}

# Processed column names

processed_columns = 'Saved or Invested in ' + our_invested_instruments.columns

# Store into main dataset

our_dataset[processed_columns] = our_invested_instruments

# Plot Figure

# =============

# Initialize figure

fig, ax = plt.subplots(2,1,figsize=(17,13))

# Insert Title

fig.suptitle(

'Invested Instruments',

fontweight = 'bold',

fontsize = 20, y=1)

# Set width

width = 0.8

# Set formatter for percentage

formatter = mtick.PercentFormatter(xmax=1.0)

datasets = [

('Romanian Dataset', romanian_invested_instruments_columns, romanian_invested_instruments, custom_dict_invested_instruments_romanian_columns, ax[0]),

('Our Dataset', our_invested_instruments, custom_dict_invested_instruments_our_columns, custom_dict_invested_instruments_our_columns, ax[1])

]

for set, columns, dict_cols, labels, ax in datasets:

if set == 'Romanian Dataset':

for col_no, column in enumerate(columns):

container = ax.bar(

col_no, round(dict_cols[column].mean(),2),

width, label=labels[column], edgecolor='black'

)

ax.bar_label(container, fontsize=10, fontweight='bold', padding=3, fmt='{:.2%}')

else:

for col_no in range(0, len(columns.columns)):

container = ax.bar(

col_no, round(columns[dict_cols[col_no]].mean(),2),

width, label=labels[col_no], edgecolor='black'

)

ax.bar_label(container, fontsize=10, fontweight='bold', padding=3, fmt='{:.2%}')

ax.set_title(set, fontsize=16, fontweight='bold')

ax.set_xticks([])

ax.set_ylabel('Percentage (%)', fontsize=13, fontweight='bold')

ax.set_xlabel('Types of instruments', fontsize=13, fontweight='bold')

ax.set_xlim(-1, 11.5)

ax_distict_legends = ax.get_legend_handles_labels()[1][:]

ax.legend(ax_distict_legends, bbox_to_anchor=(1.4,1), shadow=True, fontsize=16)

ax.yaxis.set_major_formatter(formatter)

ax.spines[['right', 'top']].set_visible(False)

plt.tight_layout()

plt.show()

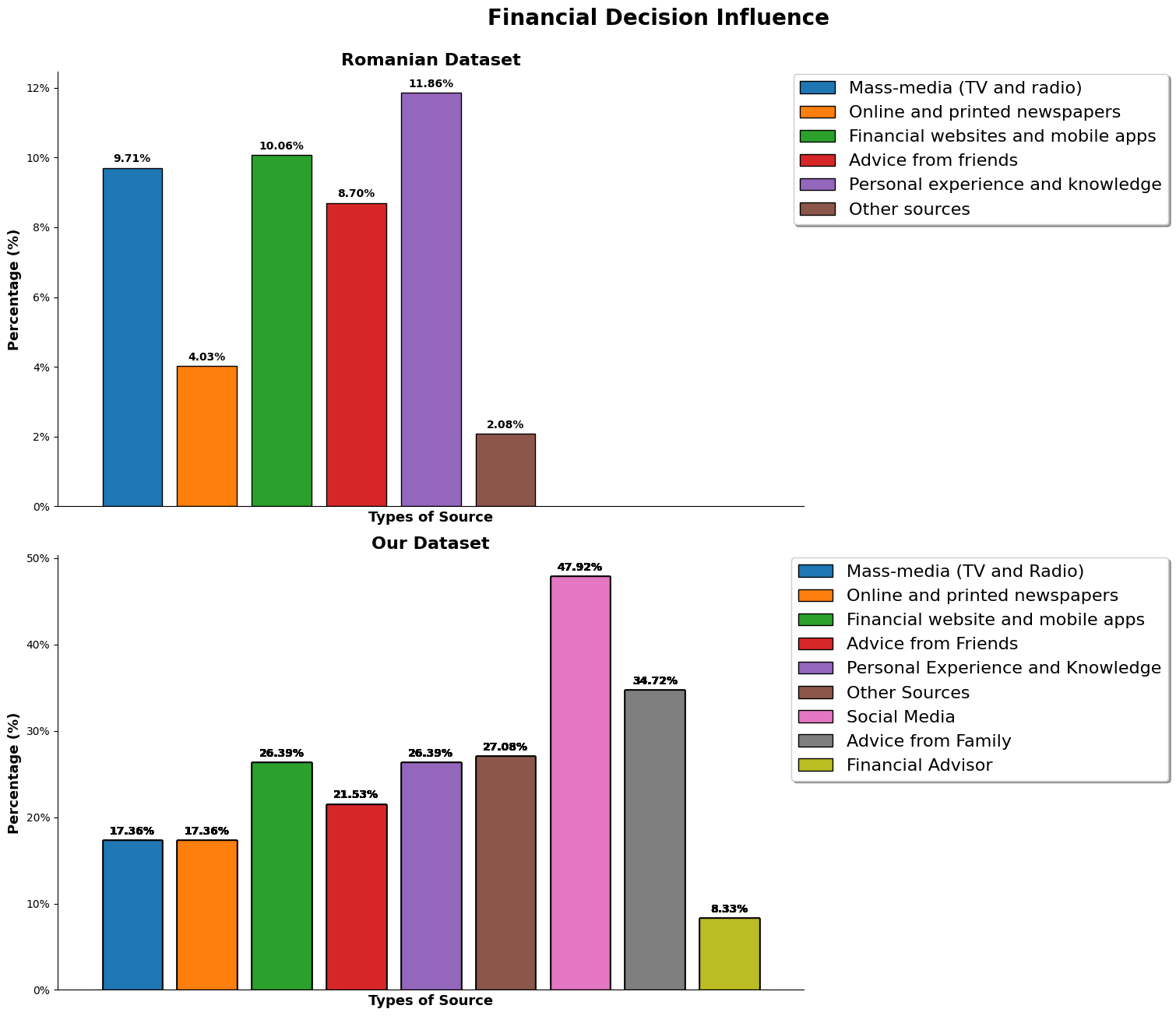

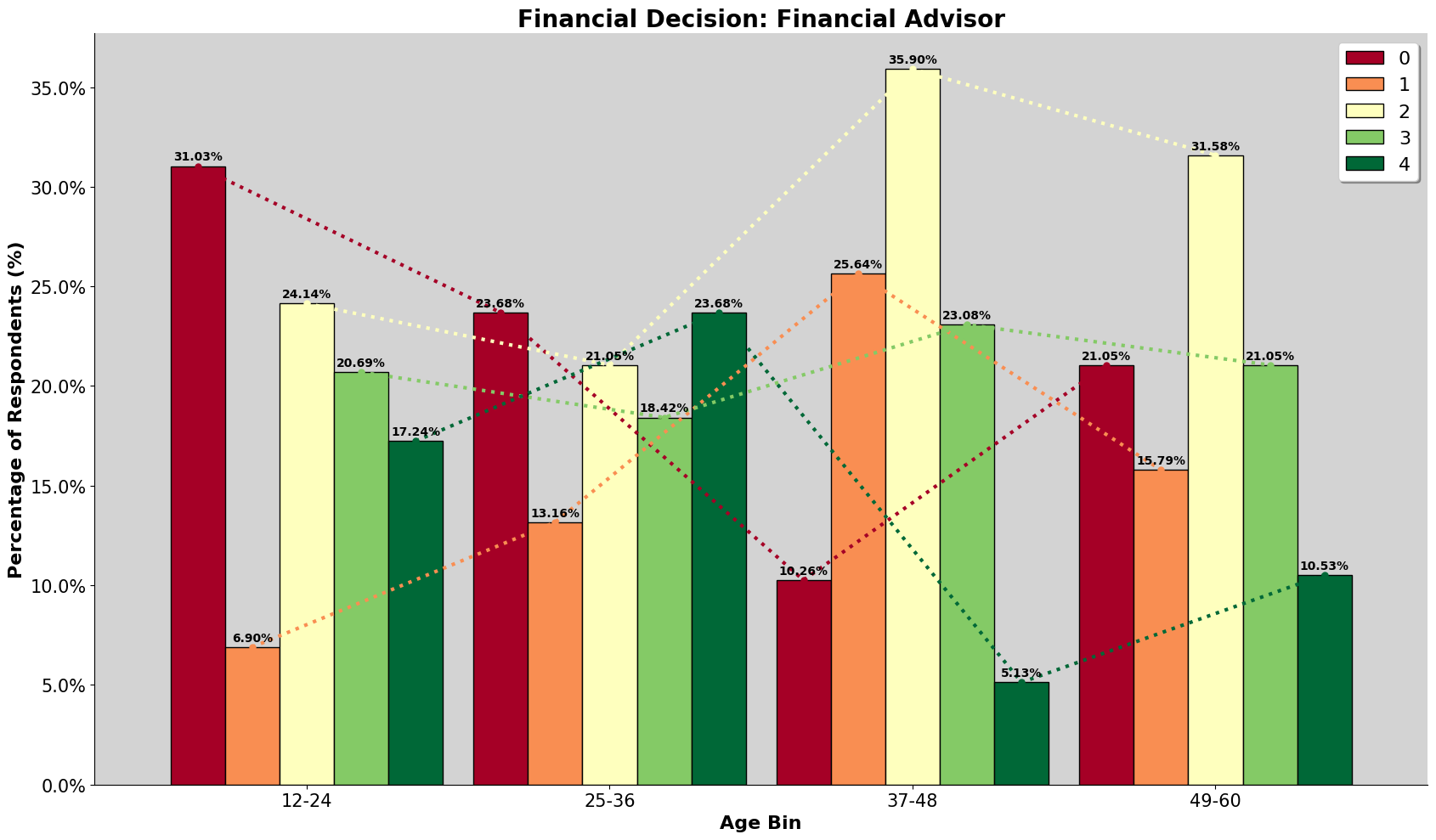

Financial Decision Influence

Similarly to the above, we have added more options for participants to choose, so we can further explore.

For the romanian dataset, the following is the choices given:

| Column | Financial Decision Influence |

|---|---|

| I3_1 | Mass-media (TV and radio) |

| I3_2 | Online and printed newspapers |

| I3_3 | Financial websites and mobile apps |

| I3_4 | Advice from friends |

| I3_5 | Personal experience and knowledge |

| I3_6 | Other sources |

For our dataset, we have added the following as well:

| Financial Decision Influence |

|---|

| Social Media |

| Advice from Family |

| Financial Advisor |

Initially, we thought of plotting the likert scale from least value to highest value for every source but it looked too messy to comprehend. Therefore, chose to only filter those that have values of 3 and 4, which are 'very influenced' and 'main influence' respectively, and to display them as percentage basis.

Because of the lesser restriction in our survey, participants get to rank how they feel about each of the source. We can see that many values are inflated and might need a deeper dive and specify what to filter and look into. The initial draft of the survey, we wanted the survey participants to rank their top 4 influences, but there were feedback stating that it was too confusing to do, so we then changed it too ranking all of them, but then there were more feedback about it being tedious as well. Hence, we ended up having them choose how influential each source are to them.

We can observe that for the romanian dataset, due to the limitation of choice, their answer should be more substantiated and for them, there are heavily influence by mass-media and from learning from their own personal experience and knowledge, while for our dataset, many of the participants are heavily influenced by social media and advice from family.

As shown by the result, even though 27% of them chose other as the source, but there were only few entries of proper input. It could be because of the survey design, participants might have been confused or selected wrongly.

When, we look into 'other sources', the listed output were 'Financial Database', 'Financial Books', and 'Constultant'.

# Data Prepration

# ===============

# Romanian Dataset ==

# To store the column indexes

romanian_financial_decision_columns = []

# Base string is I3

romanian_financial_decision_string = 'I3_'

# Loop from 1 to 6

for sub_string in range(1,7):

romanian_financial_decision_columns.append(

romanian_financial_decision_string +

str(sub_string)

)

# Custom dictionary to represent the labels in plot

custom_dict_financial_decision_romanian_columns = {

'I3_1':'Mass-media (TV and radio)',

'I3_2':'Online and printed newspapers',

'I3_3':'Financial websites and mobile apps',

'I3_4':'Advice from friends',

'I3_5':'Personal experience and knowledge',

'I3_6':'Other sources'

}

# Changing the 'yes' and 'no' values into binary

romanian_financial_decisions = romanian_dataset[romanian_financial_decision_columns]\

.replace({'Yes':1, 'No':0})

# Filling the null values

for col in romanian_financial_decision_columns:

romanian_financial_decisions[col] = romanian_financial_decisions[col].fillna(0)

# Names for the processed columns

romanian_financial_decision_columns_processed = []

for col in romanian_financial_decision_columns:

romanian_financial_decision_columns_processed.append(

'Financial Decision: ' +

custom_dict_financial_decision_romanian_columns[col]

)

# Store them into main dataset

romanian_dataset[romanian_financial_decision_columns_processed] = romanian_financial_decisions

# Our Dataset ===

# Store the required

our_financial_decision_columns = [x for x in range(16, 25)]

# Store the index of the column, column description and match the order to the romanian dataset

custom_dict_financial_decision_our_columns = {

0:( 16, 'Mass-media (TV and Radio)'),

1:( 17, 'Online and printed newspapers'),

2:( 18, 'Financial website and mobile apps'),

3:( 20, 'Advice from Friends'),

4:( 22, 'Personal Experience and Knowledge'),

5:( 24, 'Other Sources'),

6:( 19, 'Social Media'),

7:( 21, 'Advice from Family'),

8:( 23, 'Financial Advisor')

}

# Convert the string input into integers

our_financial_decision = our_dataset[our_columns[our_financial_decision_columns]]\

.replace({

'Not applicable / No influence at all': 0,

'Somewhat influenced': 1,

'Influenced': 2,

'Very Influenced': 3,

'Main influence': 4

})

# Filling some of the null values

our_financial_decision = our_financial_decision.fillna(0)

# Renaming the processed columns

our_financial_decision_column_name = []

for col in our_financial_decision.columns:

print('Financial Decision: ' + col[6:])

our_financial_decision_column_name.append('Financial Decision: ' + col[6:])

# Store the processed columns into the main dataset

our_dataset[our_financial_decision_column_name] = our_financial_decision

# Plot Figure

# ===========

# Initialize the figure

figure, ax = plt.subplots(2,1, figsize=(17,13))

figure.suptitle(

'Financial Decision Influence',

fontsize = 20,

fontweight = 'bold', y=1)

# Set width

width = 0.8

# Set formatter for percentage

formatter = mtick.PercentFormatter(xmax=1.0)

# Set values to loop

datasets = [

('Romanian Dataset', ax[0]),

('Our Dataset', ax[1])

]

# Looping through values

for set, ax in datasets:

if set == 'Romanian Dataset':

for col_no, column in enumerate(romanian_financial_decision_columns):

container = ax.bar(

col_no, romanian_financial_decisions[column].mean(),

width = width, label = custom_dict_financial_decision_romanian_columns[column],

edgecolor = 'black'

)

ax.bar_label(container, fontsize=10, fontweight='bold', padding=3, fmt='{:.2%}')

else:

for col_no in range(0, len(our_financial_decision_columns)):

container = ax.bar(

col_no,

our_financial_decision[

our_columns[our_financial_decision_columns[col_no]]]\

.loc[(our_financial_decision[

our_columns[our_financial_decision_columns[col_no]]] > 2)]\

.count()/our_financial_decision.count(),

width = width,

label = custom_dict_financial_decision_our_columns[col_no][1],

edgecolor = 'black'

)

ax.bar_label(container, fontsize=10, fontweight='bold', padding=3, fmt='{:.2%}')

# Styling

ax.set_xticks([])

ax.set_title(set, fontweight='bold', fontsize=16)

ax.set_ylabel('Percentage (%)', fontsize=13, fontweight='bold')

ax.set_xlabel('Types of Source', fontsize=13, fontweight='bold')

ax.set_xlim(-1, 9)

ax_distict_legends = ax.get_legend_handles_labels()[1][:]

ax.legend(ax_distict_legends, bbox_to_anchor=(1.5,1.015), fontsize=16, shadow=True)

ax.yaxis.set_major_formatter(formatter)

ax.spines[['top', 'right']].set_visible(False)

# Optimize layout and show figure

plt.tight_layout()

plt.show()Exploring and Futher Analysing Combined Traits

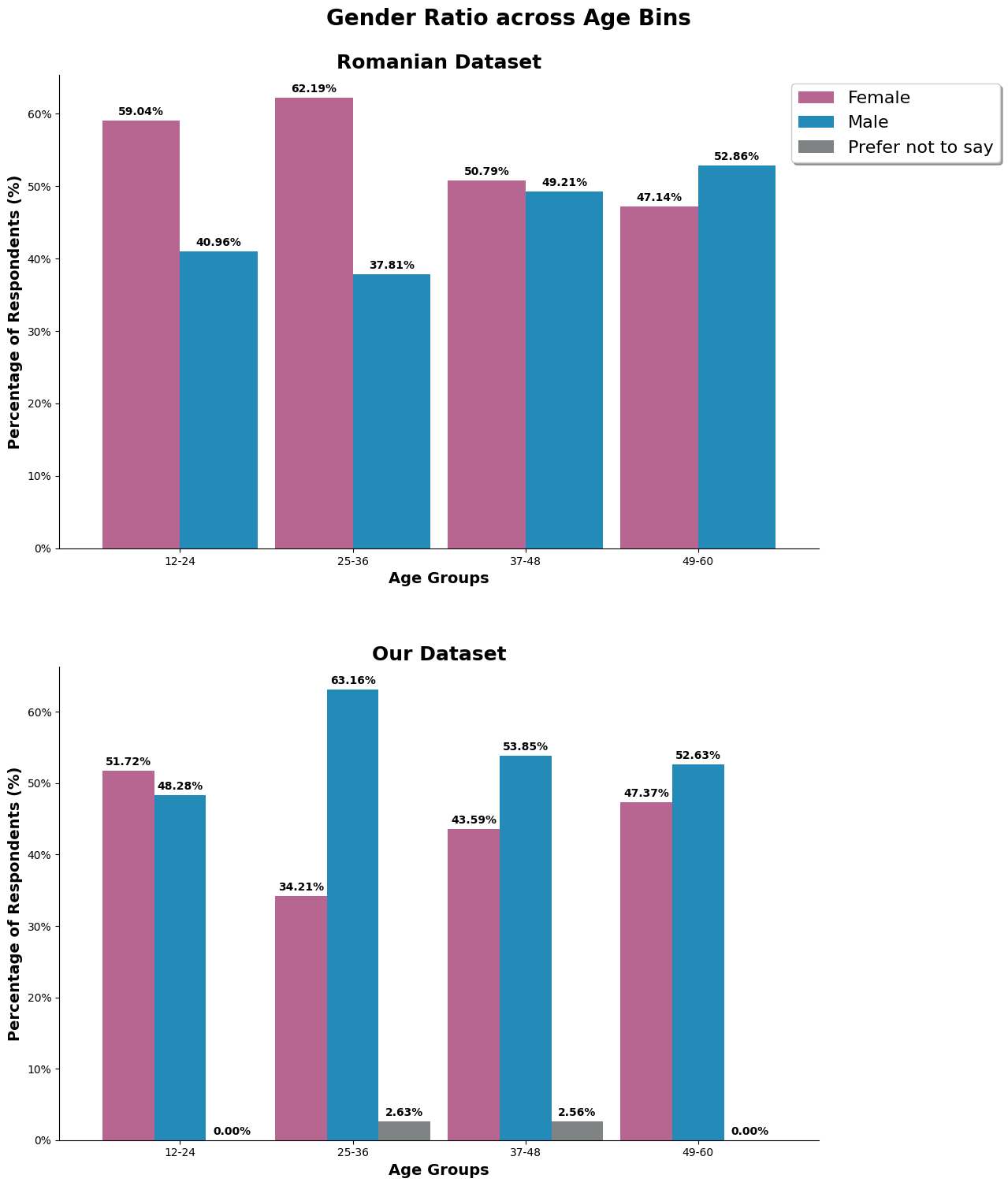

Gender accross Age Bin

Digging deeper into gender and split it by the age groups, we can observe the causes of the imbalance ratio of gender in our dataset. It is very male dominant at the age range, two times more than female. Additionally, this is also the age group where there is alot of survey participants.

For the romanian dataset, the first two age group has a slightly of females, but because the first two age group makes ups lesser portion of the population, it has a lesser effect on the overall gender ratio.

# Get the age and gender columns from the data set

romanian_dataset_age_gender = romanian_dataset.filter(items=['SD2', 'SD3'])

our_age_string = getOurString('your age', our_columns)

our_dataset_age_gender = our_dataset.filter(

items = [

our_age_string,

our_gender_string

]

)

# Segment and sort data in to bins

age_bins_romania = pd.cut(

romanian_dataset_age_gender['SD3'],

bins = [x for x in range(12,61,12)],

labels = ['12-24', '25-36', '37-48', '49-60'])

age_bins_our = pd.cut(

our_dataset_age_gender[our_age_string],

bins = [x for x in range(12,61,12)],

labels = ['12-24', '25-36', '37-48', '49-60']

)

# Group the data based on Age